Aerospace segment continues to drive growth…

About the stock: Dynamatic Technologies (DTL), is primarily into designing and building highly engineered products for Automotive, Aeronautic, Hydraulic and Security applications. With manufacturing facilities are located in Europe and India, DTL caters to clients across six continents

Investment Rationale:

• Burgeoning growth opportunities in global aerospace sector: Aerospace segment (~47% of total revenue in 9MFY26) continues to be the leading contributor of the company, led by healthy demand for the products (includes wings, rear fuselages, wing flaps and other major aero structures and assemblies) from its global OEM customers (such as Airbus, Boeing, Bell Helicopters, Dassault Aviation, Deutsche Aircraft, HAL). As per Industry reports, there is global demand of 40000+ new passenger & freight aircrafts over the next 20 years. In India’s perspective, recently at Air Wings 2026 event, Airbus official stated that Indian carriers are expected to triple the size of their fleets to 2,250 jets over the next decade, riding on resilient economic growth, expanding middle-class and surge of first-time flyers. With the recent trade deals between India-US and India- Europe, sourcing from Indian aircraft components suppliers is expected to increase considerably in global aerospace market. DTL has also partnered with L&T-BEL consortium for 5th gen fighter jet project (Advanced Medium Combat Aircraft – AMCA), positions itself as one of the leading contenders in this project. We estimate revenue CAGR of ~28% over FY25-28E in this segment (as compared to ~19% CAGR over FY22-25)

• Recovery expected in hydraulics and metallurgy segments would further drive revenue growth and profitability: Hydraulics segment (~30% of 9MFY26 revenue) is also witnessing steady demand from tractor OEMs and industrial customers. Also, company continues to focus on operational restructuring, rationalization of product lines across Bangalore & Swindon, and cost optimization initiatives. We estimate revenue CAGR of ~7% over FY25-28E in this segment (as compared to ~3% CAGR over FY22-25). In Metallurgy segment (~22% of 9MFY26 revenue), though the operational performance has been impacted by weakness in German automotive sector, the company’s focus is on cost discipline and actively pivoting capacities towards higher-growth aerospace and defence applications. We estimate revenue CAGR of ~11% over FY25-28E in this segment (as compared to ~10% CAGR decline over FY22-25)

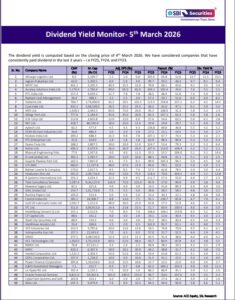

Rating and Target Price

• DTL is well positioned to witness healthy growth in aerospace segment (driven by strong industry tailwinds). Moreover, Hydraulics and Metallurgy segments are also expected to see meaningful recovery in coming period

• We estimate revenue CAGR of ~17% over FY25-28E with EBITDA margin improving gradually to 15.2% by FY28E (vs 11.3% in FY25), translating into EBITDA and PAT CAGR of ~29% and ~65% over the same period. We maintain our BUY rating on DTL with revised Target Price of ₹ 12700 per share (based on 45x FY28E EPS)