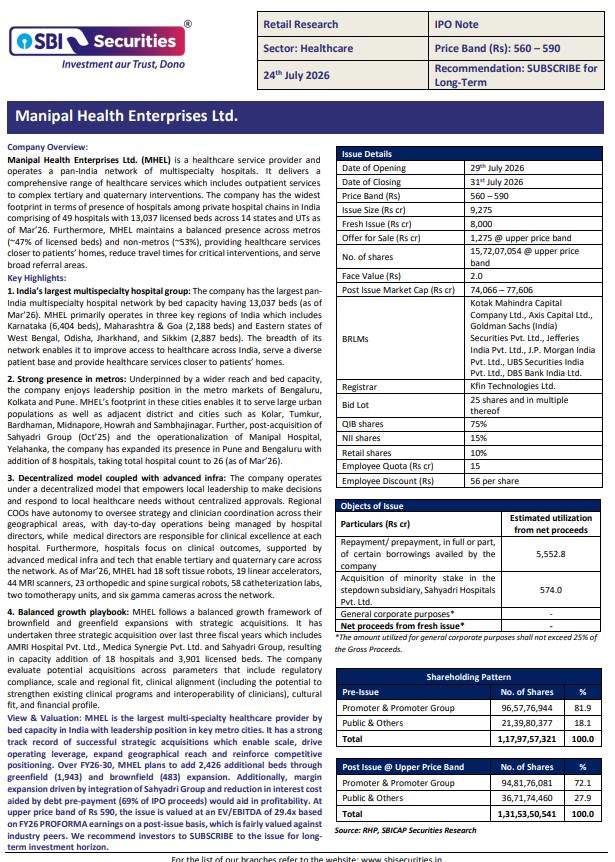

Manipal Health Enterprises (MHEL) is the largest multi-specialty healthcare provider by bed capacity in...

Indo SMC's robust quarterly performance, healthy order inflows, and exposure to structurally growing sectors...

Madhu Kela's Singularity investing in Max India highlights increasing institutional confidence in India's emerging...

Dhabriya Polywood remains a relatively under-the-radar micro-cap operating at the intersection of India's housing,...

Ashish Kacholia has built a reputation for identifying scalable businesses early, particularly in engineering,...

HFCL appears to be entering a new phase of growth driven by three structural...

Continued focus on expanding distribution channels and direct sourcing is expected to support business...

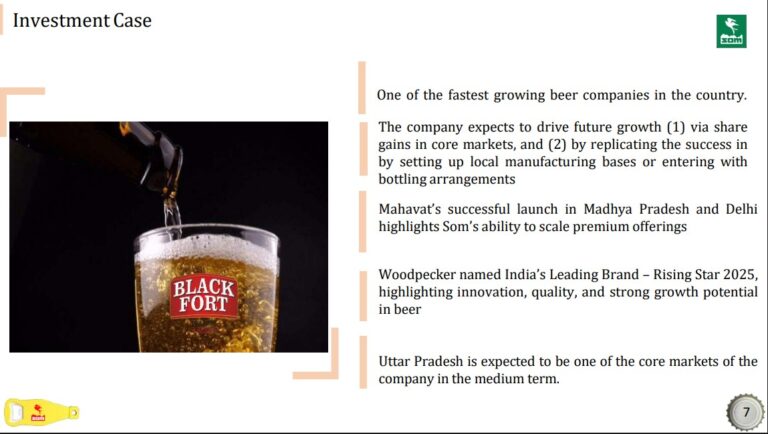

Despite recent setbacks, Som Distilleries continues to enjoy a strong position in the beer...

Despite global uncertainty, Vikas Khemani's long-term outlook remains firmly constructive.

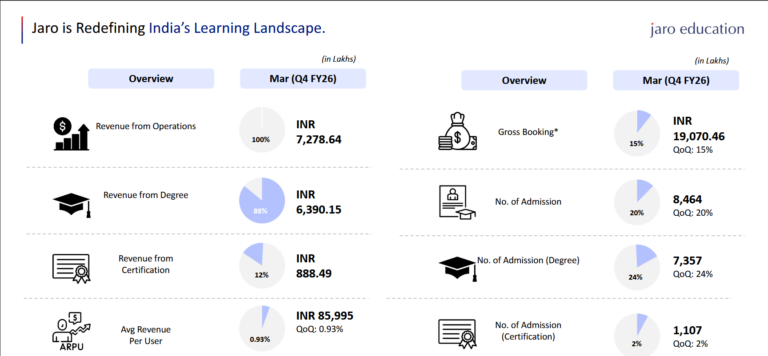

One of the biggest strengths highlighted by Deven Choksey Research is Jaro's capital-efficient business...