Novice investors like you and me suffer from the misconception that micro and small-cap stocks are risky and dangerous investment propositions. This is why we have been investing our funds in blue-chip behemoth stocks.

However, we have paid a steep price for this because while the blue-chip behemoths are still lumbering in the hanger, the micro and small-cap stocks have taken off like rockets and are soaring in the stratosphere, giving multi-bagger gains to their investors.

We must also bear in mind that almost all of our favourite stock wizards such as Dolly Khanna, Vijay Kedia, Anil Kumar Goel, Brahmal Vasudevan etc have made a fortune for themselves by investing in top-quality small and micro-cap stocks. These wizards don’t touch large-cap behemoth stocks even with a barge pole.

We must also bear in mind the timely advice offered by Shankar Sharma to “Forget Large-Cap Stocks. Micro-Cap Stocks Will Give Upto 300% Gains”. Shankar also went out of his way to spoon-feed us with two micro-cap stocks, both of which have delivered mega gains to their shareholders.

However, Shankar also issued the chilling warning that the entire micro and small-cap sector is a “mine field” and that if we place our feet wrongly, we will have our heads blown off and suffer permanent loss of capital.

Fortunately, Peter Rabover, the fund manager of Artko Capital LP, with a proven track record for finding winning stocks, has provided valuable guidance which will help us navigate the mine field. He has prepared a check-list of five non-negotiable qualities that a micro or small-cap stock should have for it to qualify for investment consideration:

(i) The company must have high Returns on Invested Capital (ROIC):

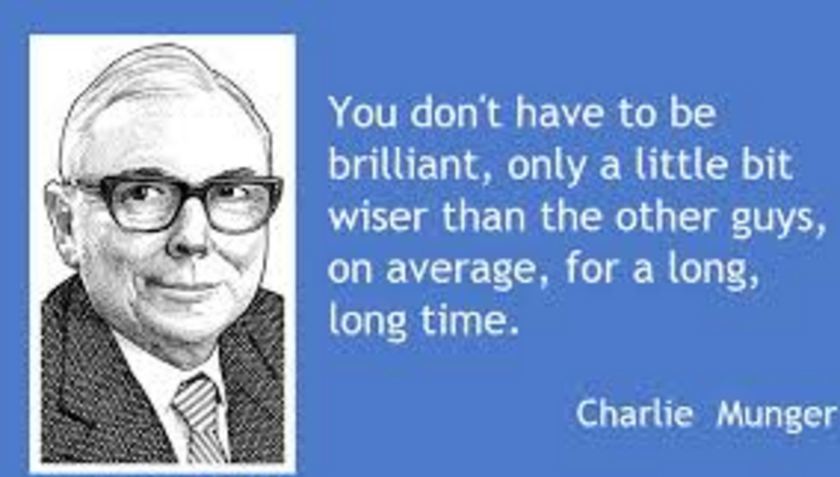

Peter Rabover quotes from Charlie Munger’s timeless wisdom that “Over the long term, it’s hard for a stock to earn a much better return than the business which underlies it earns. If the business earns 6 percent on capital over 40 years, you’re not going to make much different than a 6-percent return – even if you originally buy it at a huge discount. Conversely, if a business earns 18 percent on capital over 20 or 30 years, even if you pay an expensive looking price, you’ll end up with a fine result. So the trick is getting into better businesses. If you can find a fairly priced great company and buy it and sit, that tends to work out very, very well indeed.”

Peter Rabover advises that we must find good businesses that have consistent high returns on capital. A high ROIC generally goes hand-in-hand with a company with high competitive moats that allow the company to continue to earn outsized returns, he adds.

(ii) The company must have Quality Earnings and Consistent Cash Flow:

Peter Rabover emphasizes that over the long term, companies that can deliver consistent growth and low volatility in their earnings tend to not only perform well in the down markets but also command higher relative valuations in the up markets. He points out that quality-earnings companies tend to also have a consistent cash flow conversion rate in that they do not resort to accounting gimmicks such as pension accruals, “Big Bath” writeoffs, aggressive acquisition accounting or revenue recognition tricks.

