Vishal Mega Mart’s (VMM) private label strategy in FMCG (~27% of revenue) has been...

Amidst the slowing down of banking sector earnings and a broader market sell off,...

Aditya Birla Real Estates (CENTEX), is the real estate arm of the Aditya Birla...

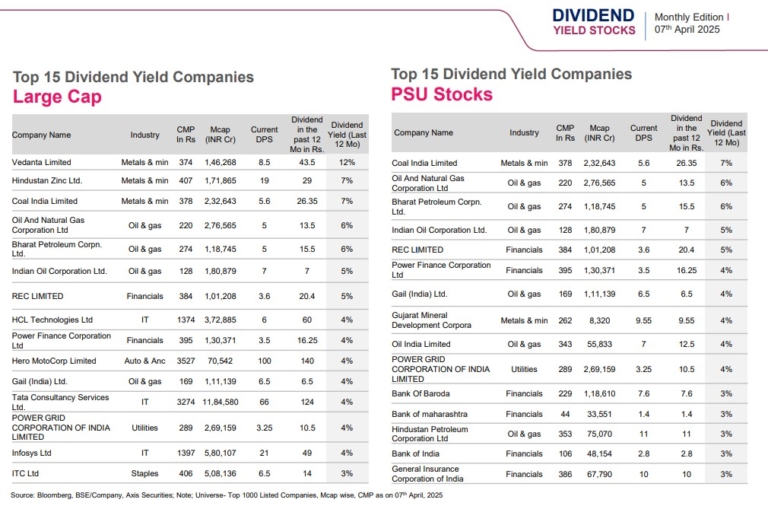

Top 15 Dividend Yield Companies in the Large-Cap, PSU, Mid-Cap and Small-Cap space. The...

PEPL has a diverse portfolio with a presence in residential, office, retail, and hospitality...

Adani Wilmar released a strong Q4FY25 business update ahead of our initial expectations. We...

Jubilant Pharmova (JPL) is an integrated, multi-dimensional pharmaceuticals company with global presence. The company...

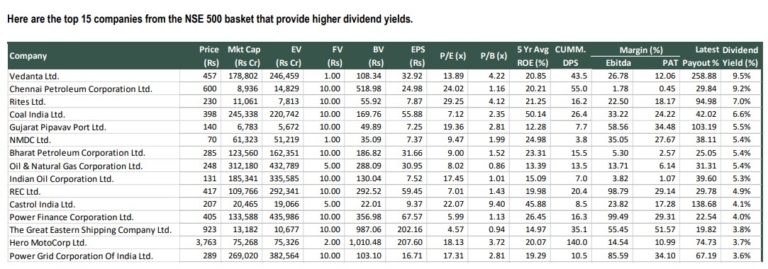

Here are the top 15 companies from the NSE 500 basket that provide higher...

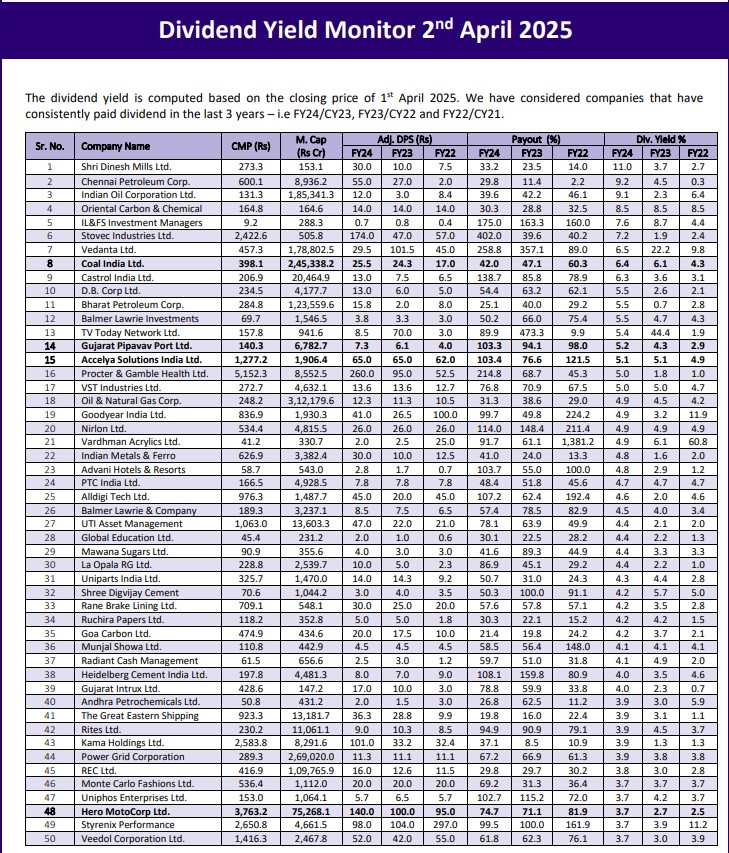

The dividend yield is computed based on the closing price of 1st April 2025....

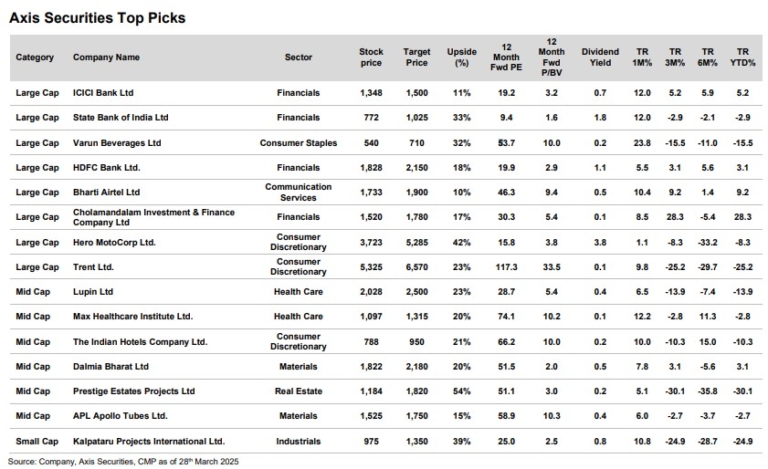

The Axis Top Picks Basket delivered an excellent return of 8.9% in Mar’25 against...