AVL_1.pdf (443.6 KB)

The company aims to raise funds by issuing up to 7,90,405 equity shares to selected buyers at a price of ₹3,573.17 per share, totaling approximately ₹282.42 crore. Name if investers are

(a)SMALLCAP World Fund, INC

(b)American Funds Insurance Series Global Small Capitalization Fund

Posts in category Value Pickr

See the bright Sun: Aditya Vision (30-01-2024)

MPS Ltd (30-01-2024)

Two soft instances from Q2Fy24 call:

-

The way Rahul flaunted that he became CEO at a young age of 31 and then followed this by over-emphasis on this pedigree, being a alumni from Wharton & Harvard. It sounded un-necessary to talk about this to answer the point around evolution of the mgmt, company.

-

The way he flaunted that their PAT target of 130 cr in FY24 is a done deal (& it was supposedly a extremely conservative guidance, which now they may even miss) & how they have over-delivered wrt guidance in the past. Also, he went on to entice the investor to extrapolate the guidance based on their past. Mgmt needs to be humble in my view. In a business, nothing is certain given so many known, unknown variables to be managed. To me it was a sign of over-confidence, arrogance.

Note: This is my own personal way of assessing leadership both within my organization as an employee and as an investor. Hence others may have completely contrary reading of such instances.

Usha Martin- Coming out of Chaos (30-01-2024)

