They gave a guidance of 30-35 cr PAT for FY25

Either thats a conservative number, or they have reduced their guidance significantly from before.

Any idea what volume they did in this quarter?

They gave a guidance of 30-35 cr PAT for FY25

Either thats a conservative number, or they have reduced their guidance significantly from before.

Any idea what volume they did in this quarter?

In my understanding, PI takes a portfolio approach to managing molecule concentration, with different molecules dominating revenues at various times. While competition for pyroxasulfone is imminent, PI has successfully navigated similar challenges in the past. Looking beyond pyro and agrochemicals, PI is now expanding into electronic chemicals and pharmaceuticals, which offer significantly larger addressable markets. I am more excited for PI’s journey now as they replicate their successful strategy in industries with far greater prospects than agrochemicals.

I am not good at understanding these macro shifts, I am more detail oriented and am generally looking for bets where I have better medium term visibility.

I bought Eureka because they are leaders in water purifier market which offers very higher gross margins. For e.g., most consumer durable cos make 30-35% GMs whereas water purifier cos make 50-60% GMs. This implies a possibility of higher operating and PAT margins at optimum utilization. Also, Eureka has been reporting double digit volume growth in last few quarters, when most consumer durable cos are struggling to grow. I feel new management is doing a decent job and there is a lot of value that they can create. Some data excerpts below on Kent’s financials (Eureka’s main peer) to show that potential PAT margins can exceed 15% in good times (super rare in consumer durable space).

