Go Digit offers motor insurance, health insurance, travel insurance, property insurance, marine insurance, liability insurance and other insurance products which the customers can customize to meet his or her needs

Posts in category investments

Nitin Spinners Ltd is all Set to grow well with new capacity on stream. Buy for target price of ₹465 (36% upside): SMIFS

Nitin Spinners Ltd (NSPL) came out with a decent performance in an improving business

environment (from margin perspective) during Q4FY24. Recent capacity addition led to ~22%/~64%/~30% growth in sales/EBITDA/PBT on YoY basis

Zen Technologies Ltd is a Rising Star. Co has guided for Rs 900 cr plus revenue along with EBITDA margin of ~35% for FY25. Buy for target price of ₹1137 (20.4% upside): SBI Securities

Valuation still attractive; Maintain buy rating- Target Rs 1,137/- At the current price, Zen Technologies is trading at 36.8x/26.1x of its FY25E/FY26E earnings respectively. We maintained our buy rating on the stock with upgraded price target of Rs 1,137.0/- thus providing an upside potential of 20.4 %

SBI has demonstrated its strength in the last few quarters both on core operating performance and asset quality. Buy for target price of ₹1000 (22% upside): ICICI Direct

SBI has demonstrated its strength in the last few quarters both on core operating performance and asset quality. Management remains confident on growth, maintenance of margins and improvement in RoA. Sustained balance sheet growth (13-15%), strong liabilities franchise and prudent asset quality is expected to aid RoA at ~1% in FY25-26E. Gains on treasury and recovery from existing stressed book to act as catalyst. Valuing the bank at ~1.6x FY26E BV and subsidiaries at ~₹184/share, we revise our target price at ₹1000 (from ₹800). Maintain Buy

HIL has dominant market position in the domestic fiber cement sheet industry. Buy for target price of ₹3093 (25% upside): SMIFS

Considering HIL’s dominant market position in the domestic fiber cement sheet industry and its commitment to achieve USD 1 bn revenue over next 3-4 years, we continue to value the stock at 10xFY26e EPS of Rs. 309.3 to arrive at a target price of Rs. 3093. We continue to have a “Buy” rating on the stock

BSE has limited scope for further rerating. Reduce for target prie of ₹2860: HDFC Sec

We thereby downgrade BSE to REDUCE, based on regulatory uncertainty, expected growth moderation in FY26E and rich valuations. Our target price of INR 2,860 is based on 35x (vs 40x earlier) core FY26E PAT + CDSL stake + net cash ex SGWe thereby downgrade BSE to REDUCE, based on regulatory uncertainty, expected growth moderation in FY26E and rich valuations. Our target price of INR 2,860 is based on 35x (vs 40x earlier) core FY26E PAT + CDSL stake + net cash ex SGWe thereby downgrade BSE to REDUCE, based on regulatory uncertainty, expected growth moderation in FY26E and rich valuations. Our target price of INR 2,860 is based on 35x (vs 40x earlier) core FY26E PAT + CDSL stake + net cash ex SG

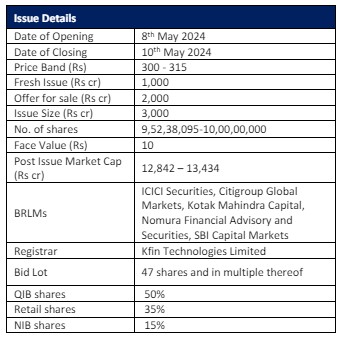

IPO: TBO Tek has a capital efficient business model with a combination of sustainable growth. Subscribe: SBI Securities

TBO Tek Limited is a top travel distribution platform operating in 100+ countries. The company’s platform connects suppliers (hotels, airlines, car rentals, cruises, etc.) and buyers (travel agencies, tour operators, etc.) through a two-sided technology platform

The Anup Engineering has strong visibility going ahead. Buy for target price of ₹2600 (28% upside): ICICI Direct

The Anup Engineering (TAEL) is one of the leading manufacturers of process equipment like heat exchangers, vessels, reactors, columns etc. Company supplies this equipment to sectors like oil & gas, petrochemicals, chemicals, fertiliser, power, aerospace and other process Industries in India and worldwide

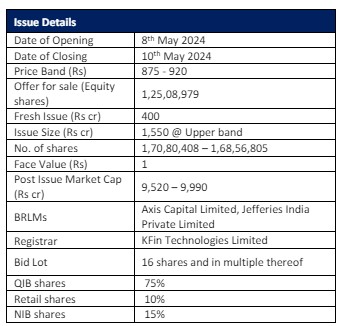

Aadhar Housing Finance (IPO) has strong parentage and professional management team. Subscribe: SBI Securities

The company is well-placed to cater to the niche segment with strong origination skills, understanding of the customers’ needs as well as focus on smaller cities. We expect these factors will help in garnering market share going ahead.

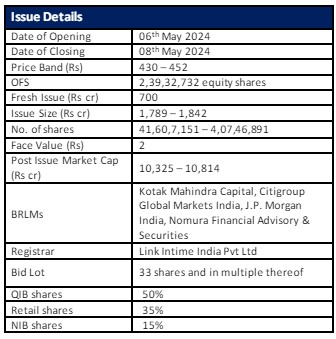

Indegene IPO: The company operates with a unique business model. Subscribe to the IPO: SBI Securities

Company Overview: Indegene Ltd is a technology led digital commercialization provider to the life science industry, including biopharmaceutical, emerging biotech and medical device companies. The company provides technology led expertise and capabilities that assists clients with drug development, clinical trials, regulatory submissions, pharmacovigilance, complaint management and sales & marketing services. Indegene operates across i) Enterprise […]

Recent Comments