Sunil Singhania's latest investment adds another layer of confidence,

Arjun

The brokerage believes the company is entering its next phase of growth, supported by...

Under Vision 2030, management aims to increase AUM from current ₹14,000 crore to ₹30,000...

Vijay Kedia is known for identifying emerging businesses with scalable business models at an...

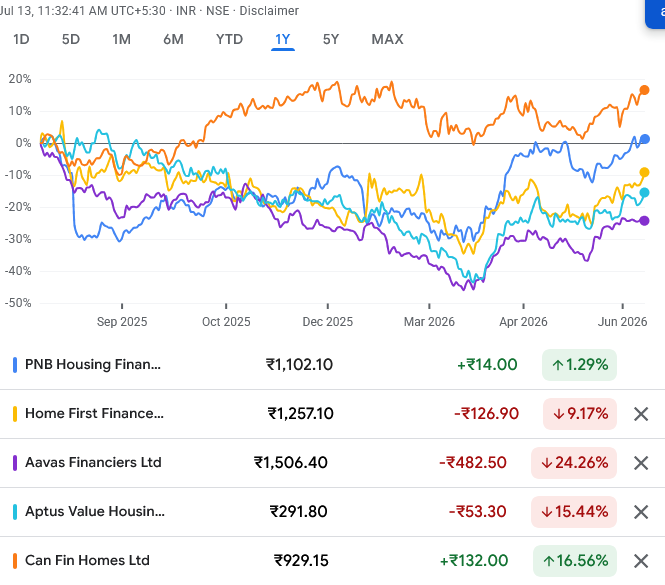

Morgan Stanley Bets on Affordable Housing Finance: 5 Stocks It Says Could Deliver a Multi-Year Rally

Global brokerage Morgan Stanley has turned bullish on India’s affordable housing finance space, identifying...

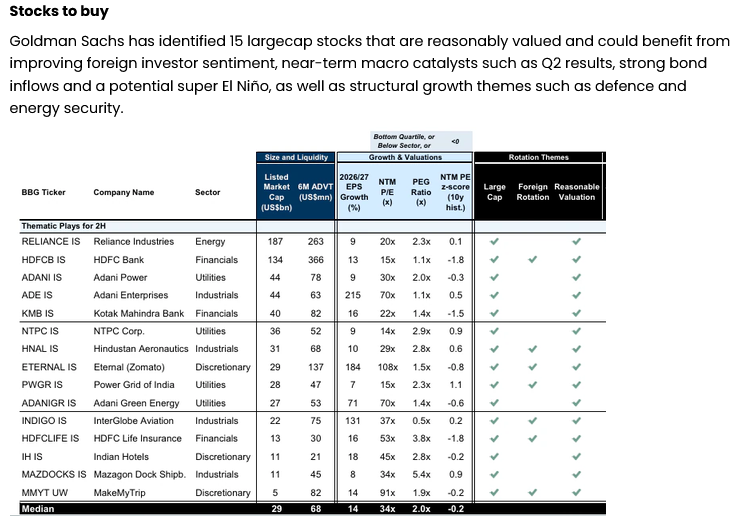

Instead of chasing expensive momentum stocks, Goldman Sachs is recommending investors focus on 15...

Bengaluru anchored the quarter with its strongest-ever sales at INR 20.7bn (56.5% of total),...

Quant Mutual Fund's ₹175 crore investment reinforces institutional confidence in Ethos' long-term growth story.

Nemish Shah Bets ₹275 Crore on Blue Jet Healthcare, Sees Value in Debt-Free Specialty Pharma Company

Blue Jet Healthcare stands out for its strong balance sheet. The company is completely...

Global brokerage Citi has issued a 'Buy' recommendation on Kalyan Jewellers with a target...