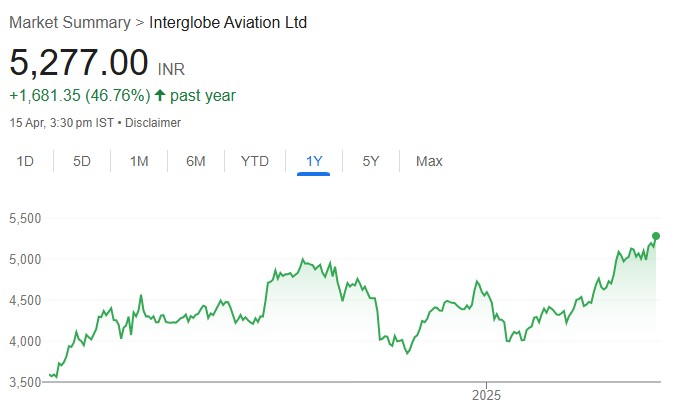

We upgrade INDIGO to BUY as we believe that benign Brent crude prices amid...

Arjun

The US Court of Appeals has vacated the preliminary injunction against Sun Pharma’s launch...

Sobha Ltd (SDL) delivered a sharp sequential recovery in Q4FY25 with presales of INR...

Hindustan Aeronautics (HAL) is a market leader in aerospace defense. It boasts a strong...

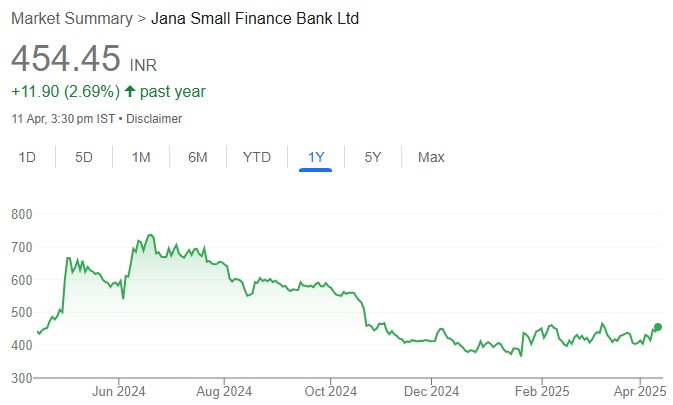

Jana Small Finance Bank (JSFB), since inception has focused on financial inclusion by serving...

Vishal Mega Mart’s (VMM) private label strategy in FMCG (~27% of revenue) has been...

Amidst the slowing down of banking sector earnings and a broader market sell off,...

Aditya Birla Real Estates (CENTEX), is the real estate arm of the Aditya Birla...

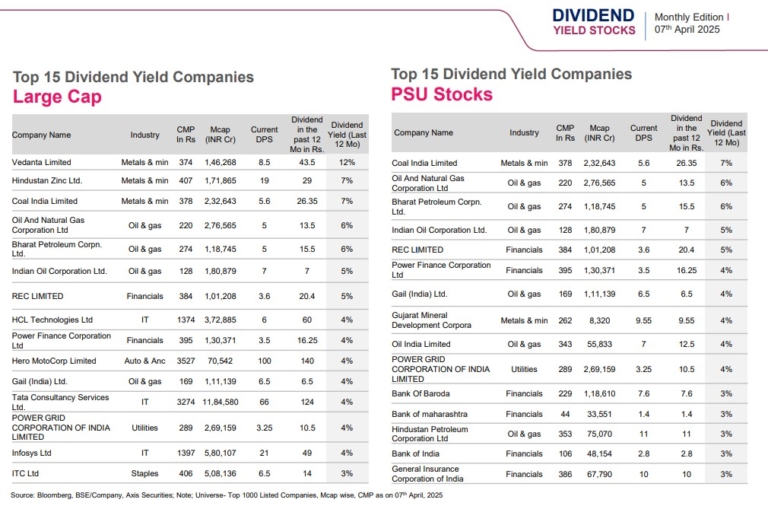

Top 15 Dividend Yield Companies in the Large-Cap, PSU, Mid-Cap and Small-Cap space. The...

PEPL has a diverse portfolio with a presence in residential, office, retail, and hospitality...