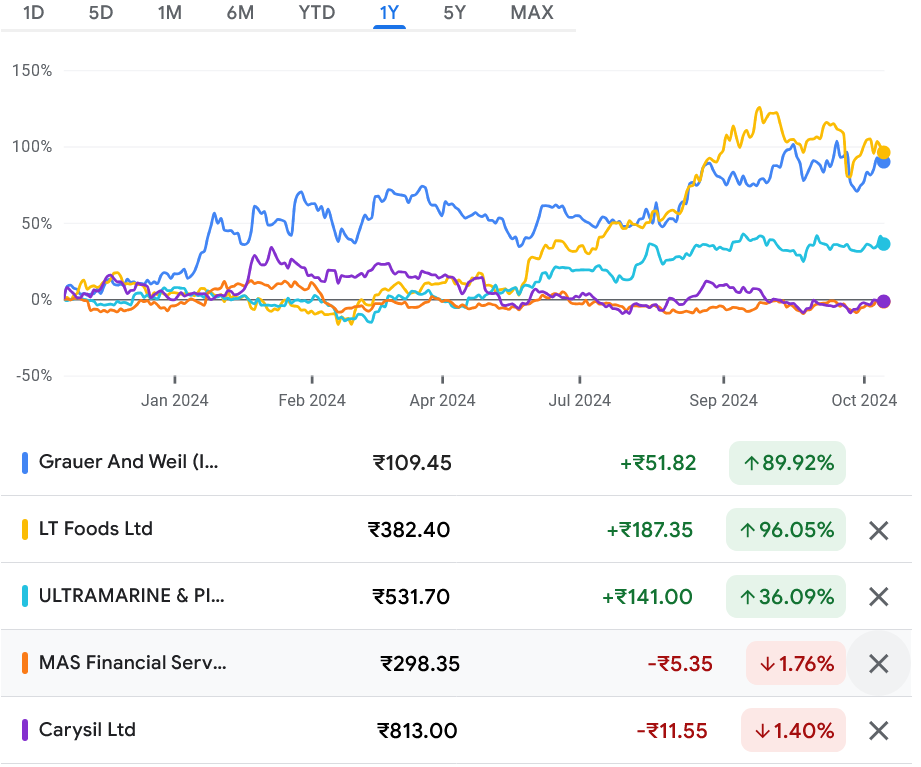

Additions to the Rising Giants PMS portfolio (as of October 31, 2024)

1. Grauer & Weil (India) Ltd.

Grauer and Weil (G&W) enjoys a strong moat in its core Electroplating Chemicals business around: the recipe of the chemicals (IP), customising the product to the requirements of the customer and providing customer service through Pan-India technical centres. Consequently, there are strong entry barriers/barriers to scale in the industry with G&W and Artek being the only 2 large Indian companies alongside a few MNC players. Moreover, G&W has created strong competitive edge through backward integration into engineering electroplating equipments as well to the in-house manufacturing of certain intermediates.

G&W has also developed a strong moat in the niche paints applications through R&D and is the No.1 player in the Oil & Gas Pipes segment and No.2 in the water pipes segment. In the Malls business, company has a unique locational advantage in the western suburbs of Kandivali (east) which lacks meaningful competition (though we could see some upcoming competition from a new Oberoi Mall).

While the Electroplating chemicals business is expected to grow in line with automotive/manufacturing industries, Paints business is expected to continue to grow at a faster pace. The Company is setting up a large R&D centre in Vasai which can help G&W to enter into newer segments and gain market share.

2. LT Foods Ltd.

In a seemingly commodity-like business of rice and rice products, LT Foods has been able to build a formidable franchise underpinned by:

A robust procurement supply chain architecture (digital investments, agri-extension team and long-standing commission agents) that has brought down the procurement costs and inventory days in a business that typically requires longer storage of inventory (due to ageing requirement of basmati rice).

Adoption of automation and industry first methods (Silo storages) that have enabled quality as well as yield improvement in the recent years.

Well-thought-out capital allocation decisions – foraying into USA, Europe in contrast with peers’ focus on much larger but challenging Middle East market. The promoters have displayed flexibility in ‘build vs buy’ to create a strong market presence in key export markets and bring diversity in the business model (such as foray into jasmine rice).

All of the above has culminated into a strong brand presence and market share across geographies with Industry leading revenue growth, margin and return ratios in the last 5 years.

Marcellus sees further growth drivers for the business from:

Rising consumption of Basmati given its health benefits (low glycaemic index) and premium positioning.

Continual market share gains, especially in India (as channels formalise; shift from loose to packaged rice) and Europe (new greenfield in UK).

Opportunity in the Middle East market through SALIC as a strategic investor.

Opportunity in health and convenience segment.

3. Ultramarine & Pigments Ltd.

Ultramarine & Pigments’ core business consists of surfactants (~35% of EBITDA) and inorganic ultramarine blue pigments (~50% of EBITDA). In the surfactants division, Ultramarine is a relatively smaller player compared to peers like Godrej Industries and Galaxy Surfactants (nearly 9x the size of Ultramarine). However, Ultramarine is the largest surfactants player based in South India giving it strategic locational edge particularly amongst local FMCG players. Similarly, in the pigments segment, it is one of the top 5 inorganic Ultramarine Blue pigment manufacturers catering to industries such as plastic, paints etc. While there are a number of unorganised players in colour pigments, players like Ultramarine carry strong technical advantage in the form of high yield ratio, consistency in quality and solutions approach to customers.