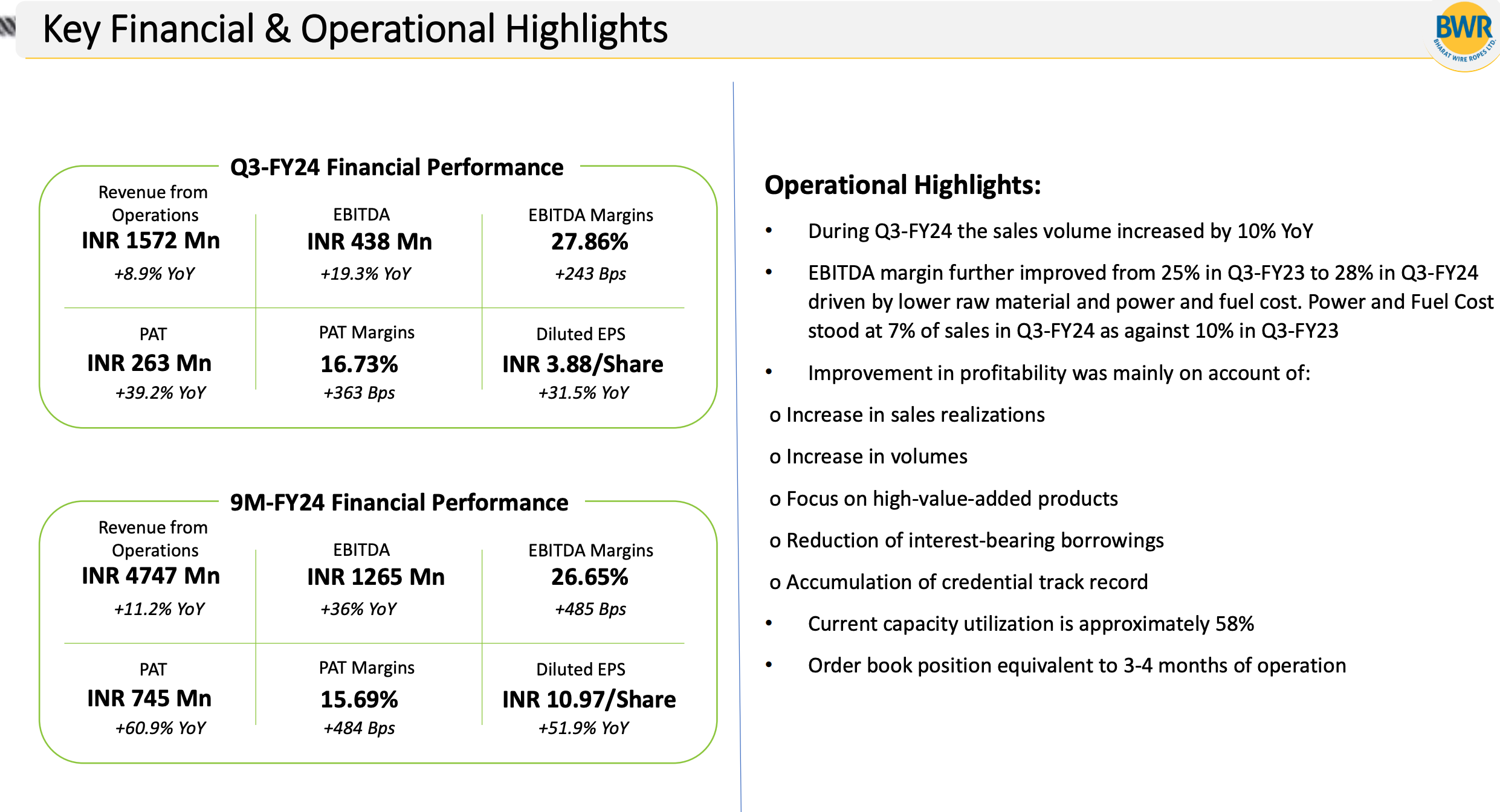

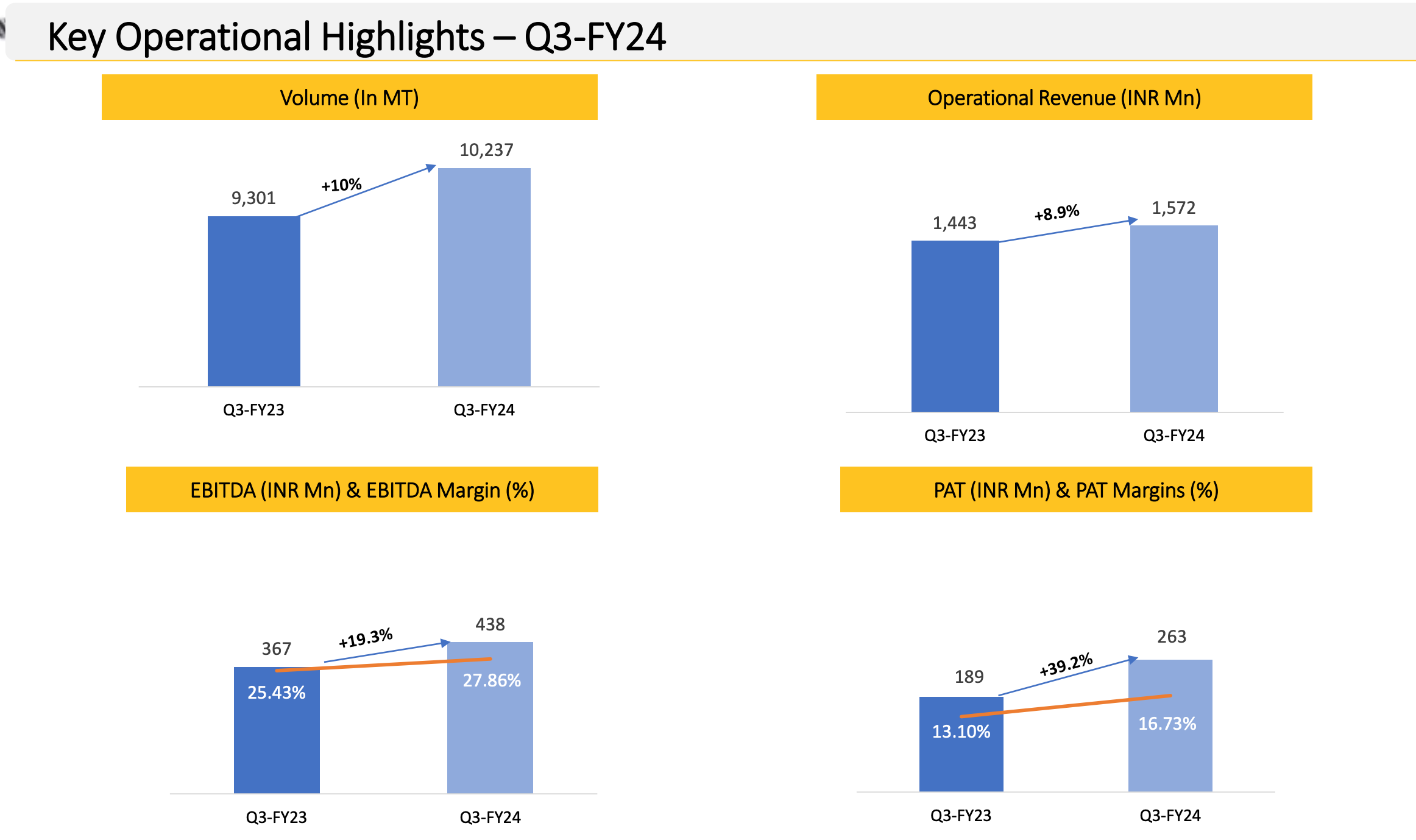

Some insights from Bharat Wire Ropes Q3FY24.