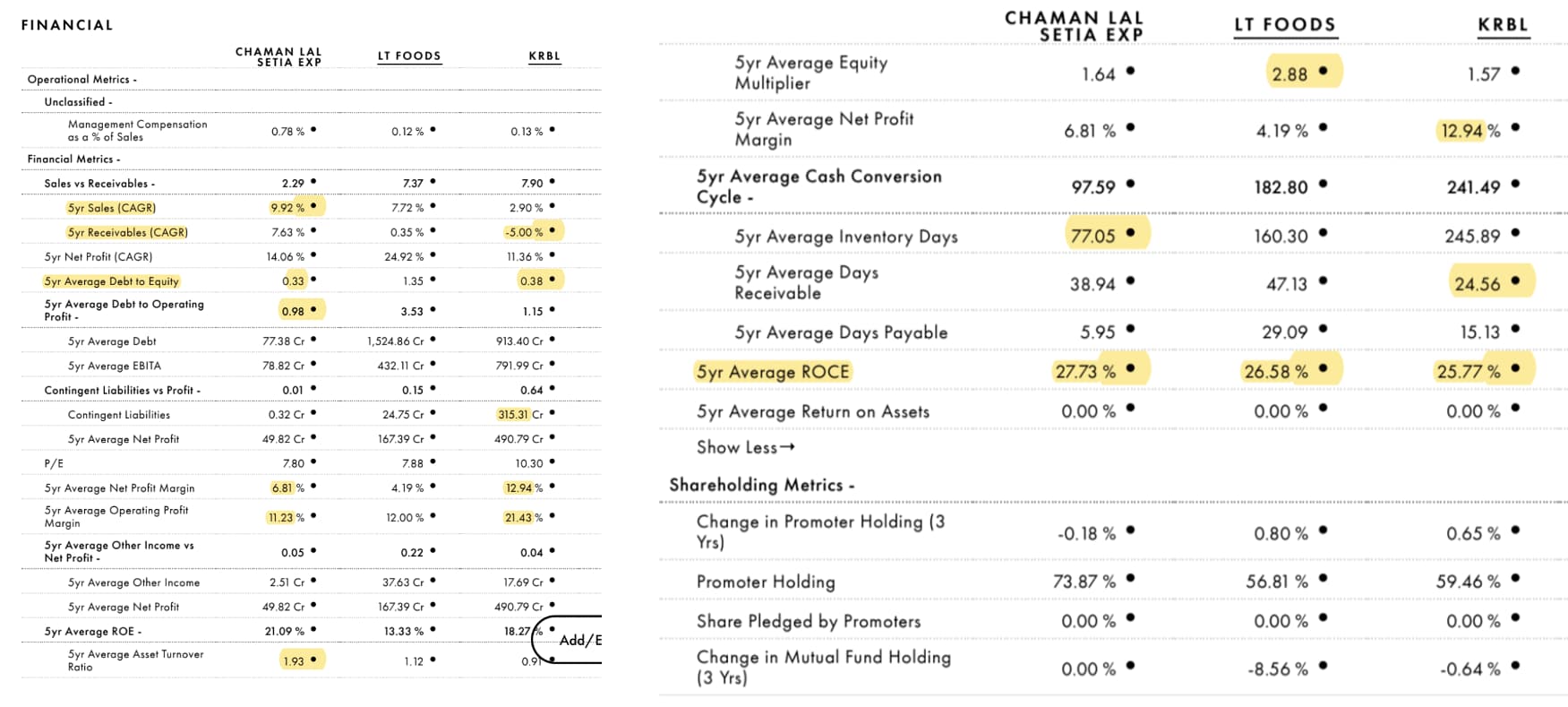

Yes, I still hold it and am excited by how management has opened up to investors and improved capital allocation (increased dividend payout to 10-15% + buyback). I feel with scale, more investors will see how well Chamanlal is managed. They make the highest ROICs, despite operating at lower margins than KRBL/LT foods. Managing inventories is the key in this business and they have done that very well.

Unfortunately, I have not been able to create much cash as I have found opportunities to deploy capital regularly. I have been selling a number of stocks which have done well (e.g. Godfrey, Nesco, HDFC AMC, Kaveri, Time techno, Ajanta, Amara, etc.) and reinvested in some new bets (e.g. Ambika cotton, Venky’s, AGI Infra, Gokul agro, Bharat rasayan, etc.). As a result, I have been unable to generate cash. I am also worried that in the next downturn, portfolio might see sharp drawdowns given how rewarding this upcycle has been. Lets see what future holds.

I cannot guarantee when I will be able to write the theses for some new bets, but I try and contribute to the respective thread (wherever possible).

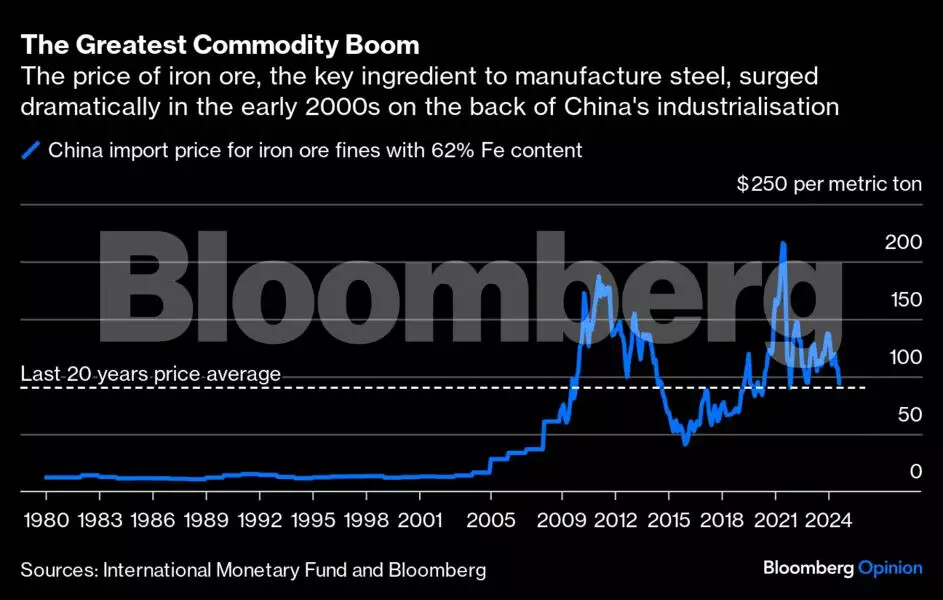

I think below statement from the article will required to be closely watched;

