JTL Industries Ltd (JTL), a prominent player in the structural steel tubes and pipes...

TRIL beat our Q2FY25E by a mile powered by strong execution (+80% YoY), lifting...

Skipper is ready to harness several tailwinds: i) power T&D capex of INR9.2tn over...

Jubilant Pharmova (JPL) is undergoing a turnaround and adding new growth drivers, which provides...

33%, and 41% revenue, EBITDA, and PAT CAGR, respectively, over FY24-27. This growth will...

Aeroflex Industries Limited (AERIND), incorporated in 1993, is engaged in the business of manufacturing...

V2 Retail (VREL) posted a 64% YoY growth in revenue to INR380cr on the...

The Axis Top Picks Basket delivered an excellent return of 10.4% in the last...

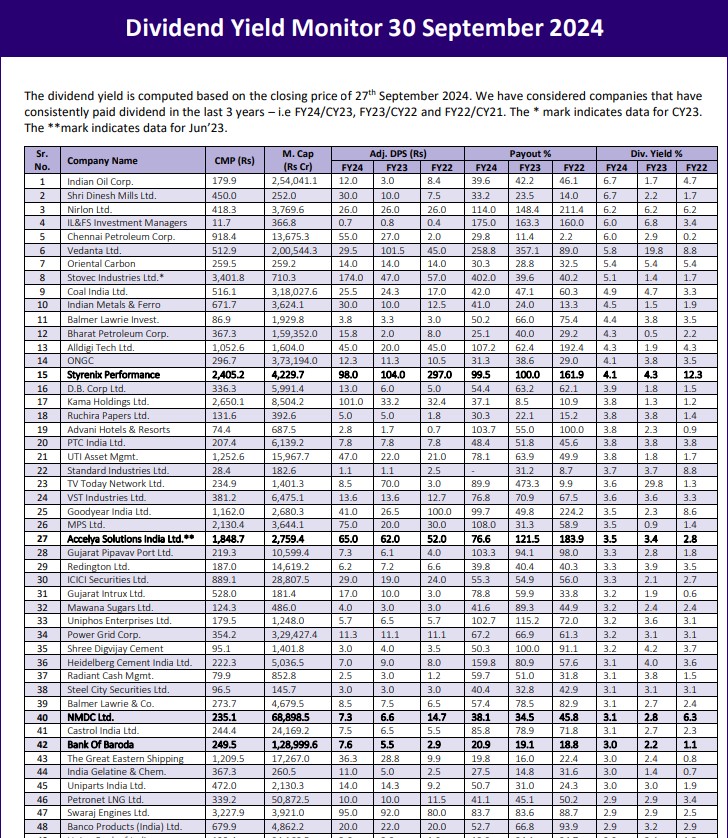

The dividend yield is computed based on the closing price of 27th September 2024....

We hosted JB’s CEO, Nikhil Chopra, for a roadshow in the UK. The company...