SDL is expected to clock INR 100bn+ in sales for FY26 (+70% YoY), supported...

investments

The sentiment among professional traders highlights a growing concern that such hyper-volatility, combined with...

The twin scandals have dealt a severe blow to IndusInd Bank's reputation. The bank's...

Kacholia’s investment reinforces the rising relevance of the recycling industry within India’s manufacturing landscape....

Kedia’s entry into Eimco Elecon has drawn attention to an otherwise overlooked mid-cap industrial...

The leading indices exhibited subdued performance throughout SAMVAT-2081 due to various challenges.

CARTRADE is well set to compound scale without stepping up CAC. We expect MUV...

Trading addiction is real. Talk to someone : a therapist, mentor, or friend. Focus...

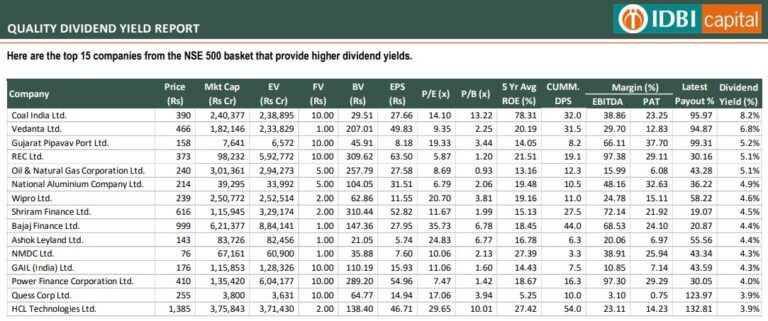

top 15 companies from the NSE 500 basket that provide higher dividend yields

When asked about his process for selecting companies, Kacholia outlined a systematic approach that...