What is Contrarian Investing?

To understand the theory behind ‘Contrarian Investing‘, we have to turn to a research report issued by Gautam Duggad and Bharat Arora of Motilal Oswal.

The duo has explained the entire concept in crystal clear terms:

It pays to be different

Identifying contrarian investment strategies that work

Contrarian investing is a time-tested investment tool, which involves buying/selling stocks that goes against the prevailing sentiment of crowd or the market. It is among the first lessons taught to budding investors and literature on the subject dates back decades.

Contrarian Investment Strategies: The Psychological Edge by David Dreman, Extraordinary Popular Delusions and the Madness of Crowd by Charles Mackay, and The Triumph of Contrarian Investing by Ned Devis are only some of the literary works that help understand this subject.

The objective of this report is to develop an application toolkit for India. We have covered two major themes based on consensus ratings (stock popularity) and valuation multiples, and have demonstrated the success of contrarian investing in India.

What is stock popularity?

Bloomberg collects analyst recommendations on each stock and assigns a consensus rating based on these recommendations. It assigns 5 points for every buy recommendation, 3 points for every hold recommendation and 1 point for every sell recommendation. A consensus rating is arrived at by taking the average of these scores.

A stock with a consensus rating of 5 would have all buy recommendations.

A stock with a consensus rating of 3 would have an equal number of sell and buy recommendations, apart from hold/neutral recommendations.

A stock with a rating change from <3 to >3 has a recommendation change from a net sell to a net buy.

A stock with a consensus rating of 1 would have all sell recommendations.

Consensus sell rating (%) of a stock = number of sell recommendations / total recommendations.

Consensus buy rating (%) of a stock = number of buy recommendations / total recommendations.

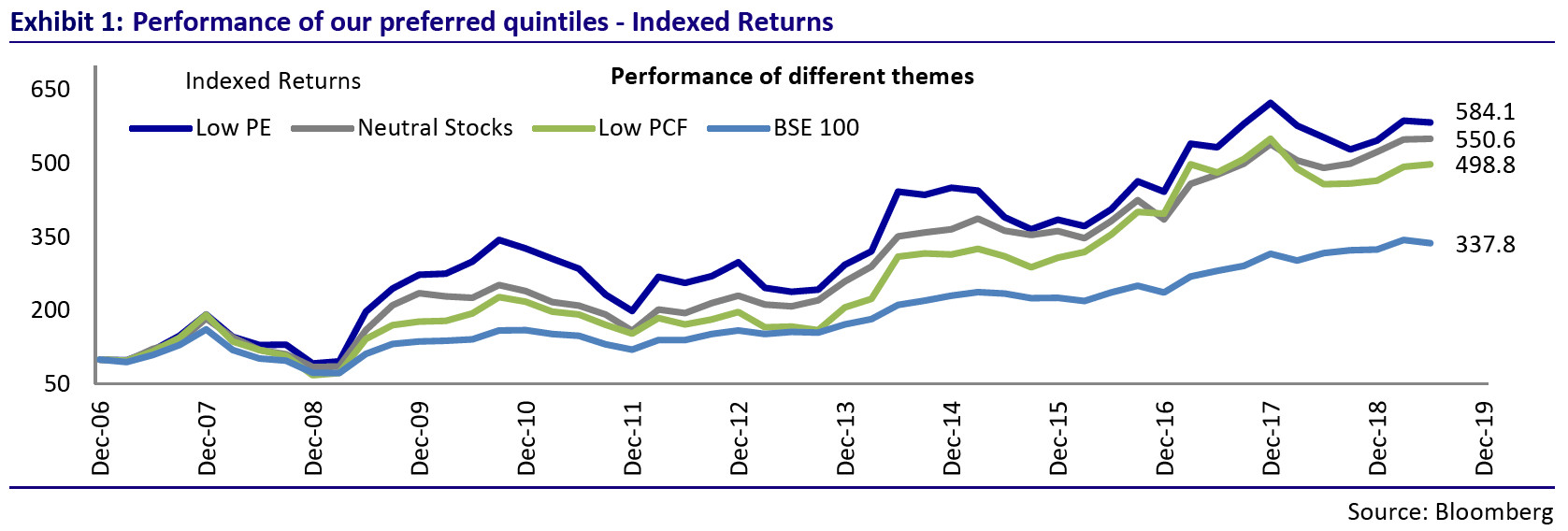

Contrarian investing can generate disproportionate return

Our analysis based on empirical evidence over the last decade suggests that investing in out-of-favor stocks can generate disproportionate returns as compared to the market.

