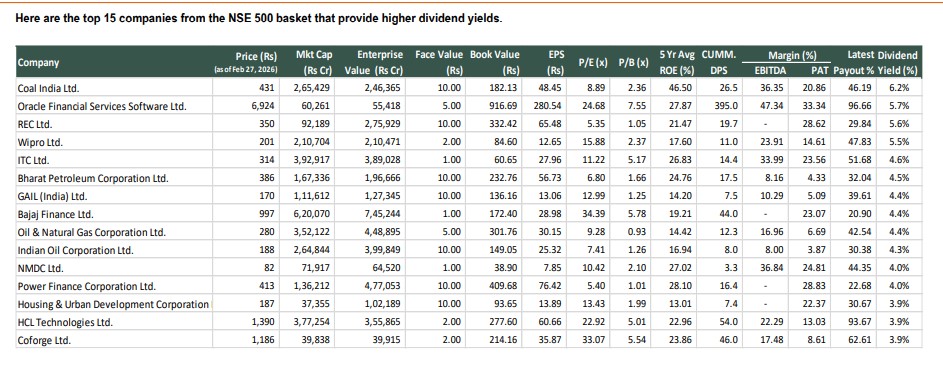

High Dividend yield of up to 6.2%

QUALITY DIVIDEND YIELD REPORT

Here are the top 15 companies from the NSE 500 basket that provide higher dividend yields.

QUALITY DIVIDEND YIELD REPORT

Here are the top 15 companies from the NSE 500 basket that provide higher dividend yields.