Sound and Fury: The AI Question!

Sector Overview

The Nifty IT index has witnessed a sharp correction over the past few months, declining ~25% YTD, primarily driven by rising concerns around the potential impact of Generative AI (Gen AI) on the long-term business model of IT services companies, along with macro and geopolitical uncertainties. Large-cap and midcap IT stocks have corrected meaningfully despite relatively stable operating performance and continued deal wins, as investors reassess near-term growth visibility and the potential structural implications of AI on traditional services delivery models.

However, historical technology transitions such as ERP adoption, cloud migration and digital transformation cycles suggest that while new technologies may initially compress revenue growth, they eventually expand the total addressable market (TAM) for IT services companies.

Long term opportunity outweighs impact: Gen AI is expected to significantly improve productivity in software development and maintenance, potentially reducing the number of engineers required for certain tasks. Industry commentary suggests that AI could lead to ~2–3% annual deflation in traditional services revenues for the next couple of years, as automation improves delivery efficiency & compresses effort-based pricing models. On the other hand, Industry estimates also suggest AI-led services could create an incremental TAM of USD300–400bn by 2030, representing a significant expansion relative to the current size USD 280 bn of the Indian IT services industry. It is also expected to create 170 mn jobs vs the 92 mn traditional jobs it displaces. As a result, the sector may face near-term growth moderation but stronger structural opportunities over the medium term. Thus, Gen AI is likely to reshape service delivery models but may also expand the overall technology services opportunity by accelerating automation and digital transformation initiatives.

On earnings front, Accenture delivered a steady Q2 gaining market share with strong deal momentum, reflected in record bookings, of US$22.1 billion. Overall, for Indian IT, it is neutral, the read-through remains of a gradual recovery, with major rebound likely to be back-ended, execution-driven and dependent on scaling of AI use cases from pilots to enterprise-wide deployments.

Valuation and Investment View

Following the sharp recent correction, most IT services stocks are now trading close to historically low valuation multiples, with market expectations already reflecting muted long-term growth assumptions. However, given the evolving demand environment and recent market movements, we have revisited our estimates and investment calls incorporating updated assumptions around revenues (2- 3% AI led revenue deflation in both FY27 & FY28), EBIT margins and EPS growth (Exhibit 4-7).

Along with revising our revenue and EPS estimates, we have also lowered our PE multiples (Exhibit 3) for the above stocks to reflect potential AI led revenue deflation and the delay/uncertainty in demand for traditional IT services.

That said, these stocks are currently trading at a steep discount to their 5-year average 1 year forward PE multiples (Exhibit 8), offering valuation comfort at current levels with limited downside risk.

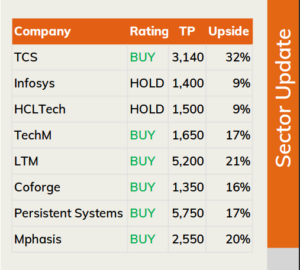

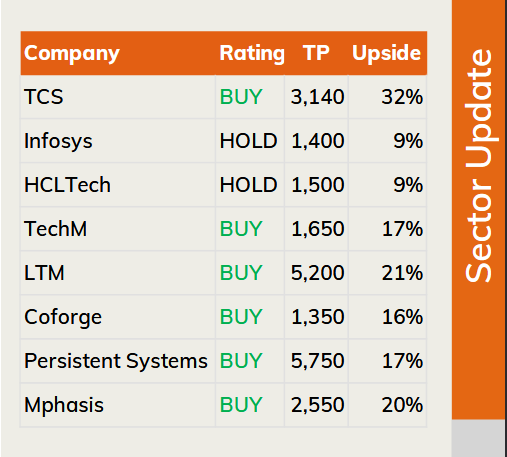

Our top picks in the sector includes Persistent Systems which is showing early monetisation traction in AI-led programs; LTM (erstwhile LTIMindtree) which has already absorbed productivity benefit passthrough and demand softness from a key client, potentially derisking future growth, and, TCS which is accelerating AI based investments/ capex to defend market leadership. We believe that staggered investments (over the next couple of months) in the selected IT stocks will yield strong returns over the next 18-24 months.