A small addition, One peer that outperformed them all is Redtape Ltd. whose Sales grew by 28.7%.

Posts in category Value Pickr

Va Tech Wabag (03-10-2023)

Thank you for your analysis! What can understand from this is if they get their act together and focus on doing more EP working rather EPC with better margins we could see earning and PE expansion both

HDFC Bank- we understand your world (03-10-2023)

I believe that, Banks should start using AI capabilities more seriously than present, to tap the right customers which are actually looking for Loans and Credit Card products, rather than randomly calling all customers for marketing Loans & Credit Cards.

Currently Axis Bank seems to be calling every week to sell such products. (This is my own personal experience and also shared by few of my friends). Here there is scope for massive improvement.

I have seen that, some younger customers who need Education Loans may not get it so it seems that, there is some gap between demand and supply.

If banks can plug these gaps, they might able to reach correct customer base.

Note : This is general observation and not related to specific bank.

Invested in HDFC Bank since 2011 onwards.

IDFC – Infrastructure Development Finance corporation (03-10-2023)

I dont see any risk on buying IDFC.

Note: I have sold IDFC First bank and bought IDFC

KPI Green- Turning Sunshine Into Cashflows (03-10-2023)

A new order of 7 MW has been received, which I estimate should be worth around 30cr.

IDFC First Bank Limited (03-10-2023)

I partially agree with your point but partially have different view.

I do not believe we HAVE TO invest in financial stocks just because financials form large part of our index / total mcap. My personal belief is invest where we can make money. Please note I have nothing personal against this bank. I am part owner too ![]()

I agree finance is big part but banks are looking lucrative only because of all the deleveraging that has happened post covid shock. All the banks have strong balance sheets. Corporates have reduced debt considerably (at the cost of low private capex). Now when the private capex pick up, bank will lend more and there will be growth. But for how long? 3 yrs? 5 yrs? Some day the party will stop. Its a cycle.

I find this statement very optimist for the reason mentioned above. Past 3 yrs went in balance sheet cleaning (for banks and corporates). Government did all the heavy capex. Private will pick up (may be post elections). So there can be growth for next 2-3 yrs. but the competition is equally intense. Currently, the bank is strongly placed to make the most of coming growth but future is uncertain. Its hard to decide right now to hold it for decades (my personal view).

Can you please suggest how did you calculate this BV ratio? according to me, current multiple is 2.4 (price 94 / bv 39).

by giving this multiple, you are placing the bank in the leagues of HDFC & ICICI & Kotak. ![]()

I agree with all these triggers. But don’t you think rerating has already happened? I believe price has run up the fundamentals. Now bank will have to deliver on all these parameters to ensure the current multiples sustain.

Once again: Nothing against the bank. I have invested in it too. All I am saying is be extra cautious. Borrowing analogy from @Worldlywiseinvestors , we are riding a tiger here. tightly pakad ke rakhna.

SmallCap Hunter : Trying to find the dark horses with triggers (03-10-2023)

@avneesh @ajayt001 @StonePitbull @Nickp @ChaitanyaC @jitenp @vikas_sinha

Based on my interests into small caps news/threads, hoping to learn more.

Many news on small caps is more or less summarized at The below VP discussion comparing PPFAS flexi funds vs small cap funds. (which largely based on recent presentation by PPFAS funds)

PPFAS supports large caps and references an IIM-A study suggesting small caps didn’t outperform large caps from 1995-2019. Some argue PPFAS might criticize small caps due to not having a small cap fund, even though historically small cap funds have given around 20% returns over a decade.

However, historically, when a lot of money pours into small caps, they tend to go down heavily with a slight market correction. Small cap funds usually follow a pattern: 2-3 years of a rally and then 1-2 years of a gloomy period. This aligns with Howard Mark’s book on market cycles, indicating we’re currently at the peak/getting to the peak of a small cap funds rally.

My query is regarding small cap stocks for a retail investor(who is 93% small caps), how one can wade through these situations.

1.If we can not time the exact top, what could be time frame to run, Diwali-23 or July-24? what time frame do you feel is comfirtable before it gets gloomy?

2.What can be considered a cautious approach, if we are not sure about running away, e.g. can take off partial profit?

.

Metro Brands – marketing footwear (03-10-2023)

I was reviewing my small holding in Metro Brands.

Metro posted 14.68 % growth in sales in the June quarter, lower than past quarters but better than most other peers. For example, Relaxo grew 11 %, Bata 2 %, Campus 5 %. I think 14 – 15 % is what its natural long run organic growth rate should be, though market growth estimates appear to be much higher. Gross margins have remained close to 58 – 60 % range in recent times. Operating margins around 30 %. Excluding Cravatex, operating margin was almost 35 % in the latest quarter. This is where Metro’s efficient outsourcing model makes a difference. Peers like Campus, Relaxo and Bata have margins in the range of 15 to 20 % but not higher. Metro’s return ratios like ROE & ROCE also continue to look good, in the 25 % range. Balance Sheet remains debt free, other than lease liabilities. Promoter salary is reasonable, at around half a percent of sales. Dividend payouts are in the range of 25 to 30% of PAT.

