The online exchange highlights a recurring theme in Indian investing: the tension between traditional...

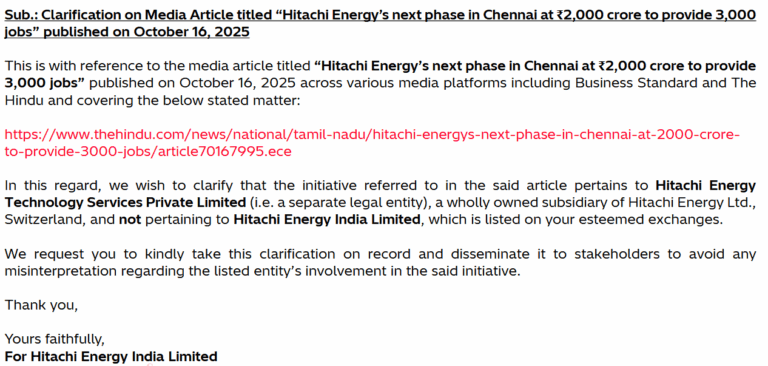

Market analysts believe that this distinction removes uncertainty about HEIL’s financial exposure

CIFC is gradually evolving into a more robust and resilient NBFC—one that is less...

Crizac’s lean, three-tiered operating model supports robust profitability, with EBITDA margins of ~25% in...

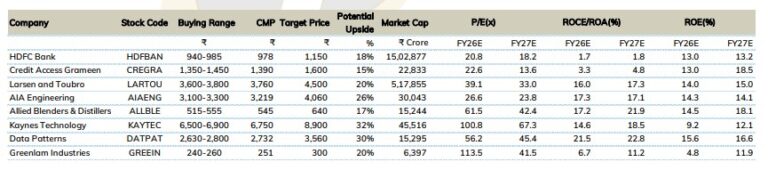

The current stock price has factored in most of the negatives.

Noticees collectively generated an amount of alleged ill-gotten gains totaling over ₹172 crore from...

Leela is also working towards obtaining regulatory approvals to demerge the office business from...

Simplifying Business Spends Zaggle is a home-grown SaaS-fintech platform that helps businesses digitise spending...

We expect double digit earnings growth to resume from FY27E onwards, which should ensure...

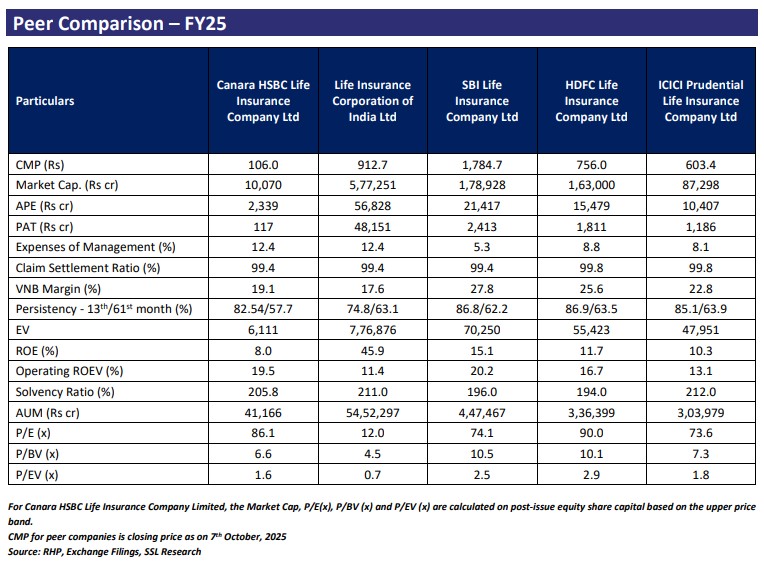

CHLICL remains focused on building sustainable long-term value through consistent growth, strong underwriting standards,...