Organized scrappily to save time. Source: [Concall Q3FY24]

Sales mix and customer insights

80% of revenues from exports. Most of the products are sold through distributors. Management could not ascertain which sectors were driving the demand. The commentary was generic – “getting good traction from all sectors”. Mgmt indicated they don’t have unique SKUs for different applications such as O&G and Marine.

Growth: Steel and product prices declining over the last few qtrs. Volumes have gone up. The company is increasing its global footprint, distribution, and working on new product lines. Expects 20% of revenues from special ropes in the next 2-3 years.

Cap utilization

- The strategy is to increase cap utilization from 60-65% to 80+% by de-bottlenecking.

- This will cost 25-30 Cr over the next 18-24 months.

- ROCE/Asset turns on capex: No clue.

- Capex: Only on the drawing board.

Competition: No clear answers on competition and the supply scenario.

Current order book: 150 cr, 2-3 months

EBITDA margin expansion over the last 2-3 years: We’ve achieved these numbers by putting numerous efforts – sales efficiency, product mix, cost controls. This business is asset heavy and asset turnover is low.

Q: Why are you being conservative?

A: Wire rope is a conservative product. Buyers don’t switch brands easily. We’re continuously adding new customers and products. We’re participating in conferences and exhibitions at global level.

Disclaimer: Invested

Tata Investment Corporation: Unusual discount to NAV (30-01-2024)

Today, I sold my largest holding in my portfolio, which I had held for over three years. The reason for selling was that the discount had narrowed to almost nil and the largest holdings held by Tata Investment Corporation, such as Titan, Trent, Tata Consumers, etc., are very expensive, which in turn made this stock even more expensive to hold. Although I was hesitant to sell at the time, I may have been emotionally attached to this scrip. Now, I am looking for alternative investment options for the proceeds from the sale.

Sky Gold ltd. – Will it reach the sky? (30-01-2024)

Fundamentally the company does look strong and poised for growth but what sets it down is the amount of stock price manipulations that have been happening lately.

Disc.- Invested

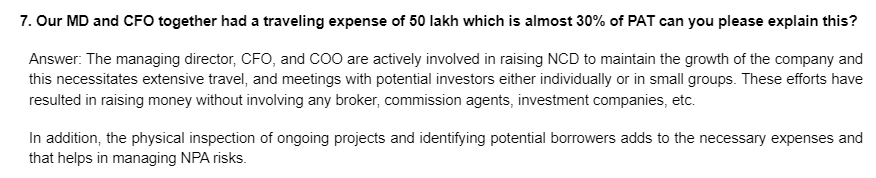

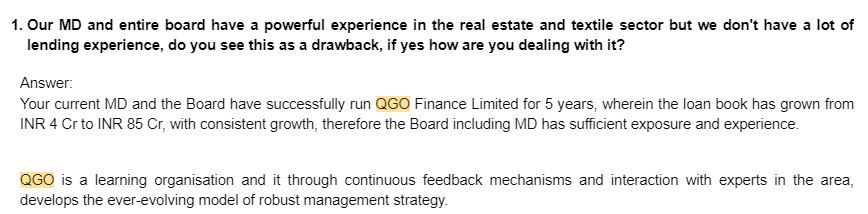

QGO Finance Ltd (30-01-2024)

my sense is that they have not scaled the business despite being in business from so many years, So the are doing good business, growing slowly, having good salary, and looks like everything is being done by management.

The have not done very good with delegating work or they wanted the business to be in their full control and run it in a natural way. My intuition is once they come close to retirement and by the time if they can have a 200cr to 300cr AUM they can basically sell the business.

