Jeena Sikho Lifecare Ltd

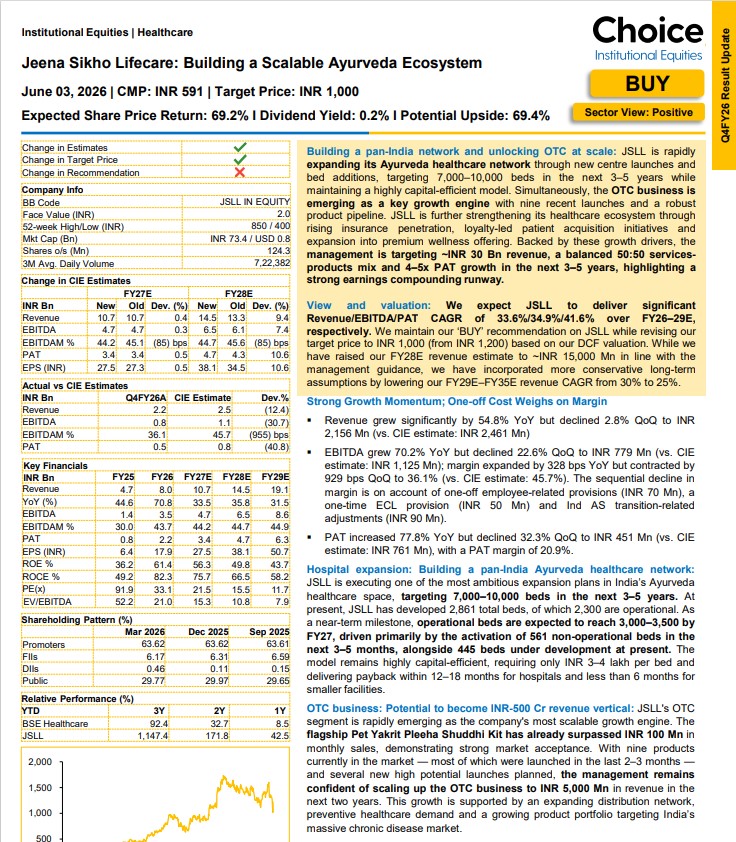

Jeena Sikho Lifecare Ltd. (JSLL), an emerging player in the Ayurveda and naturopathy healthcare space, has received a bullish view from Choice Institutional Equities, which has recommended a BUY rating on the stock with a target price of ₹1,000, implying an upside of around 69% from the current market price.

The company currently has a market capitalization of approximately ₹7,800 crore. The stock has delivered a remarkable performance over the last five years, rising nearly 3,270%, reflecting strong investor interest in the company’s growth story.

Building a Pan-India Ayurveda Healthcare Network

Jeena Sikho operates Ayurveda and naturopathy clinics across India and is focused on expanding its healthcare footprint. According to Choice Institutional Equities, the company is rapidly scaling its network through new centre launches and additional bed capacity.

The management aims to expand its capacity to 7,000–10,000 beds over the next 3–5 years while maintaining a capital-efficient operating model. The company’s expansion strategy focuses on increasing accessibility of Ayurveda-based treatments and creating a wider healthcare ecosystem.

OTC Products: The Next Growth Engine

Apart from healthcare services, Jeena Sikho is increasingly focusing on its over-the-counter (OTC) products business, which could become a major growth driver.

The company has already launched nine new products recently and has a strong pipeline under development. The OTC segment offers scalability as products can reach customers beyond the company’s physical clinic network.

The management is targeting a balanced business mix with approximately 50% contribution from services and 50% from products over the next few years.

Strong Capital Efficiency and Financial Outlook

One of the key strengths highlighted by Choice Institutional Equities is Jeena Sikho’s capital-efficient business model. The company reportedly delivers a strong ROCE of around 46%, indicating efficient utilisation of capital.

Choice expects JSLL to deliver strong earnings growth between FY26 and FY29:

- Revenue CAGR: 33.6%

- EBITDA CAGR: 34.9%

- PAT CAGR: 41.6%

The brokerage expects the company’s revenue growth to be supported by clinic expansion, higher patient volumes, increasing insurance penetration, loyalty-based customer acquisition and premium wellness offerings.

Long-Term Growth Ambition

The company’s management has outlined an ambitious growth roadmap, targeting approximately ₹3,000 crore revenue over the next 3–5 years along with a 4–5x increase in profit after tax (PAT).

The growth strategy includes:

- Expansion of Ayurveda healthcare centres

- Increasing bed capacity

- Scaling OTC product portfolio

- Premium wellness services

- Stronger digital and loyalty-driven patient engagement

Valuation View

Choice Institutional Equities has revised its target price to ₹1,000 from the earlier ₹1,200 target, based on a DCF valuation methodology. While the brokerage has increased its FY28 revenue estimates in line with management guidance, it has adopted more conservative long-term assumptions by lowering FY29–FY35 revenue CAGR expectations from 30% to 25%.

Investor Considerations

Jeena Sikho presents a combination of high growth, strong return ratios and an expanding healthcare opportunity. However, after a massive 3,270% rise in five years, valuation remains an important factor for investors to monitor.

Jeena Sikho presents a combination of high growth, strong return ratios and an expanding healthcare opportunity. However, after a massive 3,270% rise in five years, valuation remains an important factor for investors to monitor.

With promoters holding around 63.62% stake, strong ROCE, aggressive expansion plans and the potential scaling of its OTC business, the company remains a closely watched player in India’s growing Ayurveda and wellness sector.

(Disclaimer: This article is for informational purposes only and should not be considered investment advice.)