Far from being a passive stock picker who got lucky, the Big Bull was...

The company has raised its planned QIP size to ₹ 250 crore from ₹...

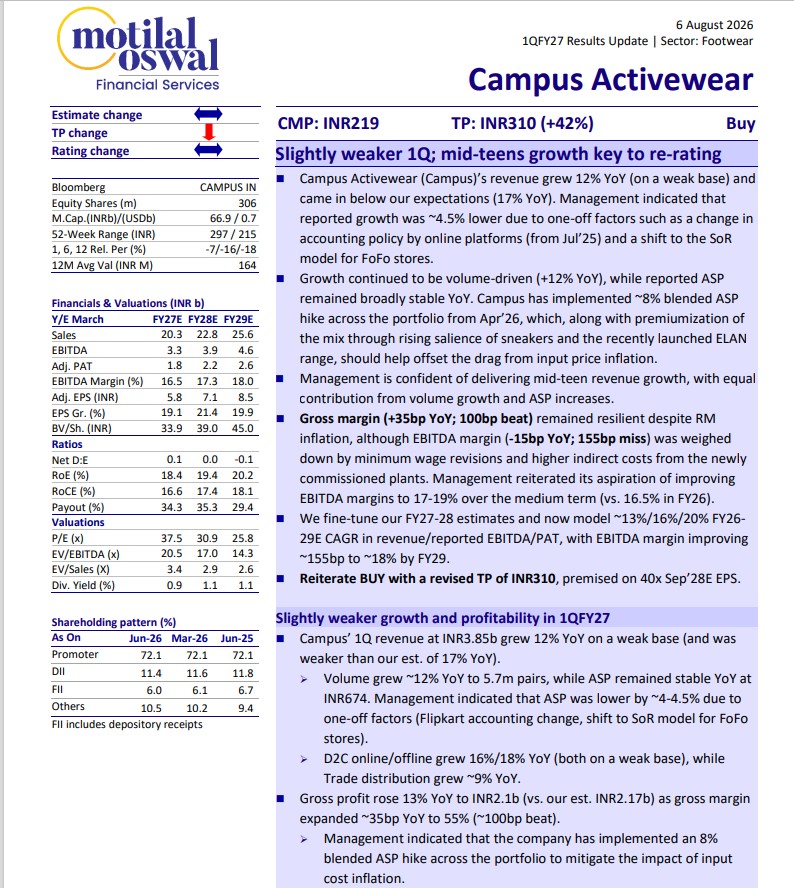

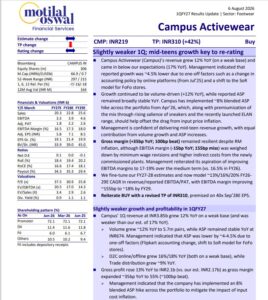

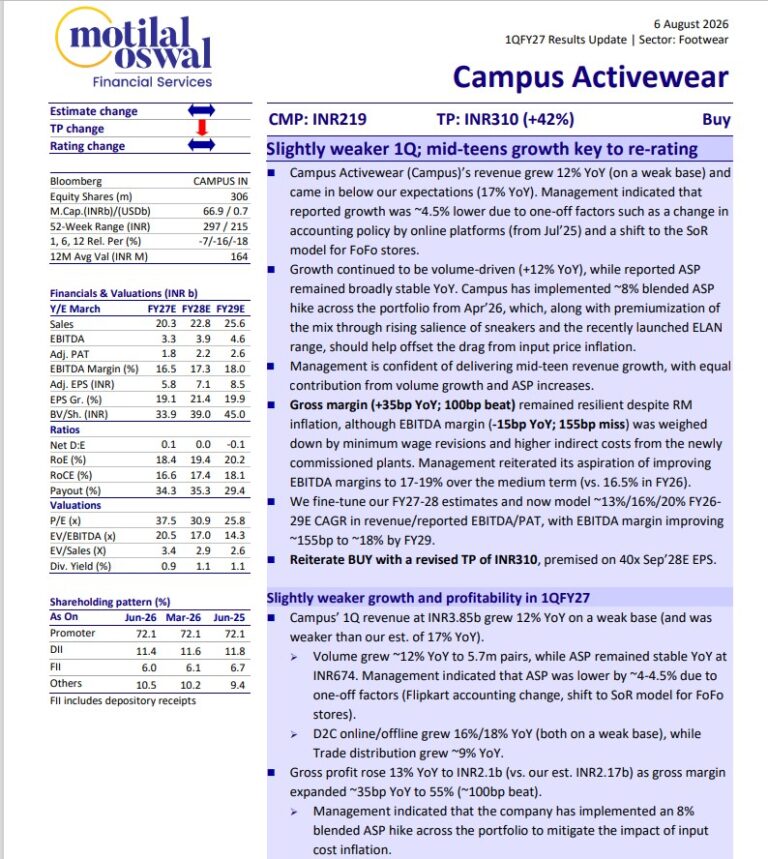

Campus is expanding beyond its core category of sports shoes into sneakers, women’s, and...