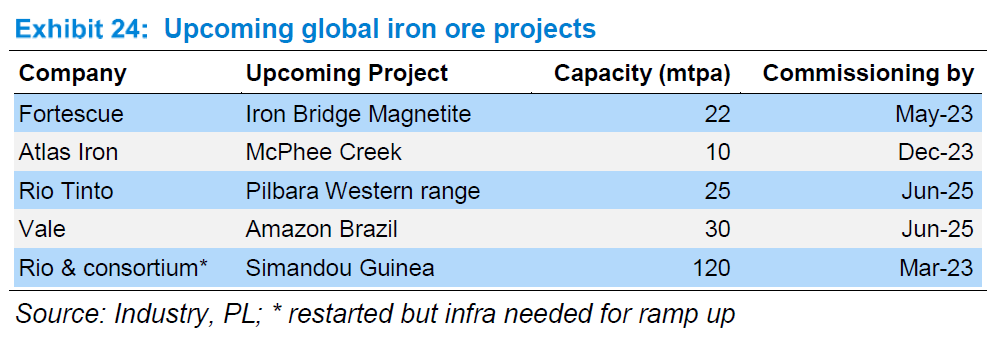

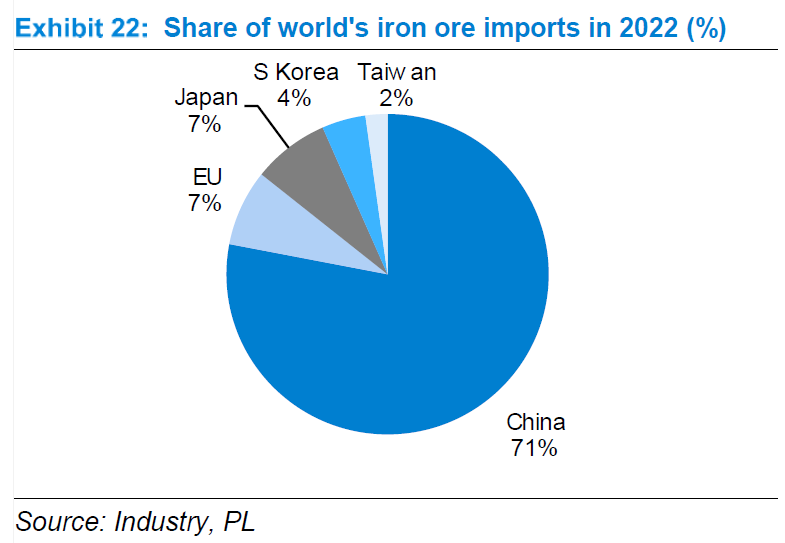

The slowdown in China comes, crucially, as a new generation of large, low-cost mines in Australia and Africa start production. That mix is the problem because it means the iron ore market, already oversupplied in the first half of this year, would remain in surplus in 2025, 2026, 2027 and probably 2028, too. Macquarie Bank Ltd., an Australian lender, says that the current surplus is “one of the worst” ever.