In FY23, store addition was the highest, and the pace has continued in Q1 FY24 as well with 27 stores added for the 3 months. This will support sales growth going ahead. Average sales per store is now more than Rs.3 crore per store, its highest on record.

The main operating cost in retail businesses is inventories. Not only inventories can be high, one does not know what they are really worth. But Metro has controlled inventories well. I understand for most of the Third-Party brands, Metro pays for the products only when they are sold, inventories are not on Metro’s account. This is such a good thing, given Third Party brands constitute a quarter of the company’s sales. New BIS Norms coming into play from 1st Jan 2024 will increase inventories, the company has said. Need to see how much this goes to.

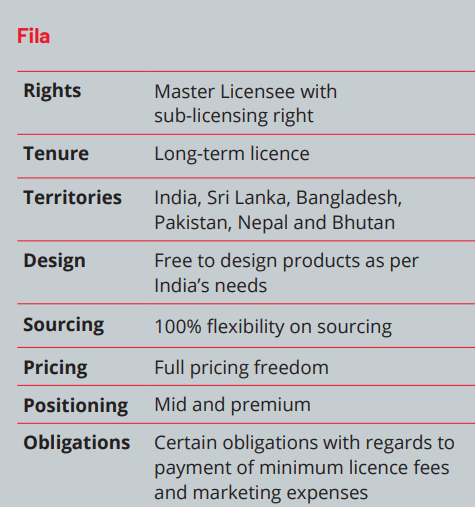

Last year, June sales were around 25 % of the full year sales. If the same ratio holds for this year as well, the company will post a full year sales of Rs.2400 core for FY24. This is excluding new additions such as Fila. Overall, Metro leaves little to complain other than valuation. The stock has always been expensive and has become even more so in the last one year.

So there is a lot riding on Fila, clearly. The Cravatex acquisition cost Rs.200 crore, consuming a large part of the Rs.300 crore raised through the IPO. The biggest brands in this space are Adidas, Reebok and Puma. As per reports, Adidas and Puma have been selling more than a Rs.1,000 crore per year each. Adidas makes around 17 % ROCE and Reebok 27 %. Metro has not announced its store opening plans for Fila yet, but when fully rolled out, Fila will clearly make a big impact on Metro’s numbers.

Metro is planning to position Fila in the Rs.4,000-plus segment, which is significantly premium than at present, with 300-400 stores for Fila alone in the long run. Besides this, Fila will also be available through 500-odd Metro & Mochi stores. The company will also sell Fila accessories and apparels, besides footwear, besides the Proline range. Fila rollout will also see a sharp spike in costs I think, both for branding & promotion as well as operating costs. Fila will be sold entirely on COCO model. And then there will be license fees, about which the company has not revealed anything so far. For the long term, the sports footwear category is growing at 25 % per annum, faster than all others. The full Fila impact will come in FY26, not before. Even the analyst estimates for FY25 do not justify current valuations.

(Source: Trendlyne)

I think market is pricing in a Rs.1,000 crore revenue from Fila in FY26 probably.

TAAL Enterprise – cheap valueations (03-10-2023)

TAAL AGM FY23 updates from Sept 26th 11am. This was compiled by a fellow shareholder (Yash), posting on their behalf. Thank him for sharing the notes in such a detailed manner.

Chairman speech:

- Engineering design capabilities: company is on a robust growth path.

- Merger of the subsidiary: there will be no dilution since it’s a wholly owned subsidiary. The rationale is to simplify the structure. The merger should be completed by Q3FY24.

- Registered office has shifted to Bangalore.

Q&A speakers – Rohit Balakrishnan, Ashwin Dsouza, Rupesh Tatiya, Swechha Jain, Keshav Garg, Aayush Agarwal

Questions answered by MD: - 3 areas: product design, construction, and infrastructure (architectural) and plant design (work for EPC companies).

- 60+ customers today. Number of customers have grown and business with each customer has grown.

- Largely exports business. 70% US & Canada, 21% EU. Trying to make entry in Japan and Middle East.

- No work for the defence sector in TTIPL.

- Expect to retain the growth rates of the past.

- Margins: built the business in that way. Have been very selective with customers. Margins are fluctuating because on site business has grown faster than offshore business. Over the longer-term margins will smoothen out.

- Invested in sales and marketing team. Will pay dividends in future.

- See good growth in all segments going forward.

- Unlike KPIT are not automotive focussed.

- Hired senior management particularly in the sales side.

- Both the office are operating at full capacity.

- Roughly 690 employees.

- Have master service agreements and then get PO which are short term. Don’t have LT order book.

- Top 1-5-10 customers: 13%-43%-60%.

- Half to 1 million dollar is average ticket size.

- In the EPC space don’t work for end customers. For other segments work with end customers.

- Don’t have any aircraft. Entire business rests within the subsidiary and hence the merger.

- Competetiors: many in Germany and France. Cyient, Axiscades, KPIT to some extents are competitors.

- Recruit people based on orders don’t keep a bench of people.

- 106crs of financials assets: FDs, Investments, Bank Balances are major.

- 45% product engineering, 25% plant engineering, 19% construction, 1% IOT services.

- Subsidiary Amalgamation NCLT Final hearing is 8th November 2023.