Dhabriya Polywood remains a relatively under-the-radar micro-cap operating at the intersection of India's housing,...

Arjun

Ashish Kacholia has built a reputation for identifying scalable businesses early, particularly in engineering,...

HFCL appears to be entering a new phase of growth driven by three structural...

Continued focus on expanding distribution channels and direct sourcing is expected to support business...

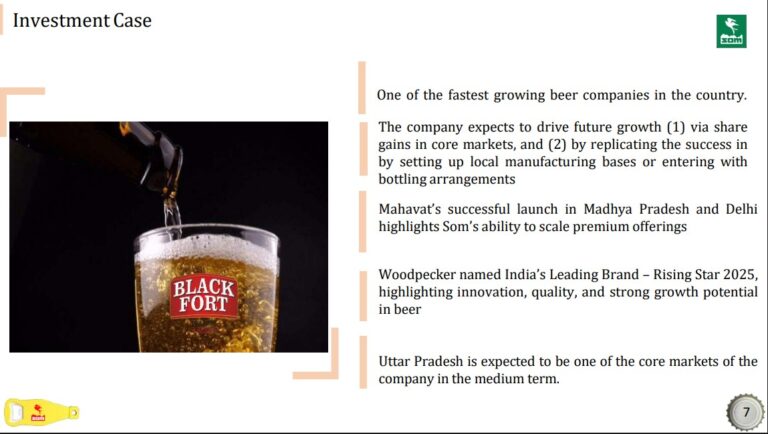

Despite recent setbacks, Som Distilleries continues to enjoy a strong position in the beer...

Despite global uncertainty, Vikas Khemani's long-term outlook remains firmly constructive.

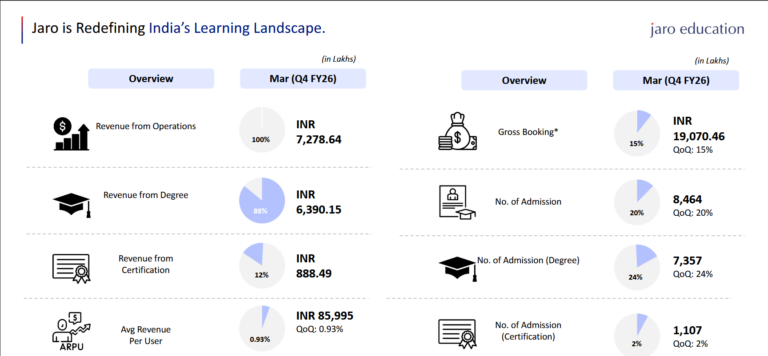

One of the biggest strengths highlighted by Deven Choksey Research is Jaro's capital-efficient business...

AFCOM Holdings has already rewarded early investors with extraordinary returns since its SME IPO.

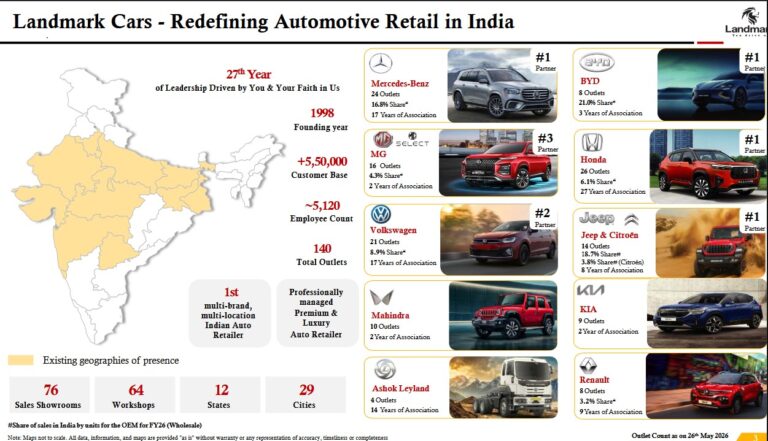

Helios Mutual Fund's purchase of a stake in Landmark Cars has once again drawn...

We expect the revenues and PAT to grow at a CAGR of ~30.5% and...