4. MAS Financial Services Ltd.

MAS Financial is a Gujarat headquartered NBFC which lends to the SME and MSME segments via two models – (i) direct lending to MSMEs (with an average ticket size of Rs. 35,000) and to SMEs with an average ticket size of Rs. 37 lacs) and (ii) lending to NBFCs which further on lend to the SME & MSME segment, this constitutes 55-60% of the loan book. Its key strength lies in its unique business model of lending to NBFCs on the asset side and building the liability side by way of assignments, thereby enabling it to make large NIMs with NPAs of under 2%. MAS has a track record of consistent and profitable growth over the previous two decades, its loan book and PAT have grown at a CAGR of 16% over FY18-24. It has been able to maintain average NNPAs over FY18-24 at under 1.5% with an average RoE of 16.3% during the period.

5. Carysil Ltd.

Carysil started as a manufacturer of quartz sinks (FY24 – 51% revenue mix) & over time diversified into adjacencies like stainless steel sinks (13%), kitchen appliances/bath products (11%) & solid surface tops (25%). Carysil started with Quartz sink exports to Europe and US. Carysil’s customers are building material companies/retailers like IKEA, Grohe, B&Q, Menards, Lowe’s and Home Depot.

Quartz has been taking share from Stainless Steel sinks due to better aesthetics. We expect Quartz sink market to grow in double digits as it continues to take market share from Steel. Carysil makes quartz sinks through “Schock” technology. Globally there are only 4 companies which have this technology viz. Schock in Germany, Blanco in US, Franke in Switzerland, and Carysil in Asia. Schock technology and know-how serves as a strong moat for the company and acts as an entry barrier. Furthermore, out of the 4 players who have Schock technology, all except Carysil have plants in US or Europe and hence are at a cost disadvantage compared to Carysil. Overtime, the firm has expanded into adjacencies like premium stainless-steel sinks, quartz surface tops, kitchen appliances (hobs, wine chillers), sanitaryware & bath fittings.

Carysil has history of doing M&A to enter new geographies or new categories in UK & USA at attractive valuations. Revenue & PAT has grown at 22% CAGR and 27% CAGR over FY19-24.

On the other hand, we have exited from Info Edge (India) Ltd- InfoEdge share price has run-up by 82% in the twelve months ending 31st October 2024) – which meant that IRR expected on the stock has come down significantly. As a result, it was decided to exit from the stock.

Source: Respective company’s annual filings

Additions to the Little Champs PMS portfolio (as of October 31, 2024)

1. Grauer & Weil (India) Ltd.

Please refer the rationale provided above under the RGP additions

2. LT Foods Ltd.

Please refer the rationale provided above under the RGP additions

3. Narayana Hrudayalaya Ltd.

NH runs a chain of hospitals across India and in Cayman Islands. The corporate hospital industry in India is undergoing structural tailwinds due to: a) increase in health insurance penetration; and b) increase in awareness and early detection of diseases related to oncology and cardiology. Amidst these tailwinds, NH has built a hospital network in Bangalore, Kolkata, Delhi and few other parts of the country. NH has also built a hospital in Cayman Islands, which has scaled up operations and profitability significantly over the last 5 years.

Competitive advantages of NH centres around the following:

Multiple profit engines firing successfully (unlike other hospitals who have only single engines profitably firing) – Bangalore, Kolkata and Cayman with healthy ROCEs in each of these three geographies. Moreover, management has disclosed in its annual reports and quarterly conference calls that bulk of its future expected bedcount growth is likely to come these three geographies.

Relatively asset light + process efficiency orientation (medical device automation as well as opex automation through in-house software development e.g. Athma, Namah and Disha are some of the inhouse developed softwares). This helps maintain low ARPOBs compared to competition with high ROCEs, without having to pay ‘star-doctors’ significant remuneration packages.

Moats in Cayman:

Low doctor costs because doctors are supplied from India – rather than imported from the US;

Tie-ups with reputed institutions in medical sciences in the US; and

Covid forced Cayman’s local population to experience NH hospital for treatment.

4. Escorts Kubota Ltd.Inspite of the erstwhile promoters losing focus on the tractors business and being at the brink of bankruptcy, Escorts has still maintained its market share, thanks to its strong brand image and turnaround architected by Nikhil Nanda and team. With Kubota now controlling majority of the stake, we believe Escorts is at a cusp of gaining market share in the tractor industry because of the following reasons:

From FY20 to FY23, Escorts underwent a massive attrition (due to variety of reasons) and now the leadership team has stabilised.

After improving product quality, Kubota’s next target is to launch relevant products for the Indian market which helps to gain market share

Escorts is forming its own captive financing arm which is expected to be a market share booster.

Apart from the domestic market, Kubota intends to make India an export hub and export tractors to Africa, US and Europe markets.

Driven by market share gains and consequent operating leverage driven margin improvement. we expect the company to clock healthy earning growth over the next 5 years.