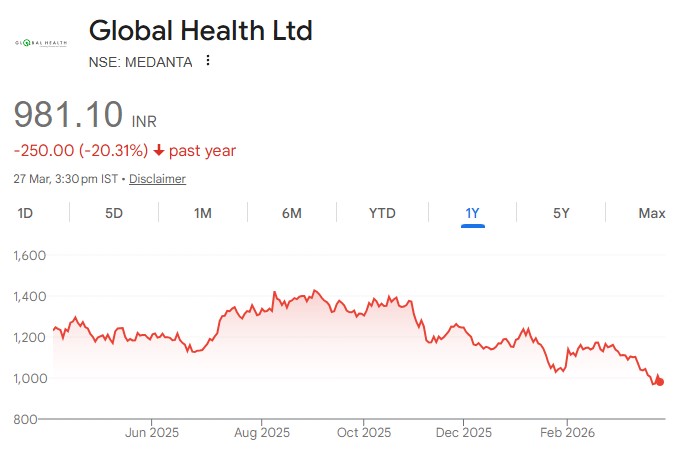

Correction creates entry; growth intact

The Medanta stock has corrected ~30% over the past six months and ~15% in the last month due to the launch of the Noida greenfield unit and recent geopolitical concerns stemming from the Middle East conflict. The stock is currently trading at 21x FY27E EBITDA, implying a 25% discount to its historical average. However, both the aforementioned factors are transitory and likely to normalise over the coming quarters. The company has limited exposure (~2% of sales) to Middle East patients, which can be offset through incremental domestic demand and inflows from other geographies. The Noida unit is progressing in line with expectations and with a clear path toward loss reduction, with potential breakeven by 1Q–2QFY27. Operationally, the company continues to be on a steady trajectory, supported by sustained strength in its core Gurugram facility and improving network occupancy (trending toward 60%), aided by a gradual ramp-up across newer assets. At the network level, Medanta’s strong quaternary care positioning continues to drive robust ARPPs, comparable to Max, alongside a broader plan to scale to ~6,382 beds by FY29 from 3,579 currently, underpinning operating leverage and EBITDA expansion over the medium term. Overall, we expect the company to deliver 14/26/32% revenue/EBITDA/PAT CAGR over FY26-28. With improving earnings visibility, margin expansion tailwinds and a more reasonable valuation backdrop, we value the company at 25x FY28E EBITDA and maintain a BUY rating with a target price of INR 1,382.