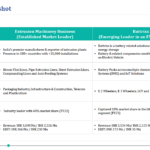

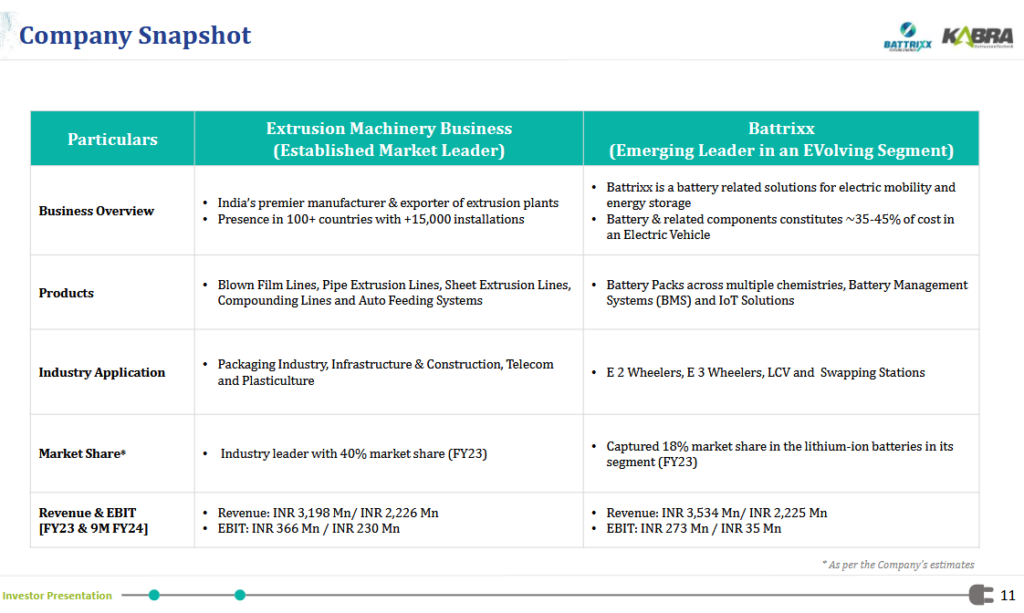

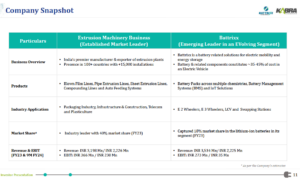

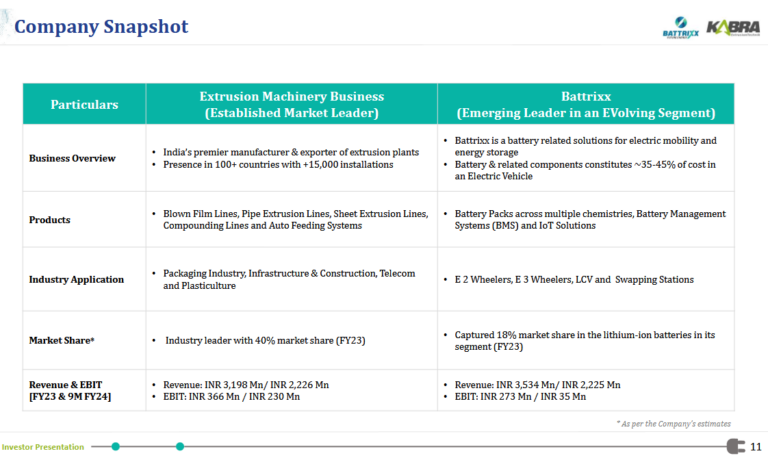

For the market, the key question now is whether Battrixx can evolve from a...

KRL’s legacy projects comprised 62% of FY26 revenues generating ~5% adjusted EBIDA margins (before...

Midcap and Smallcap indices also participated in the rally but underperformed the benchmark, reflecting...

JTL Industries Ltd is one of the India’s leading steel tubes and pipes manufacturers,...

we expect EBITDA margins to expand by ~550bps over FY26-28E, driving 52%/63% EBITDA/PAT CAGR...

We maintain a positive view on Tata Steel, driven by strategic expansion, higher value-added...

We believe improving hospitality margins, along with the increasing contribution from the commercial portfolio,...