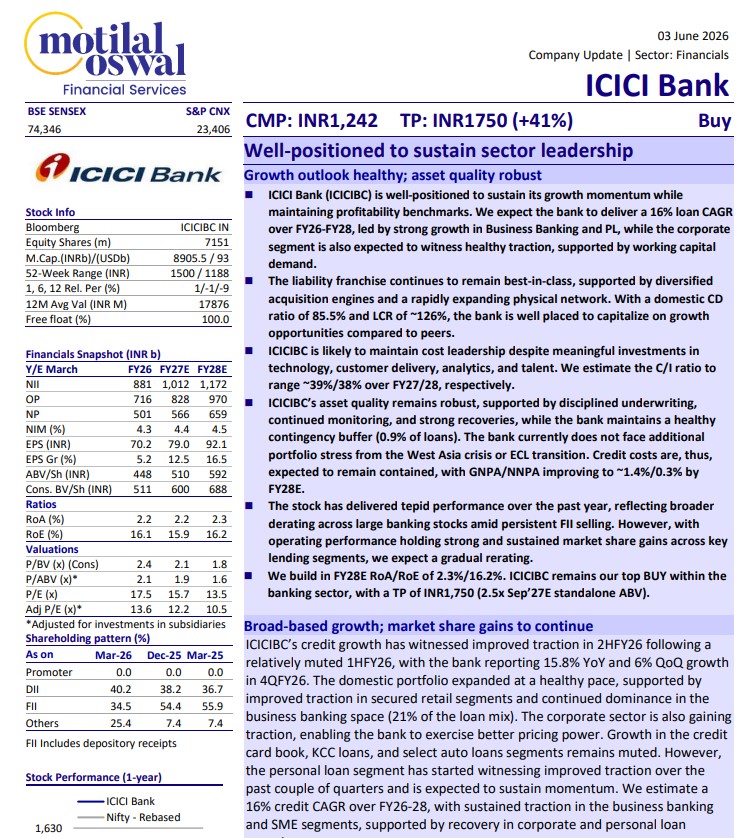

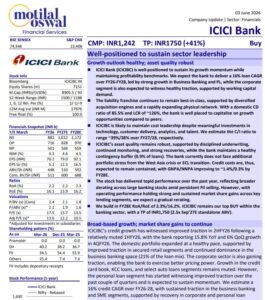

ICICIBC’s asset quality remains robust, supported by disciplined underwriting, continued monitoring, and strong recoveries

Management is guiding for EBITDA per wheel expansion from ₹262 to approximately ₹300 in...

LTHL is undergoing a restructuring with focus demerging the business into two separate entity...

For FY27, management guided for 18-20% overall revenue growth, with laminates revenue is projected...

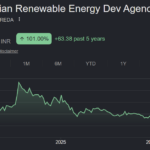

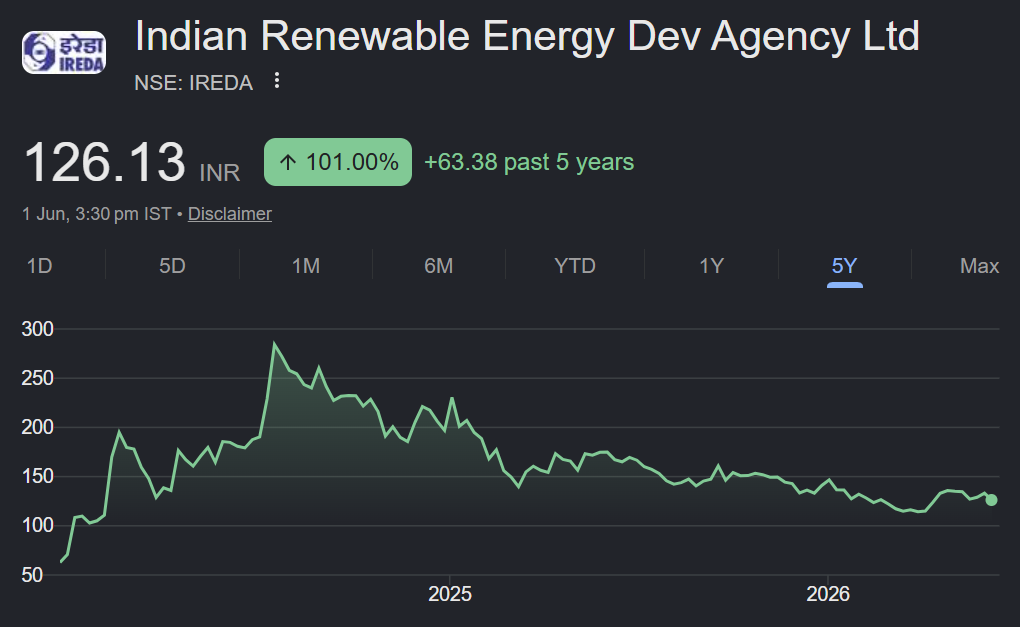

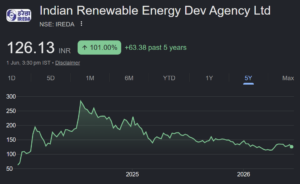

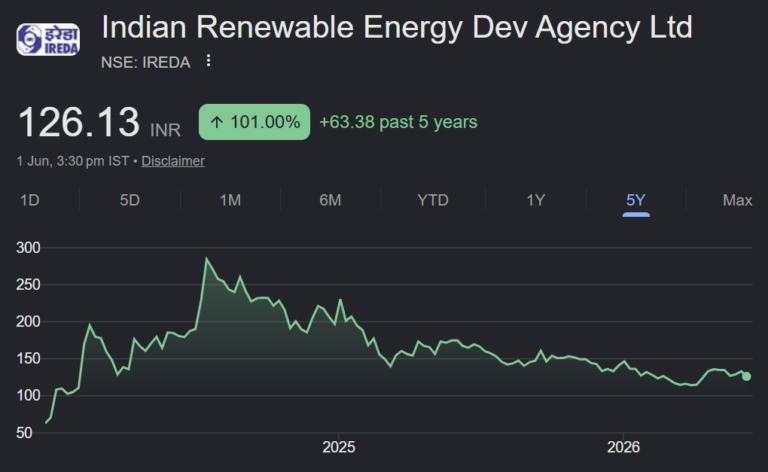

IREDA delivered mixed Q4FY26 performance, sustaining AUM growth at ~22% YoY (6% QoQ) to...

We believe earnings growth will accelerate over the next three years, driven by increased...

ELGi continues to generate approximately 100% EBITDA-to-cash conversion and maintains a strong net cash...

The company has strategically transitioned from a product supplier to a comprehensive solution provider...

Part of the multi-billion dollar INOXGFL Group, Inox Wind is one of India's leading...

Shriram properties is expected to remain on a strong pre-sales growth trajectory over the...