DLF has a strong land bank (development potential of 188msf (70%+ in Gurgaon) of...

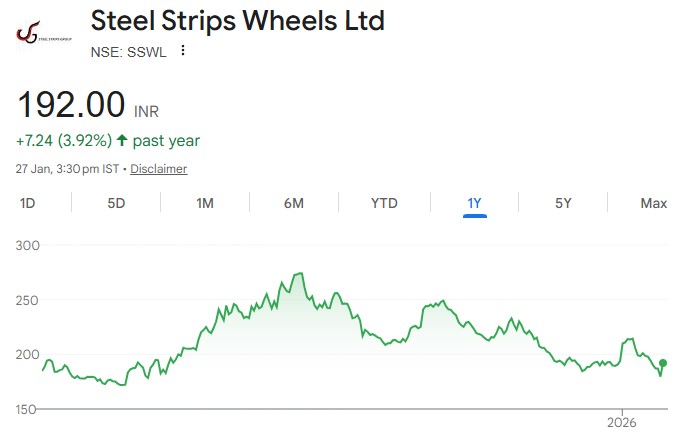

We expect EBITDA per wheel to rise to Rs 264 in FY27E and Rs...

RKL’s revenues and PAT are expected to grow at CAGR of 19% and 38%...

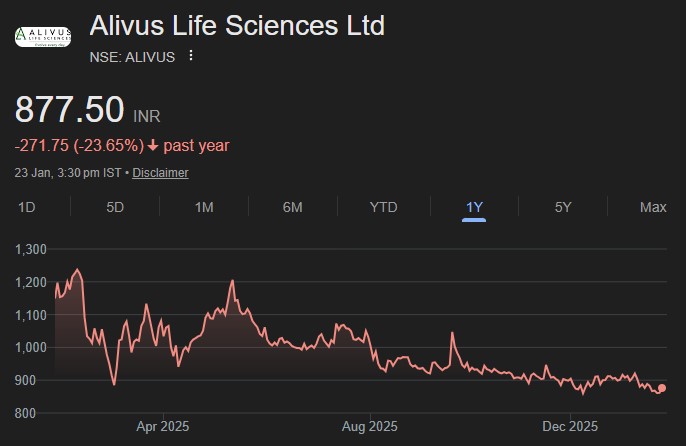

TATVA expects SDA revenue growth to sustain, with new customers’ offtake in CY26 and...

The company is also into CDMO services (~7% of FY25 revenues) catering to a...

The company is on track to expand its production capacity from 5 Mn ton...

ITC Hotels registered resilient performance in Q3FY26 aided by strong wedding, MICE and corporate...

ITCH currently has a portfolio of 213 hotels - 152 operational and 61 in...

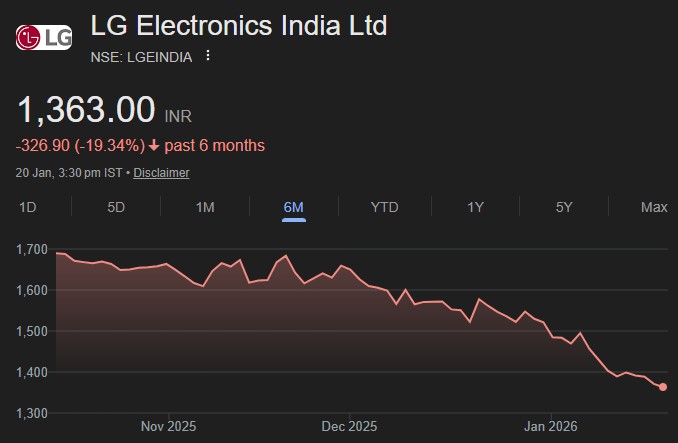

LGEIL benefits from its parentco’s massive scale, focus on technology and R&D (annual R&D...

Of the 40GW of projects with pending PPAs, industry channel checks suggest ~17GW...