Skip to content

February 11, 2026

Rakesh Jhunjhunwala

Fan Site: Inspired, Not Endorsed, By Rakesh Jhunjhunwala

Primary Menu

Articles

Portfolios

Rakesh Jhunjhunwala Latest Portfolio

Dolly Khanna Latest Portfolio, Holdings, Wiki, News | December 2023

Research Reports

Stocks Talk

Top Stock Picks 2024 | Live Portfolio Tracker

Light/Dark Button

Search for:

Subscribe

Home

Stocks News

Stocks News

You may have missed

investments

Man Industries has stellar growth potential. Buy for target price of ₹694 (80.7% upside): SBI Securities

February 10, 2026

0

investments

Crompton Greaves Consumer Electricals 3QFY26 earnings were above estimates. Buy for target price of ₹350 (43% upside): Motilal Oswal

February 9, 2026

0

investments

Jubilant Pharmova has an aspirational target for FY30 of doubling of overall revenues. Buy for target price of ₹1310 (41% upside): ICICI Direct

February 8, 2026

0

investments

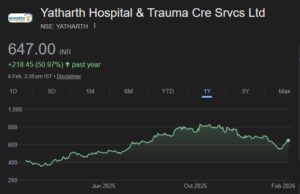

Yatharth Hospital is well placed to deliver strong, compounding growth. Buy for target price of ₹855 (33% upside): SMIFS

February 7, 2026

0

investments

Interarch Building Solutions is preponing expansions anticipating high demand. Buy for target price of ₹2850 (36% upside): ICICI Direct

February 6, 2026

0

investments

Pearl Global Industries has transformed into a professionally managed entity. Buy for target price of ₹2255 (41% upside): ICICI Direct

February 5, 2026

0