The aspiration to scale is not very high. Please note all this is just personal opinion, how I came to this conclusion, please find the answer below

if you see the balance sheet from 2018 they have been growing, now relatively it looks huge but if you see in absolute terms that is around 12cr to 14cr increase every year.

So either they have the inability to raise funds or they don’t have the capability to handle more growth or they don’t want to grow

Why capability because think about this way if I have to do the du diligence of lender, I have to raise money, I have to do the collection and also look into operations, if everything has to be done by one or two guys then it is beyond the personal capacity to do lot of business.

So you can see from this answer that basically CFO has to do everything + they are a very small team despite being in business for so many years

The promoter of this business also have previously built business and sold them so this is like their last project or something.

So entire experience is around real estate, so if you think this way, they are raising every year some money, lending it, scaling it at their own capacity and making money.

Nothing wrong in this at all but look like they are satisfied and content.

One last point I forgot to mention is, they pay divided, so this makes me think the business has matured and growing decently and promoters have or are sufficiently meeting their financial aspiration in life.

PLEASE NOTE– All this is story telling, I don’t now the promoter or I have never met them, I am not a shareholder, the screenshot are the reply from the company, which I asked during AGM, I can be horribly wrong and they can still give fantastic result and keep growing in future, I am naive kid.

Thankyou

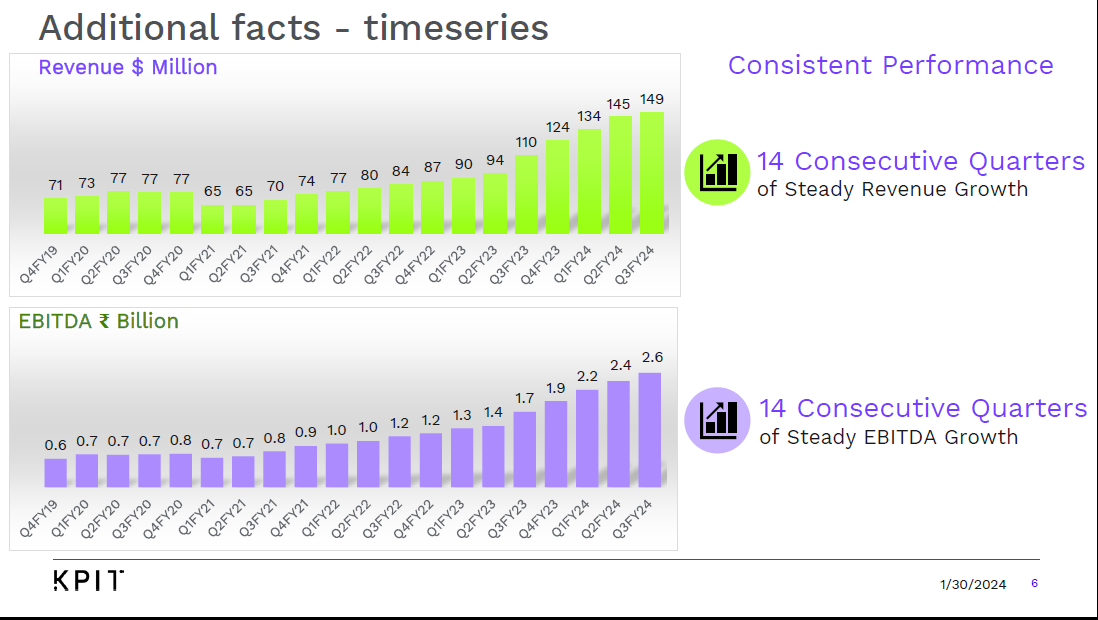

KPIT – CASE (connected, autonomous, shared, electric) – Focused Automotive Play (30-01-2024)

Another great set of results by KPIT…Story keeps getting better and better

Tata Investment Corporation: Unusual discount to NAV (30-01-2024)

Is there a specific reason except for the results for this move, it’s going above its book value ?? Don’t understand how can that be , anyone is aware or has a thesis??

QGO Finance Ltd (30-01-2024)

Does anyone here following this nano cap? QGO is doing well in every consecutive Qs.

I just bought a tracking position.

Investing Basics – Feel free to ask the most basic questions (30-01-2024)

Hi,

what does positive cash flow from inventory represents though the inventory in balance sheet has increased.

Is it generation of cash by selling inventory?

Regards