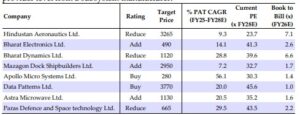

The stronger performance over FY24–25 (16%/19% PAT growth seen in FY24/FY25) has not really...

investments

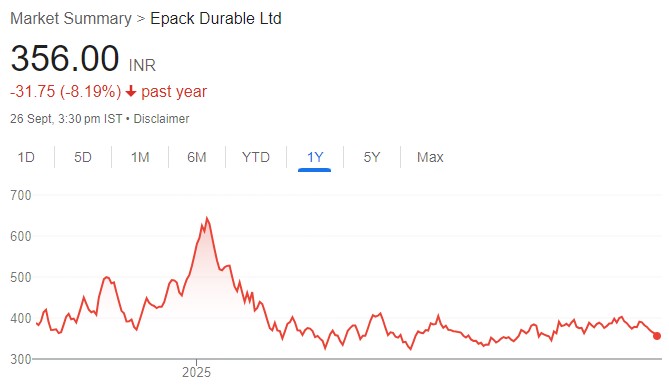

We initiate coverage on EPACK durable with BUY rating based on its commendable value...

Minda Corporation is evolving from a conventional auto component manufacturer into a high-value, technology-driven...

With RoE/RoCE above 26% and a net cash status, LOTUS stands out as the...

South Indian Bank is old south based private sector bank headquartered in Thrissur, Kerala....

We expect the company to report 17%/18% CAGR in Revenue/EBITDA over FY25-28E, aided by...

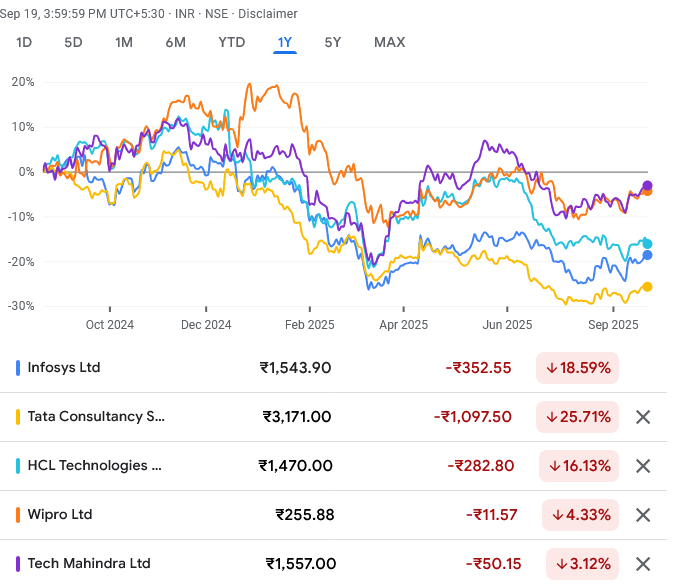

Our top picks are INFY, backed by superior pricing power, consistent execution, and a...

The company reported a robust pending order book of ~25GW as of Q1FY26, valued...

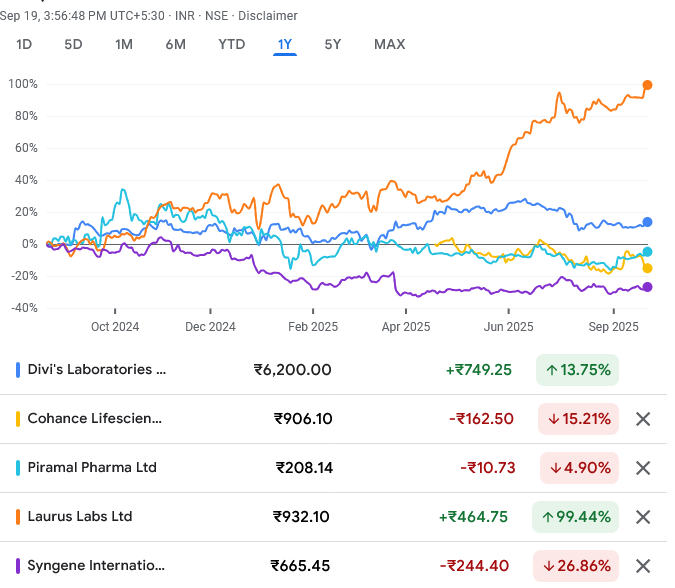

With strong fundamentals, capacity-led growth, and differentiated positioning, JP Morgan views both Divi’s Labs...

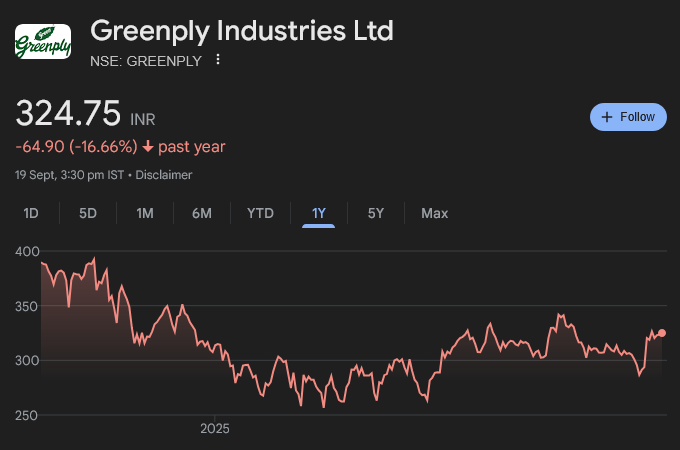

We reiterate GREENPLY INDUSTRIES LTD as our TOP-PICK from our coverage universe. We remain...