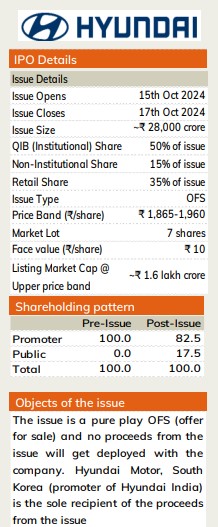

Credible play on tangible growth story in PV space…

About the Company: Hyundai Motors India (HMIL), is a part of South Korea based the “Hyundai Motor Group”, which is the third largest passenger vehicle (PV-OEM) manufacturer globally as of CY23. HMIL has for long been the second largest auto OEM in the domestic passenger vehicle market in terms of sales volumes.

• HMIL is amongst the top three contributors to Hyundai Motor global sales volumes, with contribution rising from 15.5% in CY18 to 18.2% in CY23.

• HMIL’s portfolio includes 13 models across major passenger vehicle segments including Grand i10, Aura, Verna, Exter, Venue, and Creta etc.

Key triggers/Highlights:

• Hyundai Motors India Ltd (HMIL) is the prominent and long-lasting player holding a significant ~15% market share in the domestic PV segment.

• Low penetration of passenger vehicles domestically offers long runway of growth, with HMIL well equipped to capture this tangible growth story.

• HMIL’s sales have been bolstered by the rapidly expanding SUV segment, which accounts for ~63% of its total sales, vs. ~60% share for the industry.

• HMIL flagship model, Creta, led sales in mid-size SUV segment, while the Verna dominated the premium sedan segment with ~20% market share.

• With a strategic focus on Electric Vehicle market, HMIL is aiming to launch four new EV models in India with Creta EV slated for launch by Q4FY25.

• Tactical capacity expansion with acquisition of Talegaon plant (~2.5L units)

• Capital efficient business model (RoE, RoCE: 20%+) with cash surplus b/s.

Our View & Rating

• Sales/PAT at HMIL has grown at a CAGR of 19.4%/47.7% respectively over FY21-24, led by 11% sales volume CAGR and consistent improvement in EBITDA margin profile. HMIL clocked EBITDA margins of 13.1% in FY24 with RoCE placed at 50%+. At the upper end of the price band, HMIL will command a valuation of ~26x P/E, ~16.5x EV/EBITDA & ~2.3x P/S on FY24 basis which is at a tad discount to industry leader i.e. Maruti Suzuki India.

• We assign SUBSCRIBE rating on HMIL given steady growth prospects amid industry tailwinds, robust financials & healthy SUV product slate. We expect limited listing gains to this IPO, however expect HMIL to deliver healthy double-digit portfolio returns over medium to long term.

Key risk & concerns

• High quantum of related party transactions with presence of sister company Kia in similar segments may lead to potential conflict of interest.

• Regulatory led rise in ASP’s and consequent pressure on volume growth.