(iii) The company must have a Clean Balance Sheet:

The third non-negotiable condition is that the company must have a low debt:equity ratio. While a little bit of debt in the capital structure is healthy and gives room to grow opportunistically, a lot of debt can lead to a lot of health issues.

Peter Rabover cautions that in addition to debt levels, we must also screen for hidden liabilities such as lawsuits, environmental or counterparty commitments etc.

(iv) The management must have high ownership of the stock:

Peter Rabover emphasizes that we must make sure that the management of the company is highly incentivized to create value. This will happen either when they own a significant ownership or when their compensation is structured toward creating value.

(v) The business model must be simple:

“Complexity breeds risk” Rabover says. He gives the example of a finance company packaging derivatives on obscure assets which is likelier to have black holes in its business model than a grocery retailer. We must be able to understand and explain what a company does in under a few minutes, he adds.

Now, the million dollar question that we have to work on is which are the micro and small-cap stocks that fulfill Peter Rabover’s description of winning stocks and which can give us multi-bagger gains?

question still remains unanswered to me

Good post. Highly informative

The last point summarises “The business model must be simple” exactly why Reliance has been a poor stock in the past ten years giving zero returns to its shareholders. The company is so complex (petrochemicals, refining, oil and gas, shipping, international trading, treasury management, Telecom, Retailing of fuel, groceries, Jewellery, lifestyle, you name it, Reliance is there. Jack of all trades. No analyst can analyse this company. Which is why the markets value this company at a junk PE. Just one company of the Tatas, TCS has market capitalisation of 1 lakh crore more than the market cap of all Reliance group companies of both brothers PUT TOGETHER. No wonder Buffet and Munger are the Gods of investment.

Dear Venky,

there is another reason why reliance lost trust of peopels .

Mass cheating they have done in previous bull run with RPL, RNRL etc …

Me too had good loss in that euphoria and learnt lesson, but then I promised myself I will neither buy reliance stocks nor any of their services in my lifetime .

Market do not forget so easily .

Thanks,

Prashant

I fully agree even No FII is coming close to Ril or any stock once you loose faith no one will trust. R com all show rooms closed pathatic service god knows what will geo do its nice that no one is touching even if it moves lots of people are waiting to get out.

thanks

viek

Not just RCom, Reliance Fresh has shut down scores of outlets, despite the business model predicted to be profitable by 2018, not a long gestation period. And scores of Reliance petrol pumps shut down for years. I can’t think why any major company will let it’s brand value erode so fast.

Fully agree with all above respondents to my note. Now just wait and see, Jio project will come to an end sometime in near future. Just wait for the NEXT big bang project. The company has an obsessive disorder with new projects. This new project they will announce will be world beating, record megascale project. The net effect will be its already 2lakh plus crore bank borrowings will now hit ten lakh crores. The shareholder will be made a fool again.

It is false that stock wizards dont touch blue chips. There are several blue chips which these guys have accumulated. It just doesnt show up in their portfolio due to the size. Dolly himself has stated that he has blue chips. There are several bluechips like HPCL, Indigo, IOC, Vedanta, Coal India, Hindalco , Tata motors etc which has given super returns in the last few months. several of them have even doubled in last 1year. Point here is to be opportunistic and not being fixed to just one market cap.

People has habit of searching ,we have HDFC bank,whih is giving steady returns for last two decades and it at continue to do so for atleast 5 more years.Similar is case of Kotak , Indusind,yesbank.Asian paints is giving steady returns,so is Lupin.But we want to invent Zero again ,so always in search of something new.

#Niveza #Review ::

The article is really worth. While picking any stock one should look at the business model first. Try to find as simple business as one can. Clarity in the balance sheet is very important. There can be fraudulent practices as well. One need to study with the risk point of view. Promoter holding should be checked. Consistent earnings should be in radar. Compared to peers, stock should be cheap. Valuation ratios are important as well.

Visit: Stock Market Tips

Currently it is rarely that a stock would be undervalued on these parameters. Every stock is rising …………..!