Quant Mutual Fund's ₹175 crore investment reinforces institutional confidence in Ethos' long-term growth story.

Nemish Shah Bets ₹275 Crore on Blue Jet Healthcare, Sees Value in Debt-Free Specialty Pharma Company

Blue Jet Healthcare stands out for its strong balance sheet. The company is completely...

Global brokerage Citi has issued a 'Buy' recommendation on Kalyan Jewellers with a target...

Carraro is entering a phase where earnings are expected to grow faster than revenues,...

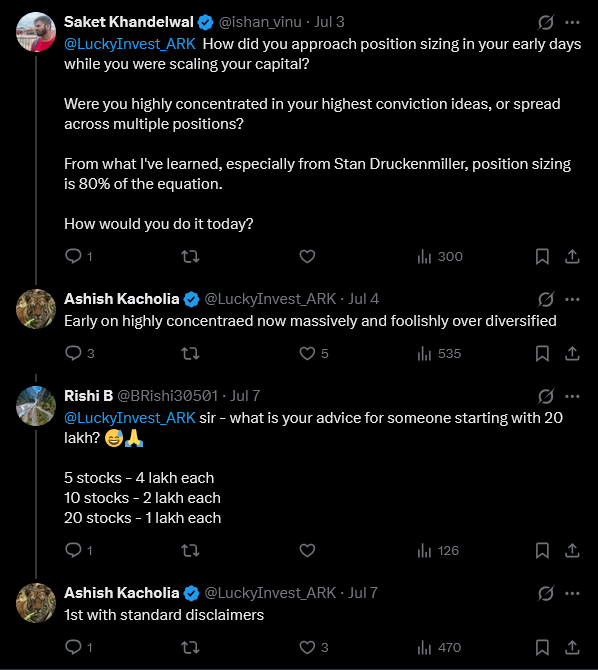

Concentrated investing is not suitable for everyone. Investors who lack the time, expertise or...

Domestic Pharmaceuticals growth has been impressive recently with the TTM May growth touching ~11%,...

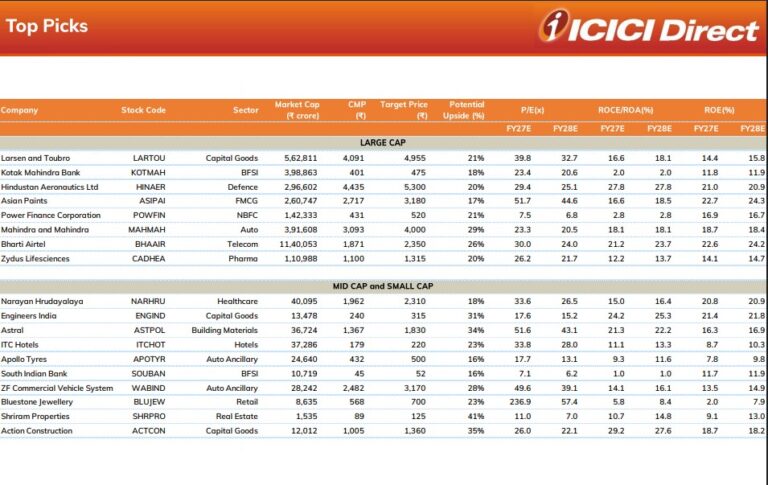

18 Top Fundamental Picks of July

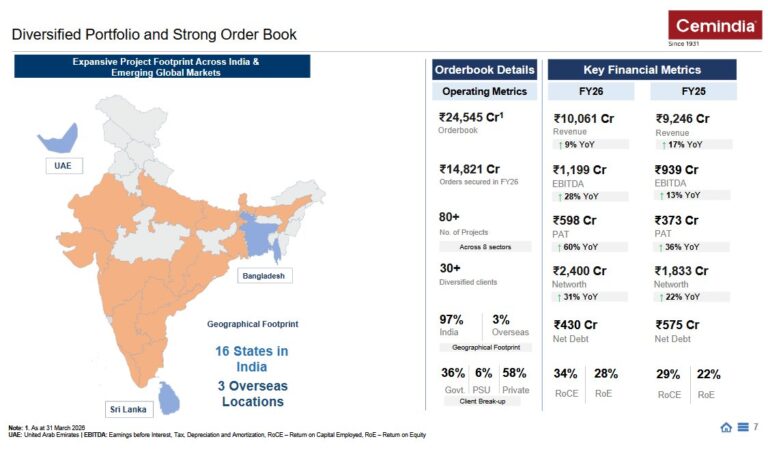

Madhu Kela's investment in Cemindia Projects is proving rewarding, with the stock doubling in...

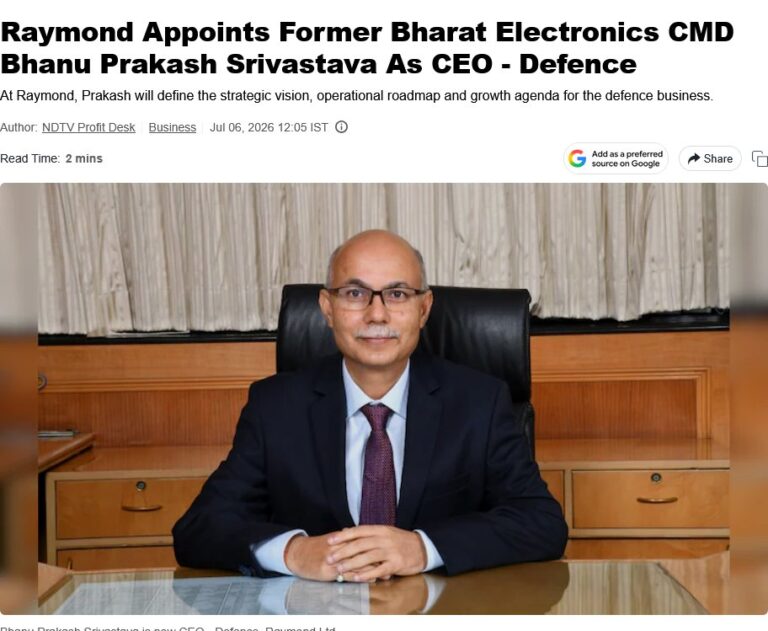

As India continues its push towards defence self-reliance, Raymond's latest strategic move could mark...

As Michael Burry's warning and CLSA's cautious stance indicate, the AI story is unlikely...