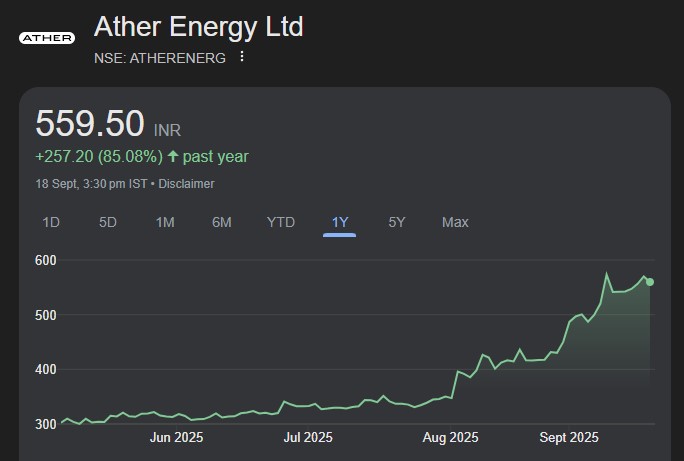

Strong growth with improving cost structure

The company is in a strong volume growth phase and is accelerating its efforts towards profitability. The current growth phase is aided by dealership expansion, as it is looking to reach 700 stores by the end of FY26, from 351 stores as of FY25-end. We expect another growth phase to start from late FY27 or FY28, which would then be led by portfolio expansion, with the expected addition of lower priced models on the new EL platform. On the profitability front, we expect benefits from operating leverage, move to lower cost LFP battery, move to the lower cost EL platform, better vertical integration at the new plant in Sambhajinagar, and better monetization of its software and accessories to help aid the company’s journey towards a positive EBITDA, and beyond. We upgrade the financials, with positive EBITDA now expected in FY28. Considering another inflection point from FY28, we factor that in the multiple and, hence, raise the EV/sales multiple from 5.0x to 6.0x, which is a premium to the listed peer set. We value the company at 6x Sep-27 EV/sales for a TP of Rs 748 and maintain BUY, while also maintaining the company as our top pick.