Our findings suggest that neutral to moderately popular stocks deliver significant outperformance, even bettering the most popular stocks. Our findings are in harmony with the findings of “Analyzing the analysts: When do recommendations add value?” by Narasimhan Jegadeesh, Joonghyuk Kim, Susan D Krische and Charles Lee, Journal of Finance 2004, that in the absence of favorable characteristics (value stocks and positive momentum stocks), the most popular stocks are associated with the worst returns.

Our findings prove that out-of-favor low P/E stocks deliver disproportionate returns, significantly beating the benchmark. In contrast, the performance of high P/E stocks is dismal.

Our findings are in harmony with the findings of “Cross-Section of Expected Stock Returns”, by Fama-French, Journal of Finance, 1992. Great recommendation: Buy stocks with a consensus change from net sell to net buy

Our findings suggest that a simple strategy of investing in stocks for which analyst consensus has changed from “net sell to net buy” with a holding period of one year has delivered 24.1% annual returns over the last 10 years.

In the study, “Analyzing the analysts: When do recommendations add value?” the authors also find that the quarterly "change" in consensus recommendations is a robust return predictor that appears to contain information not contained in a large range of other predictive variables.

Performance of Contrarian BUY and Contrarian SELL calls indicated in last quarterly update

The proof of the pudding is in the eating.

In the latest report, Motilal Oswal has produced data which shows that the theory of contrarian investing does and work and results in handsome gains for investors.

In fact, the simple strategy of investing in stocks for which analyst consensus has changed from net sell to net buy with a holding period of one year has delivered 21.1% annual returns over the last 10 years.

Key takeaways from 1QFY20 quintiles

Our analysis suggests that, over a longer term, neutral-to-moderately popular stocks deliver a significant outperformance, even bettering the performance of the most popular stocks. In 1QFY20, the most popular stocks performed the best, beating the benchmark, whereas the neutral to moderately popular stocks delivered the third best return.

Our findings prove that, over the long term, out-of-favor low P/E stocks deliver disproportionate returns, significantly beating the benchmark. In 1QFY20, high P/E stocks performed the best, whereas low-P/E stocks came in second.

Similarly, out-of-favor low P/CF stocks deliver disproportionate returns, significantly beating the benchmark. In contrast, the performance of high P/CF stocks is dismal. In 1QFY20, low P/CF stocks delivered the best returns, whereas high P/CF stocks delivered the second best returns.

1QFY20 was characterized by the decent performance of the value quintiles (low P/E, low P/B delivered second best returns, whereas low PCF came in first).

We also note that in some sub-themes, the returns from a quintile deviate from the long-term pattern, as highlighted in our initial detailed note. However, this is in line with the trends observed even in the long-term study – where returns can deviate for a quarter or two, but over the long period, the hypothesis is proven right. For example, in the Popularity theme, instead of Quintile-4, Quintile-1 has delivered the best returns in 1QFY20.

Best delta: Consensus change from Net Sell to Net Buy

Our findings suggest that a simple strategy of investing in stocks for which analyst consensus has changed from ‘Net Sell to Net Buy’ with a holding period of one year has delivered 21.1% annual returns over the last 12 years.

Net Sell to Net Buy stocks for 1QFY20: There were no stocks that satisfy this criterion for this quarter.

Exit from list: United Spirits and ABB have exited our list after completing 12 months. These stocks entered from ‘Net Sell to Net Buy’ in May’18 and delivered (17.2%) and 27.8% returns in a year.

