Vision FY30 lays roadmap for multi – year growth…

About the stock : Established in 2011, Muthoot Microfin Ltd., part of the Muthoot Pappachan Group, is the third-largest microfinance institution in India by AUM. The company primarily provides unsecured microfinance loans to women borrowers under JLG model and has gradually diversified into individual, MSME and other rural lending products through its pan-India distribution network.

• AUM mix: JLG loans – 82.5%; Individual loan – 17.1%; MSME LAP- 0.3%

Investment Rationale

• Customer – penetration strategy to drive the next growth cycle : Under Vision 2030, management aims to increase AUM from current ₹14,000 crore to ₹30,000 crore by FY30. Of this, ~₹11,700 crore of incremental AUM is expected from gaining wallet-share from existing customers with superior repayment track record for 1-2 cycle. New customer accretion is expected to garner remaining ~₹4,300 crore. Thus, next phase of growth is expected to be driven by deeper penetration within existing customer base rather than JLG-led customer acquisition. We believe customer-graduation model across MSEL, MSME LAP, gold and other products to support AUM CAGR of ~18–20% over FY26-28E.

• Portfolio repricing, funding optimization and productivity gains to drive profitability : Post yield pressure witnessed in FY25-26, we expect yields to improve by ~60 bps to ~23% by FY28E, led by repricing of back book, scaling up of higher-yielding disbursement and decline in NPA related drag. Cost of funds are expected to moderate to ~9.4% (vs. ~10.0%), aided by rating upgrade and access to low-cost securitisation markets, driving NIMs to ~14.3%. Deeper customer penetration, scaling of higher ticket size products and reduction of cash handling should improve productivity, driving operational efficiency to 5.9% (of AUM), thereby aiding operating profit CAGR of ~30% over FY26-28E.

• Building a more resilient portfolio across portfolio : A rising share of individually underwritten portfolio to seasoned customers supported by strengthened risk-management architecture including proprietary scorecards, AI-led underwriting, dedicated collections team and digital customer engagement are expected to aid asset quality and lower credit cost volatility. This along with deeper wallet-share within existing borrower is expected to drive further moderation in GNPA to 2.8% and moderation in credit cost by FY28E. This should support healthier return ratios, with RoA/RoE improving to 3.1%/14.9% by FY28E.

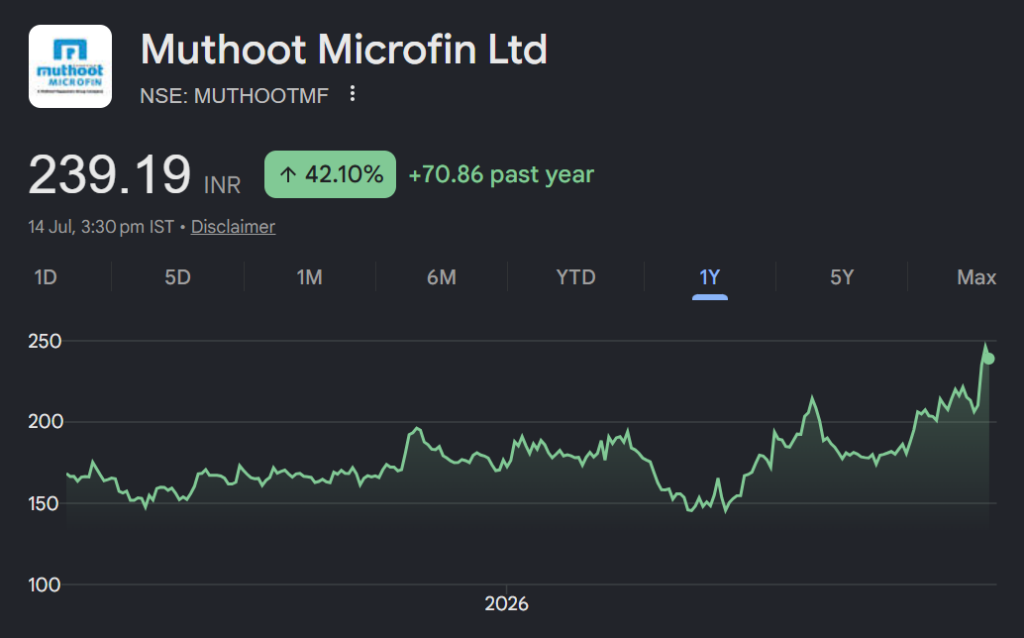

Rating and Target Price

• Muthoot Microfin is well placed to benefit from improving microfinance cycle, supported by its strong parentage, experienced management team, strategic customer penetration and calibrated expansion beyond JLG loans. Margin expansion driven by portfolio repricing, lower funding costs and normalization in credit costs, along with operating leverage, is expected to support a meaningful recovery in earnings over medium term. We value the stock at ~1.2x FY28E BV and assign BUY rating with a target price of ₹270