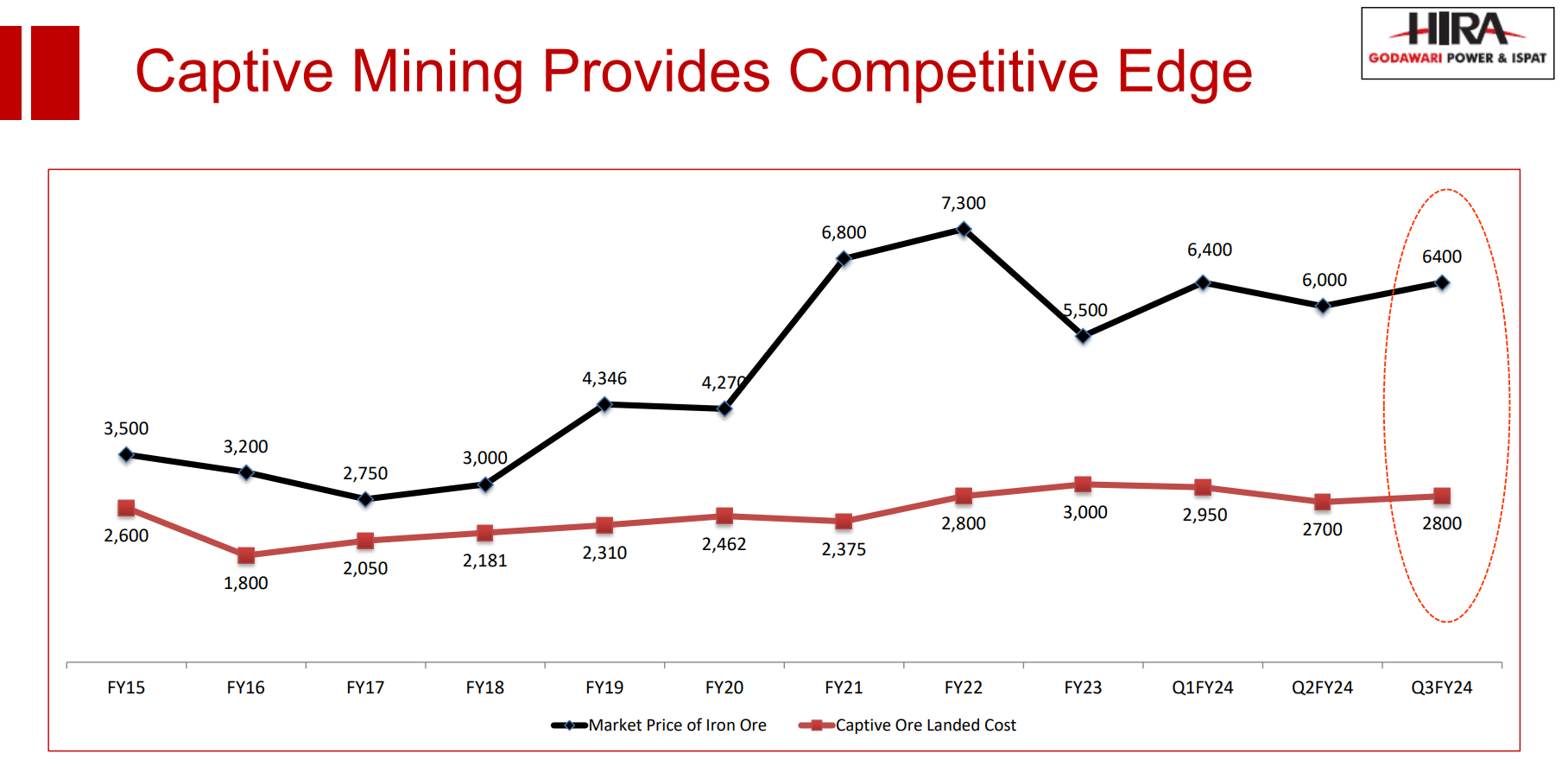

For GPIL the landed cost of captive iron ore is around 2800rs ($40).

Currently the iron ore price is around $98.

Iron Ore – Price – Chart – Historical Data – News (tradingeconomics.com)

The article also pointed out that;

Over the medium-term, iron ore prices must drop to rebalance the market, pushing out high-cost miners. How low? It would depend a lot on whether the new mines come on stream on time, and whether the Chinese real estate sector recovers a bit.

In 2015-16, the prices dropped to $50 due to oversupply. Rio Tinto Plc., the world’s largest iron ore miner, digs the mineral out of the Pilbara region of Western Australia at a cost of about $21 a ton.

I think there is medium term risk to iron ore prices as pointed out in the article. There is higher probability of capital cycle playing out in this sector going forward.

However, GPIL is one of the low-cost producer having high grade Fe iron ore mines.

Disc: Invested & Biased. Not a mining expert or related to mining industry. Views are personal.

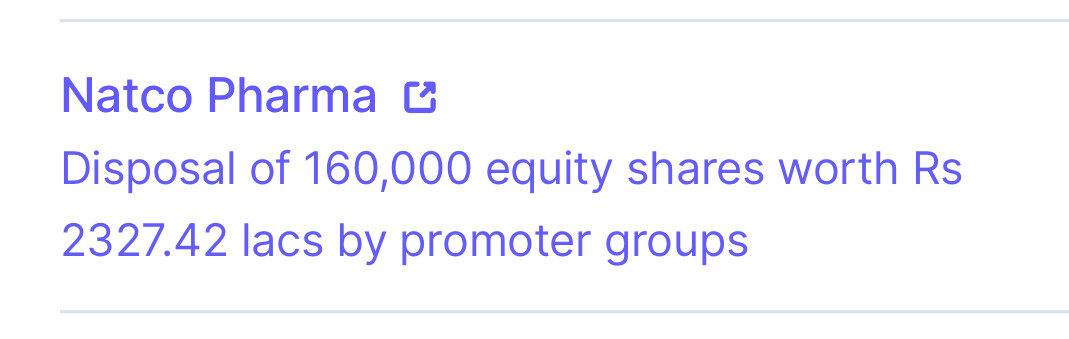

Nothing to worry, its not even 0.1% of total market cap.

