Let me try and answer the questions. Most of what you have asked is already covered in the thread.

- Nisith Arora had already clarified in the earlier call that it will preferably be two or three acquisitions as opposed to one to spread the risks. He clarified on the call yesterday that talks are going on and some of them have fallen through at the valuation stage. To surmise that the money was raised without any acquisition target in mind is a stretch. Price negotiations are the trickiest part of any acquisition and quite a few deals fall through at this stage.

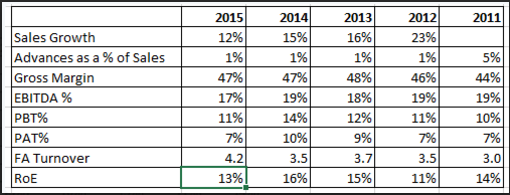

Another interesting point that he raised in the call yesterday was that the sellers are seeking out MPS to sell their companies. Sounds interesting but will have to wait for some meaningful merger to happen before we can take this at face value. - As investors in MPS, we should be clear that the organic growth will at best be between 10-15%. I would personally pencil in 10% for my calculations. Their entire sales strategy is based on farming existing clients as opposed to having more feet on the street and knocking on doors of new clients i.e hunting. This is a strategy that they have consciously adopted to keep the sales cost in check. This is why it is important that they acquire companies which come with a steady revenue source as opposed to say a TSI evolve which had the right people and domain expertise but need to be redeployed on new projects to gain revenue.

The management wants to be a $80 million company in the next 3-4 years and they are working towards it.

Rahul Arora seemed more confident on this call as compared to the one last quarter. However, the management was not convincing on the questions about revenue growth. Not knowing the sales and profit figures of the three small subsidiaries that you have before you come to an investor call was a miss as far as i am concerned.

The slack that the investor community is cutting the MPS management is decreasing with every passing quarter and i hope that the management is aware of that.

yup. I like these guys.

yup. I like these guys.