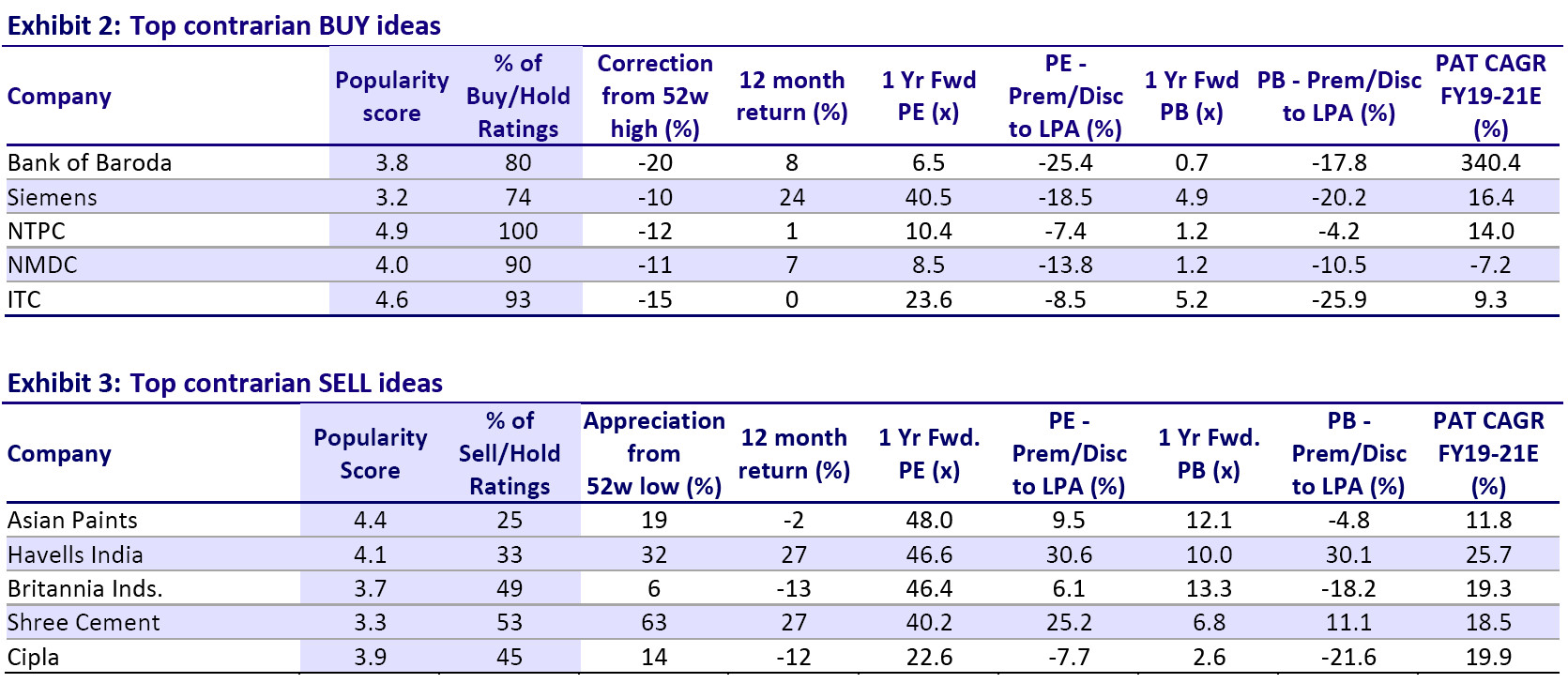

Top Contrarian Stock Picks In 2019

Motilal Oswal’s top contrarian Buy and Sell picks based on the various themes covered in the research report as well as in the past – Popularity, Relative Valuations, Net Sell to Net Buy, Consensus SELLs.

Contrarian BUYs: Bank of Baroda, Siemens, NTPC, NMDC and ITC

Contrarian SELLs: Asian Paints, Havells, Britannia, Shree Cement and Cipla

A normal small investor should buy best quality fundamentally strong blue chip compnies for long term, when ever he has surplus money and should sell when he needs money.

A regular and small investor should never get into Direct Equity. Always go through MFs and that too SIPs. Minimum period of SIP should be atleast 7 years. Should also have diversified portfolio (RE, Gold, Debt, Equity MFs) besides NPS, Term and Health Insurance. Don’t get influenced by reading about multibaggers, warren buffet and equity beating all classes of portfolio etc.

Exactly sir. even the high conviction ideas goes wrong for the high profile and whiz kid investors, and for small investors like us, we can land in huge trouble. better to go with mutual funds.

RJ has given a very good interview yesterday. He is hopeful of a recovery in the economy and still has faith in the Modi govt reforms. He feels that 10750 is the bottom for our market. Shereen Bhan was asking quite good and asking tricky questions to him!However one thing that was quite evident that he is not that bullish on the market as be normally is.