Skip to content

June 10, 2026

Rakesh Jhunjhunwala

Fan Site: Inspired, Not Endorsed, By Rakesh Jhunjhunwala

Primary Menu

Articles

Portfolios

Rakesh Jhunjhunwala Latest Portfolio

Dolly Khanna Latest Portfolio, Holdings, Wiki, News | December 2023

Top Stock Picks 2026 | Live Portfolio Tracker

Light/Dark Button

Search for:

Subscribe

Home

Archives

Archives

You may have missed

investments

GRM Overseas: Madhu Kela & Nikhil Vora’s Bet on the Packaged Food Opportunity Faces Market Pressure

June 9, 2026

0

investments

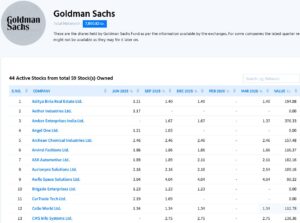

Goldman Sachs Bets on India’s Consumer & Digital Growth Stories Through Groww and Cera Sanitaryware

June 9, 2026

0

investments

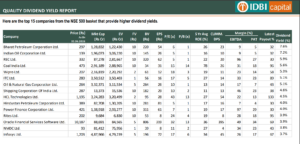

Top 15 companies from the NSE 500 basket that provide higher dividend yields.

June 8, 2026

0

investments

Man Industries: At a Structural Inflection Point with a Massive 53% Projected Upside

June 7, 2026

1

investments

Jeena Sikho: Ayurveda Healthcare Player Poised for Growth, Choice Institutional Equities Sees 69% Upside

June 7, 2026

0

investments

Rising Cricket Phenom: A Look Inside Vaibhav Sooryavanshi’s Net Worth and Assets

June 7, 2026

0