ELGi continues to generate approximately 100% EBITDA-to-cash conversion and maintains a strong net cash...

The company has strategically transitioned from a product supplier to a comprehensive solution provider...

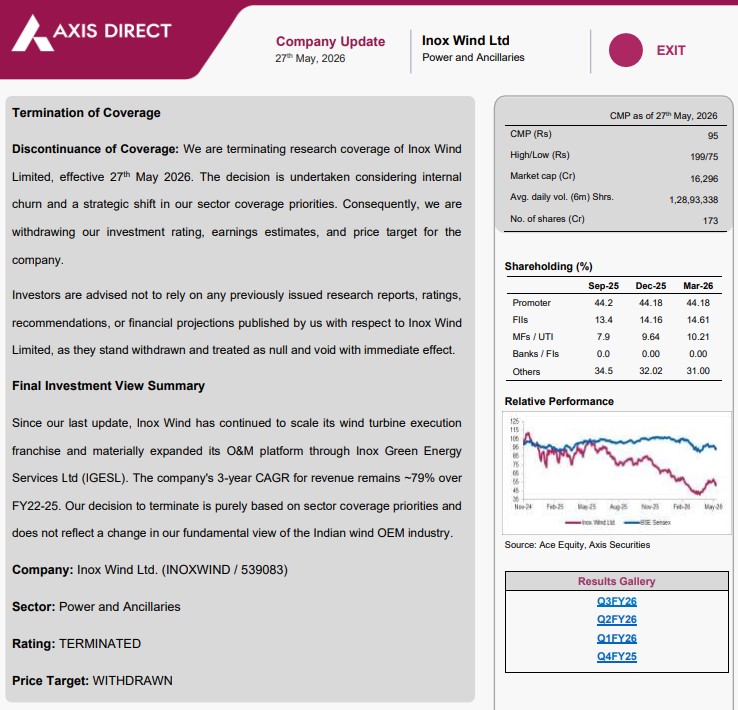

Part of the multi-billion dollar INOXGFL Group, Inox Wind is one of India's leading...

Shriram properties is expected to remain on a strong pre-sales growth trajectory over the...

The company added six new projects having cumulative GDV of ₹ 3410 crore. Of...

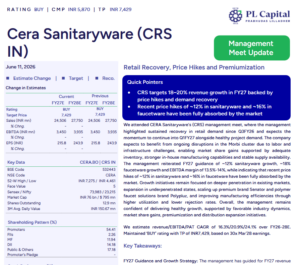

We remain constructive on the company given reasonable valuations and strong growth viability and...

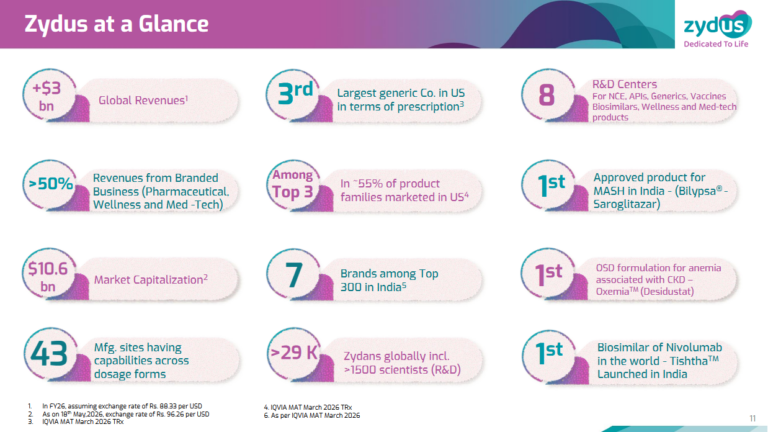

Zydus Lifesciences, headquartered in Ahmedabad, India, is an innovative, global pharmaceutical company that discovers,...

The company’s debt-free balance sheet, ongoing automation initiatives and planned capex towards defence and...

Prince Pipes and Fittings reported strong Q4FY26 performance with highest ever quarterly sales volume...

Sportking India (SKL) is a leading yarn manufacturer in India with 2 spinning units...