Vikas… this info is very much available in public domain. Sajal Kapoor like collaboration and hence his views are biased.

I have a different view, Natco did CDMO in 1990s early 2000 as job work and already moved ahead in value chain while other players (not so competent) are doing that now. It is not easy to go against patent and win the litigation, need lot of guts to challenge Innovators. As per Sajal Kapoor, Natco is an extremistan, but I see Natco as a DoD business instead of QoQ or YoY. Look at last 10 years data on valuation parameters like sales CAGR, profit CAGR, ROCE and ROE to understand what I mean to say. The tons of cash Natco is generating and continue to generate through Revlimid till early 2026 will help the company to grow inorganically. Moreover, in the recent con call, Rajeev mentioned that Semaglutide launch is expected in 2026 in India, this will keep the growth momentum going as it will contribute significantly being a wonder drug.

Mutual funds were thinking that Revlimid is a one off, hence were valuing company as base business + Revlimid, hence were reducing their holding in Natco. As a result, MFs hold only 2.7 percent stake now, which is at 15 years low (never went below 5 percent since 2014). Now, looking at growth, they will end up buying it again at higher price.

I may also be biased as Natco is my top holding, but will continue to hold for another 7 years. If Divis can be a 1.25L crore market cap company and Laurus can be a 40k crore market cap company, Natco can also be a 2.5L crore market cap company, just new couple of more Revlimid like opportunities.

Hii,

Is the company only moving after all time high breakout or there is something I am missing?

Regards,

Mohit Tayal.

Again they are raising funds and this big names will come.

But what they will do with this much money?

