Hi,

Seems like the older members are not active anymore. I have just created a whatsapp group for Valuepickr Ahmedabad. Lets discuss and organize a meetup.

If you want the link for this new Ahmedabad/Baroda group do message me.

Hi,

Seems like the older members are not active anymore. I have just created a whatsapp group for Valuepickr Ahmedabad. Lets discuss and organize a meetup.

If you want the link for this new Ahmedabad/Baroda group do message me.

The market appears to be taking into account the future earnings per share (EPS) generated by the inclusion of new plants in Chennai and Mundra. This anticipation has led to a perceived reevaluation of the company’s market capitalization. Currently, the stock is trading at a ratio of 1:1 in comparison to the market capitalization to revenue, which seems relatively lower compared to industry peers. The addition of these plants is expected to contribute positively to the company’s overall revenue, and investors seem to be factoring in the potential impact on the stock’s valuation.

Thanks for mentioning this! I think I could’ve worded it better.

What I meant was, most of the times, companies may track you without really knowing it’s you, with the ultimate goal being a “conversion”. (for eg. by cookie syncing). Affle may or may not be able to legally sell user data, but it’s probably not in their best interest to do so given the value and importance of first party user data to their own platform.

Hello everyone,

I’ve been tracking this company since it’s share price was around 250 levels, have sold most of my holdings at a good profit.

Thinking to reinvest, is this a good time to enter, considering the opportunities available in the near future?

I am forming a new whatsapp group for Valuepickr Ahmedabad as I think the admin of this thread is inactive from last many days. Anyone from Ahmedabad can ping me and we can schedule offline meets.

No email, this is from the concall

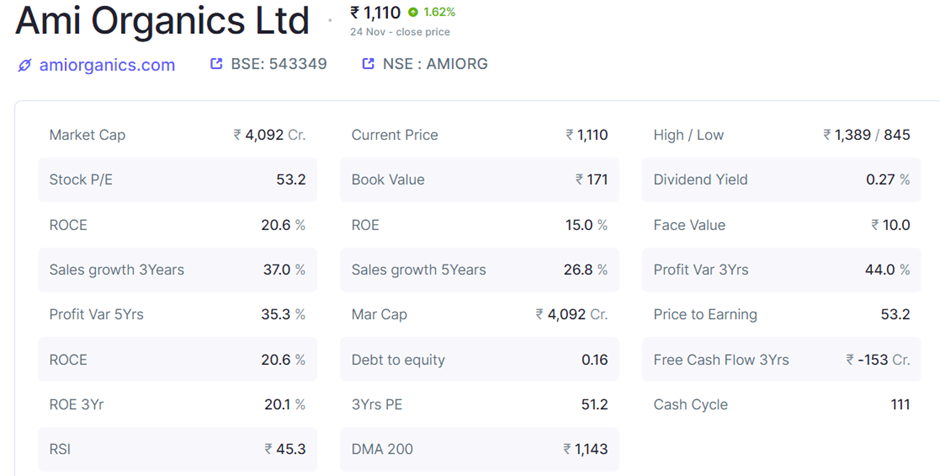

My notes on Ami Organics:

Source: screener.in

Summary rationale: I bought Ami Organics Ltd’s (AOL) just last week (24th November) making it over 5% of my portfolio. On the face of it stock looked expensive at over 50PE, however given the growth opportunities and its presence in sunrise industry (EVs and semiconductors) it looks reasonably priced.

My thesis on AOL is mainly based on three key opportunities:

*Assuming cost of intermediate accounts for 5%. The cost of Acetaminophen which is used in paracetamol tablets like Dolo 650 is about 15%.

Electrolyte additives: AOL has developed electrolyte additives which are used in lithium batteries to increase the life of the batteries. Market size for this is estimated to be over USD1 billion and likely to double to USD2 billion in the next 3 to 4 years. AOL aims to garner 10% of this market which puts its revenue potential to about 1600 crores annually by end of 2030.

Semi-conductor chemicals business: AOL recently in Q2 FY24 acquired 55% stake in Baba Fine Chemicals (Baba) which is semiconductor chemicals. AOL aims to take Baba’s revenue to over 200 crores by FY25. This is a high margin business with EBITDA margins in 40% range vs. current AOL business in 20% range.

In addition to above, AOL continues to launch large market size products like UV absorber, and has maintained that further contracts with Fermion are in the discussions. All the new products are likely to support margins and operating leverage is likely to result in margins in 25% vicinity from current range of 20%. Currently margins are somewhat depressed as the company integrated Gujarat Organics plants over the last two years which exhibited very low margins.

I have modelled two scenarios

Opportunity based:

and,

Capex and management guidance-based scenario

In above two scenarios my worst return expectation by FY28 is likely to be 20% CAGR in scenario 2 (capex and management guidance based) with PE derating to 30. While best return expectation is likely to be at 43% CAGR in opportunity-based scenario with re-rating to 60 PE.

Right to win:

Though some of the risks to above estimates are mitigated by first mover (outside China) advantage, exclusive agreements and India cost advantage, we still need to account for below risks:

Customers:

Company caters to major domestic and overseas MNCs.

Source: AOL Q2 24 presentation

Peers: Divis Lab (APIs), Neogen and Neuland.

Thanks

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation.

True. Still holding and adding small quantity once in a while. What baffles me is the way so many stocks have gone up with & without justification of fundamentals, while this one moves very slow. Makes me wonder if this is artificially done for the sake of accumulation

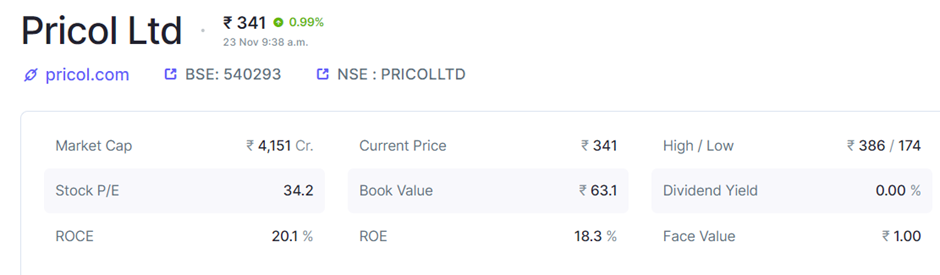

My notes on Pricol:

Source: screener.in

Summary rationale: Pricol was on my radar for last 6 months but now with about 12% correction I became interested. Price corrected post soft Q2 24 results. However, management continues to guide ~4,000 crore revenues by FY26 and some margin improvement (~200bps over next two years). Back of envelope calculation showcases about 35% revenue CAGR and profit growth well above it. LTM PE is 34 which means company is available at 1PEG*. I find companies less than 2PEG attractive.

*PEG: PE (price to earning multiple) to growth ratio.

DIS systems used to be in 200-300 rs for per vehicle now they are priced at 1200 per vehicle (2-wheeler). With increased digitisation and more sophistication these products are likely to go in 2000-2500 rs range over the next three years, as per the management.

Other triggers:

Right to win:

Risks:

Products: Pricol makes driver information system (65% of revenues) and actuation, control and fluid management system (35% of revenues).

Source: Pricol Q2 24 presentation

Customers:

Company caters to all major 2wheeler, 3wheeler, commercial vehicles, tractors manufactures

Source: Pricol Q2 24 presentation

Competitor: Minda Corp

Thanks

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation.