Posts in category Value Pickr

KP Energy – Lotus in muddy water (29-07-2022)

Is anyone still following this company? Can anyone explain the recent development of the result of Gujarat High court for petition filled against the company.

Thanks

E2E Networks Ltd – Listed small Cloud computing player (29-07-2022)

The no. of equity shares is relatively low. Jusr 1.45 cr. This will give per share sale of ~35 Rs. P/S comes to around 3.8. If we consider the latest quarterly report annualized, which is safe to do as the sales have consistently grown QoQ from 2020 onwards, annual sales will be 60cr (15cr Q1 FY23) This will give an sales per share of ~41 and P/S of 2.9. Based on these numbers it’s not too cheap and not too expensive either.

The thing imo is that no one invests in this microcap stock keeping in mind the current numbers and stats. This is too risky a bet to make sense of via current performance. This is a bet/speculation on the future potential of this business. Different people have different ways of arriving at that future value but it’s potential value all the same.

Personally I am holding from price of 65 and not expecting any big upticks anytime soon unless some hanky panky stuff plays out. But I’ll bestaying invested all the same.

Valiant Organics – High ROCE, debt free (29-07-2022)

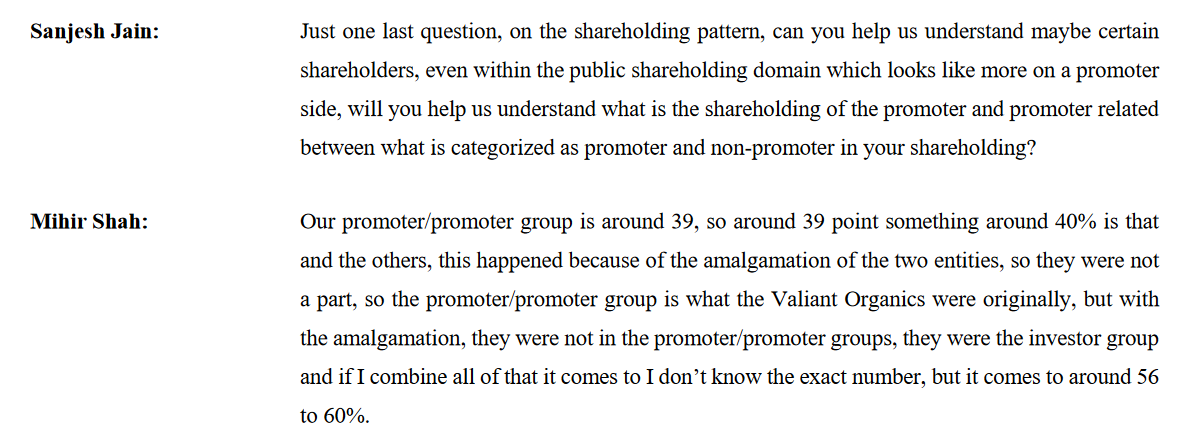

Adding on this, I was going through the last concall transcript (Link) and found the below snapshot as relevant

Initially I had assumed the selling as some form of internal adjustment while others picked up stake and now this realignment of shares seems to point to that.

Godawari Power – Any Trackers? (29-07-2022)

Can you please confirm where do you see 1000 crore cash balance by mid-term results? I couldn’t find it in screener or in the presentation

IDFC First Bank Limited (29-07-2022)

I see a lot of TA around stocks here but for consumer facing entities like IDFC First Bank, I see very little appreciation for the consumer-centric approach that VV adopts at every step of the consumer journey. It’s a qualitative factor and perhaps the most important one. Would love to see someone perform an analysis on how consumer-centric the bank’s products and support are. Just to remind this forum, VV ‘thought of a better bank’ after his outstanding stint at ICICI Bank. Imagine the learnings, if you can. We’re looking at the WIP of something better than HDFC and ICICI here. There will be hiccups but the overall vision and commitment to the vision cannot be ignored during a fundamental analysis.

CarTrade Tech – A Multi-Channel Auto Platform (29-07-2022)

I have this question, cartrade has about 1,933 crores in book. is this entire amount parked into fixed deposit and if so what is the mode they paid back? Is it paid yearly or quarterly? In the current quarter I see 9 crore+ in other income category. Does it mean this other income is the credit intrest they received from parked money ? And is it is fair assumption to consider runrate clock is 36 Cr fr an year term.

Godawari Power – Any Trackers? (29-07-2022)

No, it doesn’t sell Iron ore

Yes bank (29-07-2022)

To be very honest i am disappointed by the price. It comes around 14.25. They could have raised capital after 3 to 6 months and got better valuation.

But something is better than nothing. These two firms will be board member and this capital will help in growth. Let me put some calculations below. I know business don’t work mathametically that is why i am going to back each of my calculation logically.

After this capital raise. I feel it is going to be $1 billion don’t know why they are mentioning 8900cr. Let us go with $1 billion.

This allows yesbank to give advances worth 44000cr at 18% CET.

Next 2 years profit till FY24 let’s assume 5000cr. Now i feel this is on lower side because yesbank PBT will be added to book value not PAT because they have 9000 cr tax asset. Even this quater their book value was up by 420cr. So this helps in lending 28000cr.

Their asset size will go down by 20000cr by transferring to ARC. So they can lend this 20000cr as well.

Till next capital raise a total of 92000cr can be disbursed. Note i have not accounted for recovery. For lending 92000cr bank needs minimum 1.2 lakh cr on liability side. So till the time yesbank becomes 4.2 lakh cr size there won’t be any dilution. I feel they can reach this size by FY25 end it is difficult to achieve before that.

Currently yesbank cost is very high close to 78% cost to income this quarter. This cost will be same till this year end because they are doing heavy investments to change their entire mix. This change in advance mix requires heavy immediate investments but the revenue you generate for this would come in later years. This was mentioned in con call as well.

I spoke to some senior yesbank employee today and what i got to know that during ravneet gill time employee were scared . Corporate culture was bad. They were working like PSU but since prashanth kumar had come things are changing. All guidance give for Fy21 were met. It takes time to change and that is what yesbank is doing. He also said that despite being in yesbank for 3 years he does not know the role of few departments( I mean how are these people even contributing to the bank). I am also customer of yes security and i have never seen such horrible service in my life. What i am trying to say is to change all these things it takes time. They sold their MF last years and slowly slowly cleaning is happening.

Coming to the point. On 4.2 lakh cr for a well established bank and under good leadership i belive 1.5% ROA is achievable. So 4.2 lakh cr and 1.5% ROA and 3200cr shares. EPS of around 2 and PE OF 25 so price of around 50.

The whole game lies in the 1.5% ROA which again i think is achievable because of they being more towards retail side. I have dealt with 10 banks till now in the last 2 years as customer and only KOTAK AND YESBANK have something called as relationship manager at every level. My dealing with bank involves lot of activity so i understand the efficiency to some extent. Just to name a few like(PIS OPENING, INWARD/OUTWARD REMMITANCE/NRE KYC UPDATION/BROKER ACCOUNT OPENING/BRANCH SHIFTING. just try changing your mail id in sbi and see the pain you go through. Yesbank was at that level. The comfort i have got here is better than any of them till now( this is personal experiance might be different for others).Many might contest that other banks also have but the true meaning of this position is being fulfilled by these 2 banks only. That is why they have 25k employee. All these small things make a big difference in future.

Even if the price is 35 or 40 by FY25 and you bought it at 12 just see your CAGR. I am very confident of their growth. Let’s see

The biggest asset of bank is their employee. Slowly slowly there is pressure from higher management. Employee are meeting sales targets. Inefficient departments are being removed. The complete corporate attitude is changing. Since this is 85% of my portfolio i am tracking this every second and pretty confident as of now. I have demanded the mail Id of the CFO of the bank and have very important questions. If i get that will be sharing with you more details with better clarity. I know CFO himself doesn’t respond and his team does but that will also be big.

Thankyou