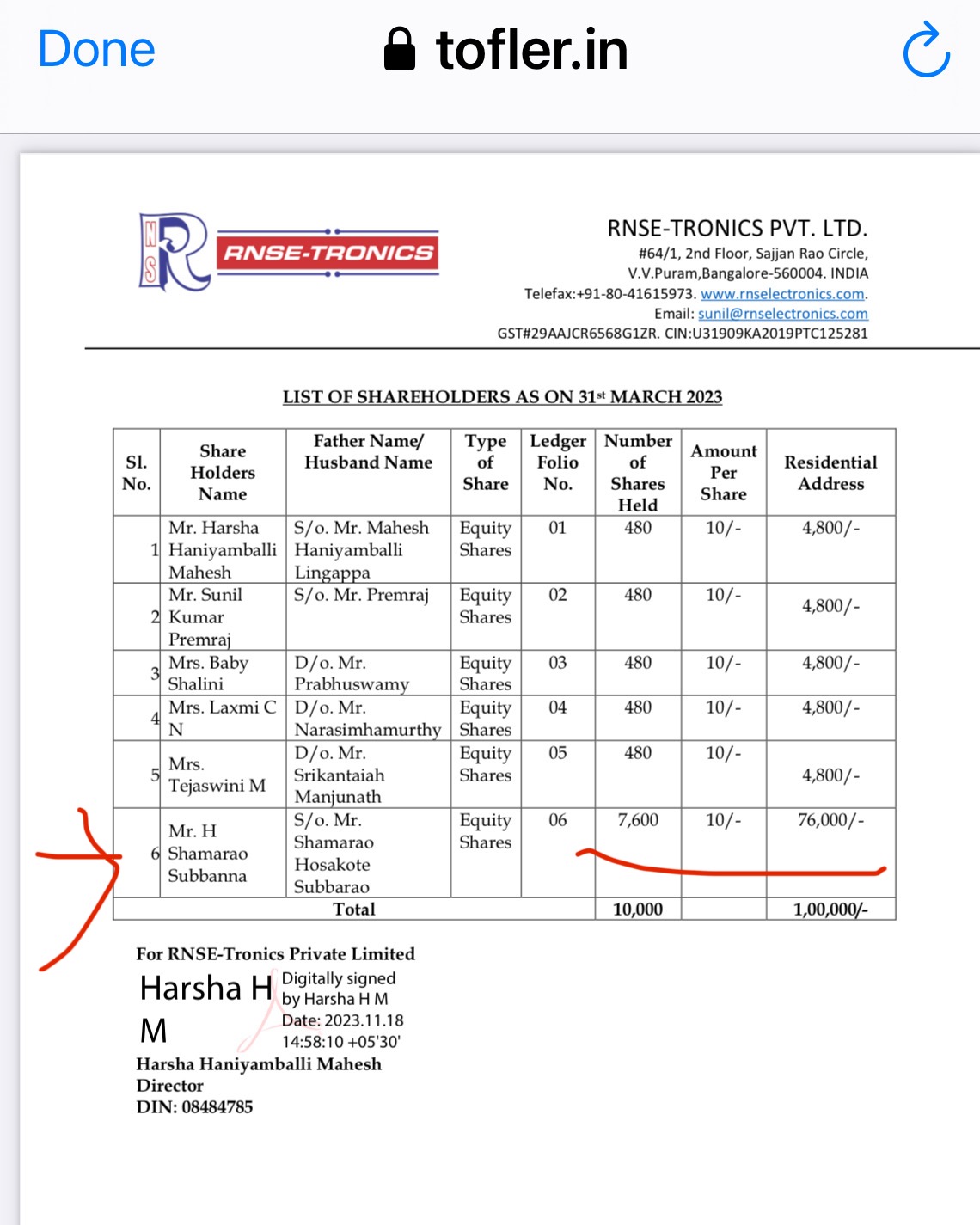

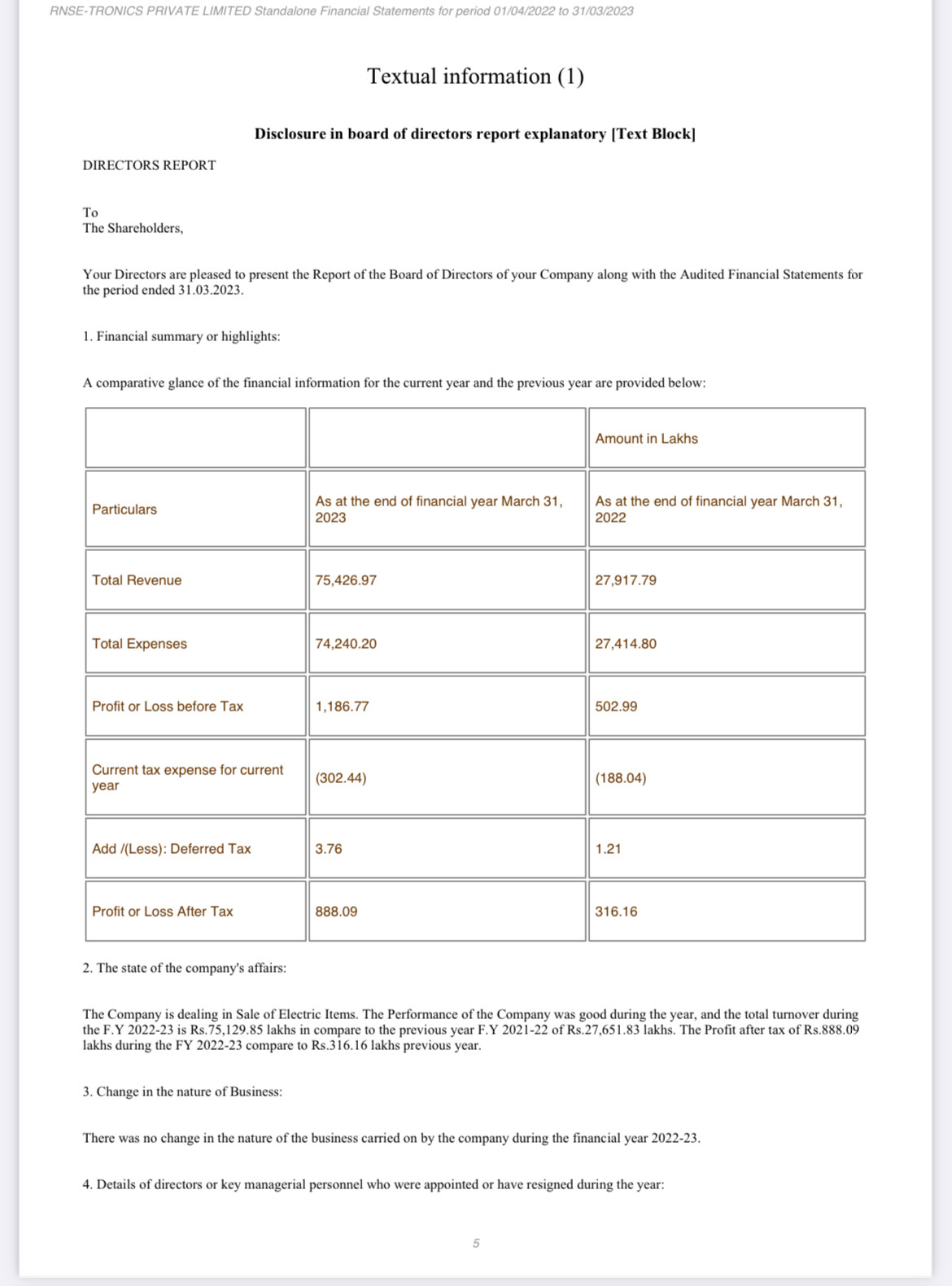

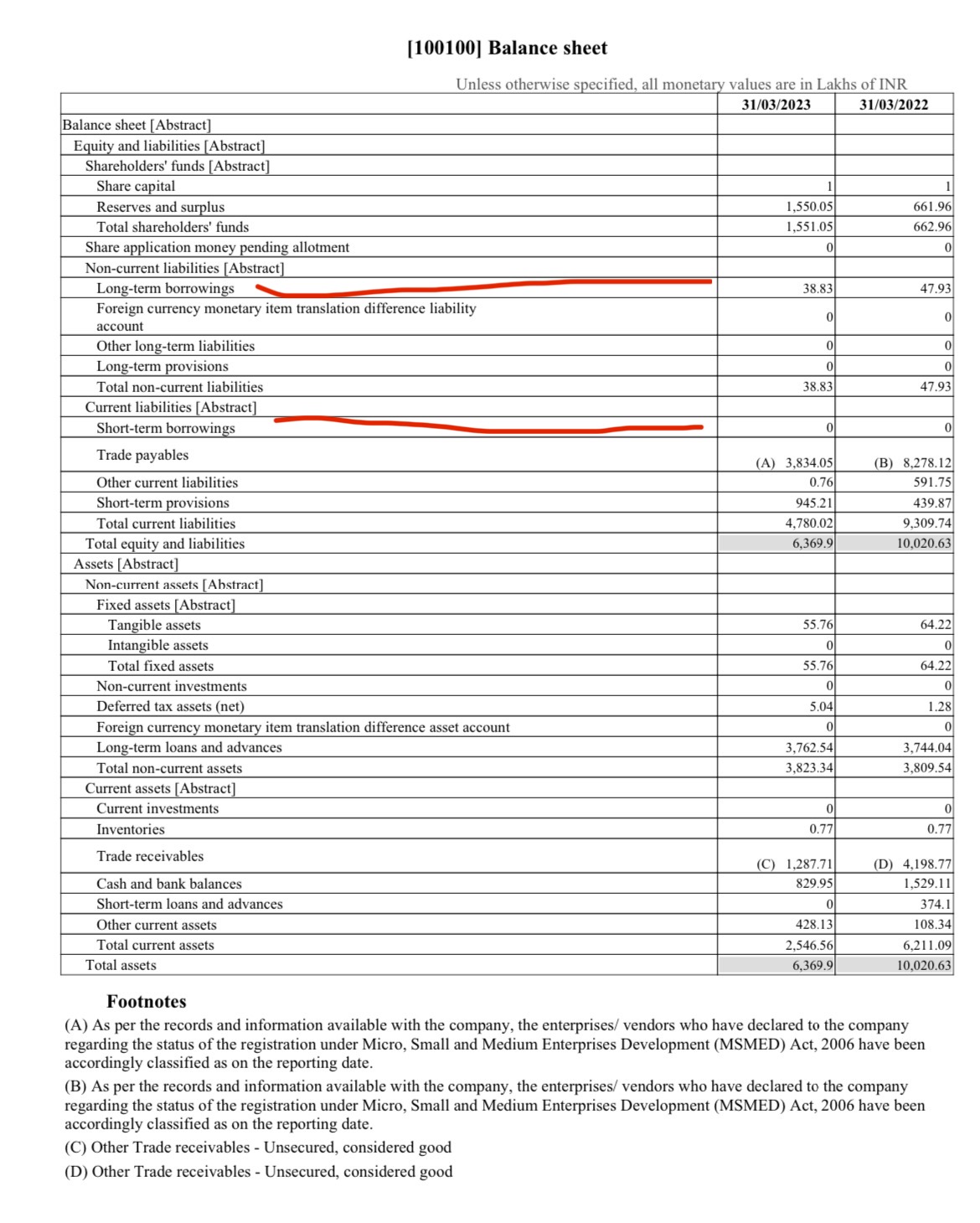

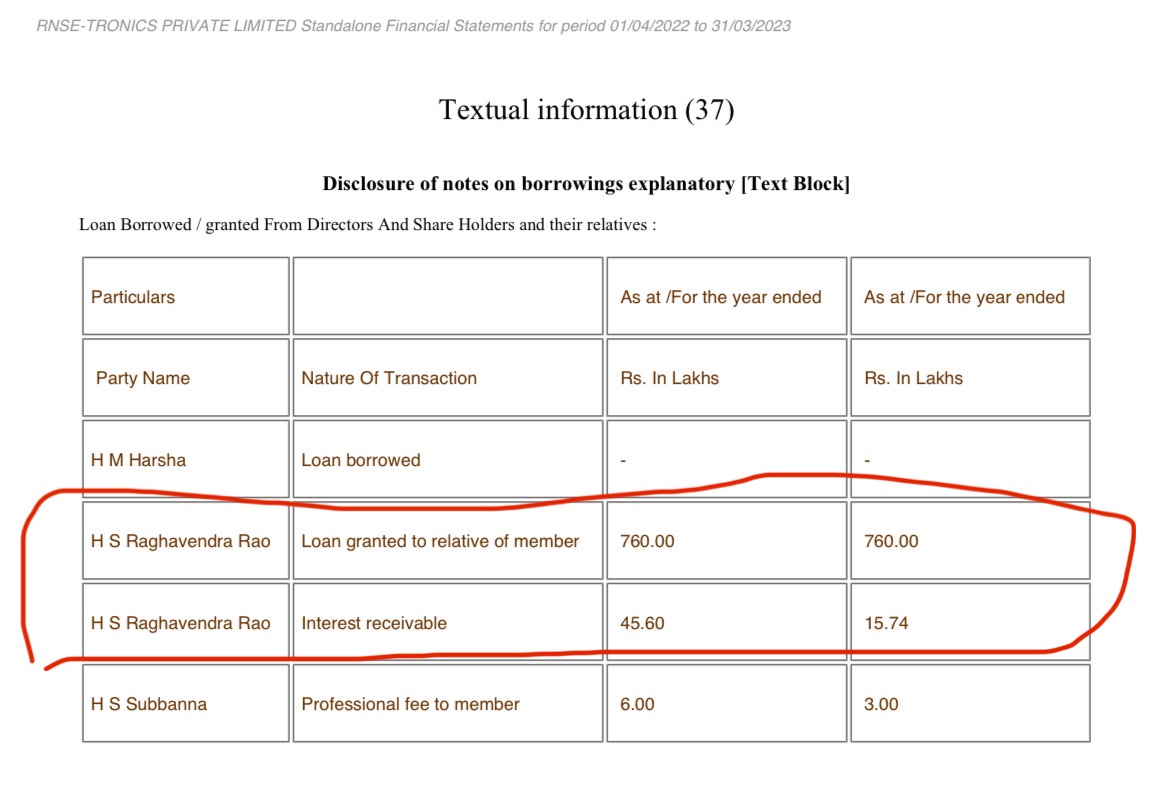

So I downloaded the financials of RNSE-Tronics Pvt Ltd from MCA via Tofler. This is the same promoter owned company which supplied components to DCX. Here are my findings.

76% of the shares of this company are owned by the MD.

Margins are not that great. It made a profit of Rs 8.8 Crores on a revenue of Rs 754 crores.

However it does not have any borrowings, meaning payments are made swiftly by DCX.

It has a given a loan of Rs 7.6 crores to the MD pf DCX.

Apart from the loan of 7.6 Cr I do not see any red flag. I fail to understand why the majority of components are sourced from this company.

FY21 and FY22 had Covid bump up. So limited growth in FY23 is understandable. What about FY24?

Promoters keep spinning stories according to their convenience