Sharda Cropchem appears to be entering a phase where business fundamentals are improving after...

Arjun

We upgrade our rating on BAF to BUY with a TP of INR1,300

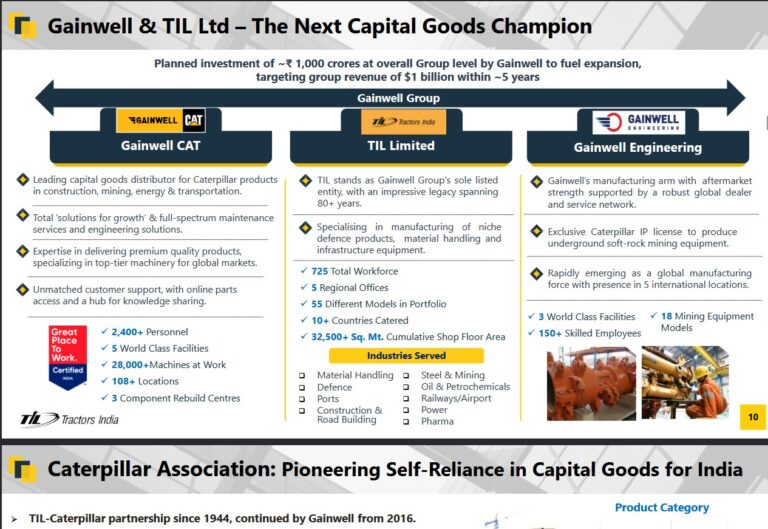

TIL today represents a classic turnaround story rather than a mature business.

Akash Bhanshali may not seek headlines or television appearances, but his investment track record...

TANFAC appears to be entering a transformational phase supported by large capacity expansions, improving...

Considering the favourable risk-reward profile, we maintain our BUY rating with a target price...

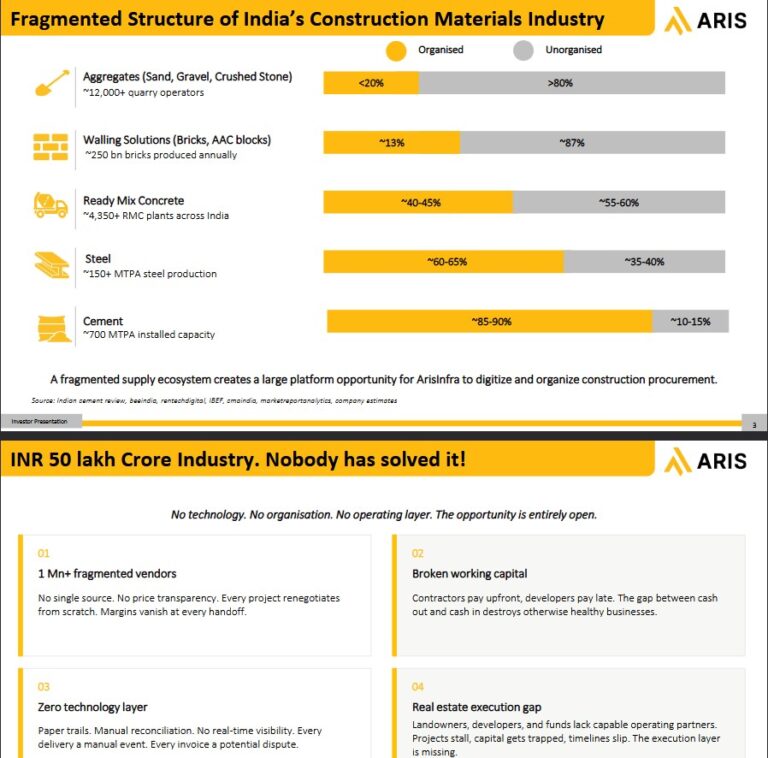

For investors with a higher risk appetite seeking emerging small-cap opportunities linked to India's...

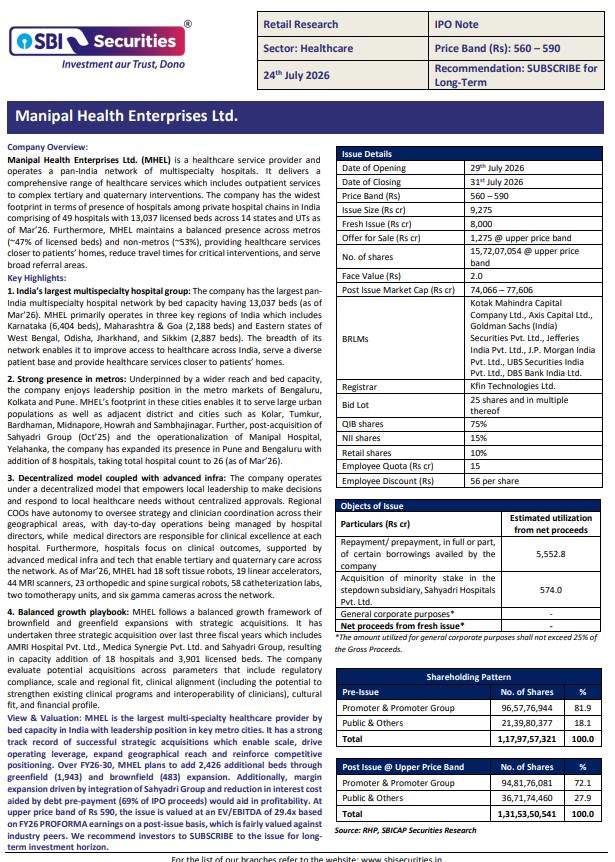

Manipal Health Enterprises (MHEL) is the largest multi-specialty healthcare provider by bed capacity in...

Indo SMC's robust quarterly performance, healthy order inflows, and exposure to structurally growing sectors...

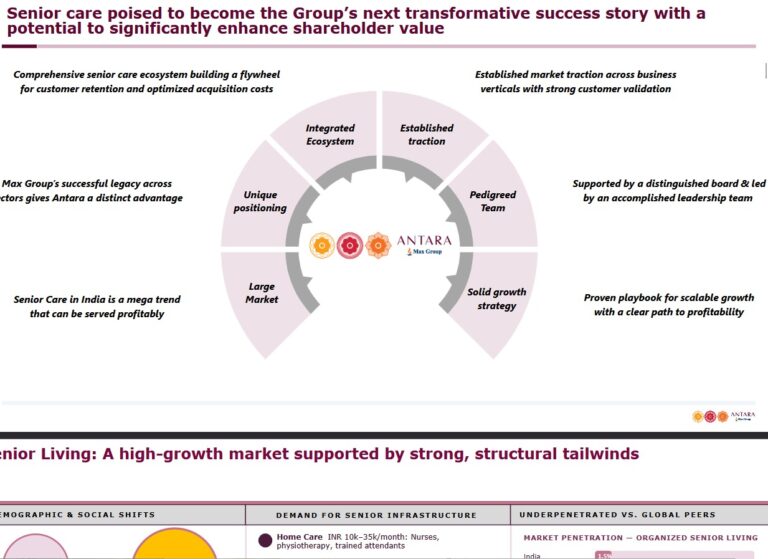

Madhu Kela's Singularity investing in Max India highlights increasing institutional confidence in India's emerging...