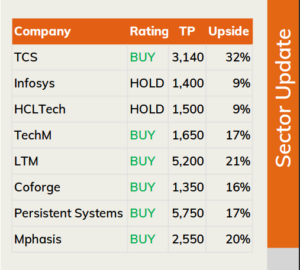

Best play on gas consumption

Our positive view on PLNG is based on strong volume growth

Our positive view on PLNG is based on strong volume growth

expectation. This view is not contingent on an upward trajectory for the Dahej regas margin or a strong marketing margin. Despite our conservative margin assumptions, we see an upside of 23% in this stock (will likely increase to 40% if the current margins were to continue). LNG continues to be competitive versus liquid fuel for the industrial segment, allaying concerns about soft demand for LNG.

Given PLNG’s competitive positioning and high earnings visibility, we reiterate BUY.

Competitive position: STRONG Changes to this position: STABLE

Regulatory risk factored in: Our view on PLNG is based on strong volume growth (FY13-FY20 CAGR of 11% v/s FY08-FY12 CAGR of 14%); it is not contingent on strong marketing margins or an increase in the Dahej regas margin. We believe consensus is unduly worried about the regulatory uncertainty; we see the worst case impact being limited to 15% of our valuation. In fact, most of the regulatory concerns are already factored in the current stock price (`151). As a result, PLNG is currently trading closer to our bear case valuation of `140. We see 23% upside despite our conservative assumption for marketing margin (at `10/mmbtu) and Dahej regas margin (flat at current levels). This upside could rise to 40% if PLNG earns a marketing margin of `15/mmbtu (FY12 margin: `22/mmbtu) and the Dahej regas margin continues to rise 5% annually to FY15 and remains flat thereafter.

Concerns over LNG demand overblown: The high cost of LNG versus coal and urea has led investors to question LNG’s demand growth potential. But as LNG would be used primarily as a substitute for liquid fuels in the industrial segment, there is little reason to worry (LNG is 11%-25% competitive v/s liquid

fuels). Further, we expect the industrial segment to consume up to 53% of the incremental gas demand over FY13-FY15 thereby providing enough scope for LNG demand growth. We are cognizant that Kochi is a new market for gas, hence we have assumed a gradual volume ramp-up at the Kochi terminal.

This is a relatively low-risk business model as PLNG does not bear volume or margin risk for 80-85% of its capacity due to long term (+20 years) and back-to-back contracts with LNG suppliers and gas off-takers.

Valuation: Using a DCF-based model we value PLNG at `185, which implies an FY13 P/E of 13.9x (5-yr average of 10.2x), FY13 EV/EBITDA of 9.1x (5-yr average of 7.4x) and FY13 P/B of 3.3x (5-yr average of 2.4x). Even though FY13-14 EPS growth can be muted due to capitalization of the Kochi terminal, we expect 20% EPS CAGR over FY15-FY20 driven by 14% volume CAGR. Key

catalysts: (a) clarity on regulatory uncertainty (expected over next 3-6months) and (b) signing of a substantial LNG purchase contract.

Download Research Report

[download id=”312″]