We remain positive on Coal India amidst healthy volume growth on anvil, superlative return...

Arjun

We firmly believe ACI is on the right track to expand into more critical,...

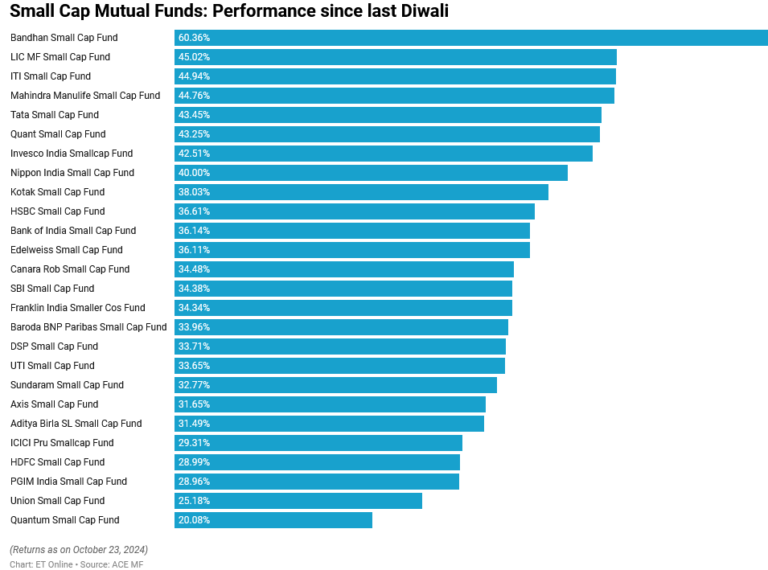

Bandhan Small Cap Fund is the topper in the small-cap category with a return...

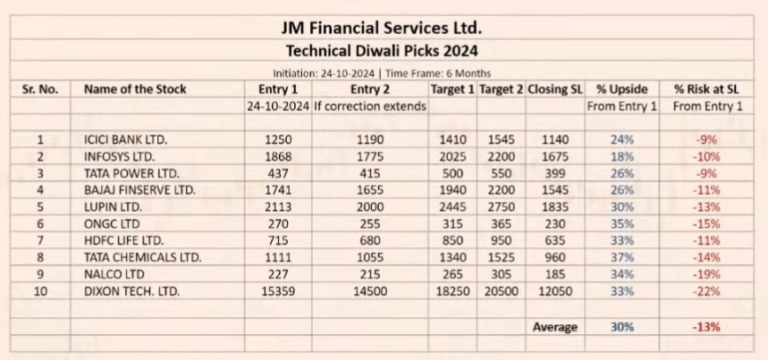

Rahul Sharma of JMFICS says the market (Nifty at 24000) is oversold & has...

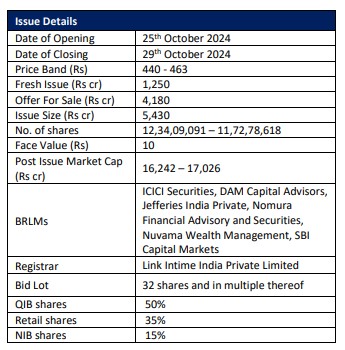

Afcons Infrastructure Ltd. (AIL) is a flagship infrastructure, engineering and construction company of Shapoorji...

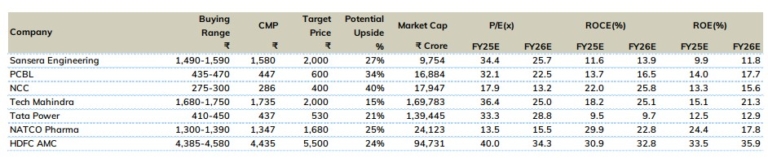

Keeping the key filter of quality and growth visibility, we continue to see reasonable...

Samvat 2081 is set to be a pivotal year for the global economy. We...

We believe that SAMVAT 2081 is likely to be bottoms-up stock pickers market. Investors...

RBL posted a miss in earnings (~33%) with PAT at Rs2.2bn/0.6% RoA, mainly due...

We initiate coverage of Genus Power Infrastructures Ltd. (GPIL) with a BUY recommendation and...