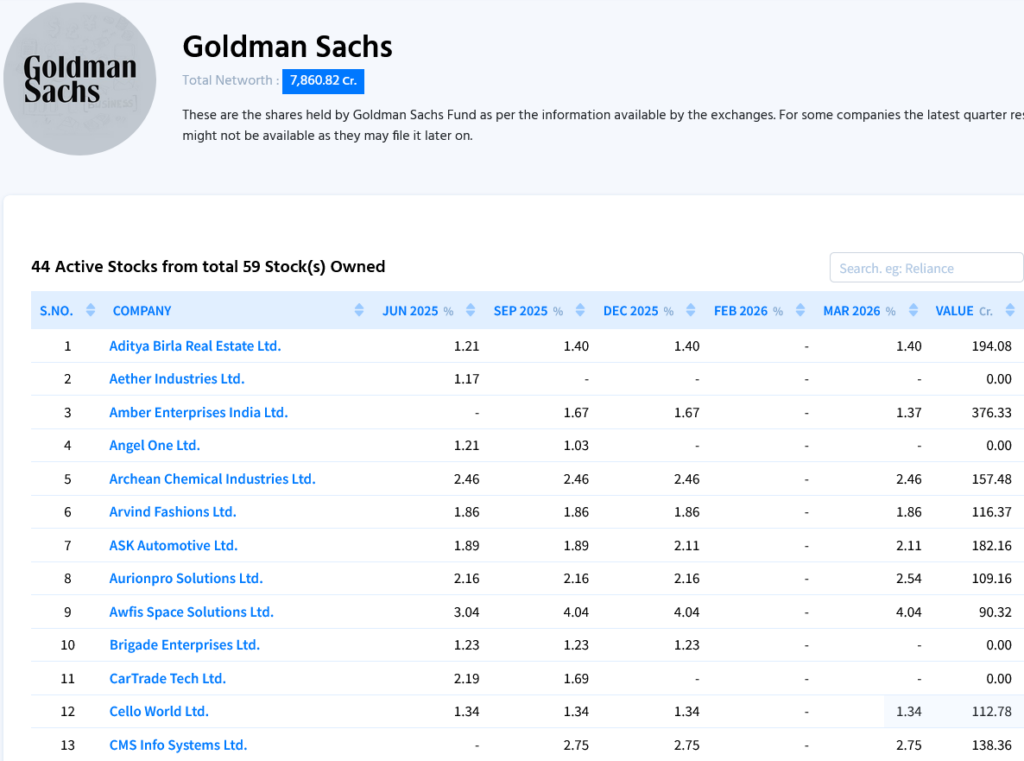

Global investment giant Goldman Sachs has built an impressive portfolio of Indian mid-cap stocks, with holdings worth around ₹7,860 crore. One of its recent notable moves has been adding exposure to Groww, the popular digital investment platform, with an investment of approximately ₹210 crore at around ₹185.5 per share.

Groww has emerged as one of India’s fastest-growing fintech platforms, especially among first-time investors and Gen-Z users. The company started as an online mutual fund investment platform and later expanded into discount broking, stocks, ETFs and other financial products. Its simple user interface, strong brand recall and focus on young investors have helped it gain significant traction in India’s rapidly expanding retail investment ecosystem.

India has witnessed a sharp rise in demat accounts and retail participation in capital markets over the last few years. The shift from traditional investing channels to digital platforms has created a large opportunity for companies like Groww. Rising financial awareness, increasing smartphone penetration and the growing popularity of systematic investment plans (SIPs) have further supported the sector’s growth.

The valuation, however, reflects high expectations. Groww is reportedly trading at around 40x FY27 earnings and about 32x FY28 earnings, indicating that investors are pricing in strong future growth. Analysts and market experts remain positive, believing that the company can benefit from the long-term expansion of India’s wealth management and brokerage industry.

Goldman Sachs’ investment highlights the increasing interest of global investors in India’s fintech theme. The firm appears to be betting that companies with strong digital platforms, scalable technology and a young customer base can become long-term beneficiaries of India’s financialisation trend.

While Groww’s growth story is attractive, investors will closely watch factors such as competition from other discount brokers, regulatory changes, customer acquisition costs and whether earnings growth can justify the premium valuation.