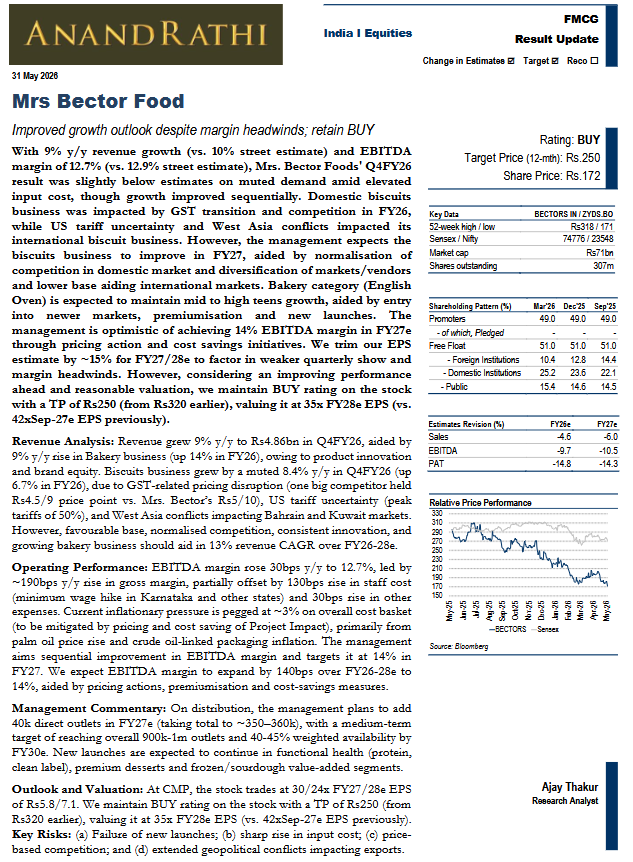

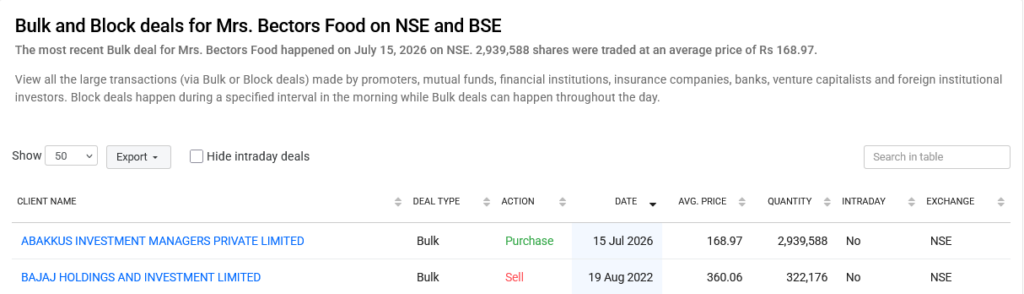

Ace investor Sunil Singhania’s Abakkus Asset Manager has increased its exposure to Mrs. Bector Food Specialities Ltd, acquiring a 0.96% stake at ₹168.97 per share in a bulk deal executed yesterday. The investment comes at a time when the stock has corrected nearly 35% over the past one year, taking the company’s market capitalisation to around ₹5,950 crore.

The purchase indicates growing institutional confidence that the recent weakness in the stock may be temporary and that earnings could recover over the next few years as demand improves and margin pressures ease.

Organised Biscuit Makers Continue to Gain Market Share

Mrs. Bector Food remains one of India’s leading premium bakery and biscuit companies with strong brands such as Cremica and English Oven. One of the structural tailwinds for the company is the ongoing shift in consumer preference from the unorganised to the organised sector.

The implementation of GST has steadily increased the competitive advantage of organised manufacturers, particularly in the biscuits segment. As tax compliance becomes stricter, smaller unorganised players are finding it difficult to compete on price, enabling branded companies like Mrs. Bector Food to expand their market share over time.

Strategy 2.0 to Drive the Next Phase of Growth

The company has unveiled its Strategy 2.0, aimed at accelerating growth through product innovation and premiumisation.

Management plans to introduce products in fast-growing categories such as:

- Functional nutrition products

- Protein-rich foods

- Clean-label offerings

- Health and wellness-focused snacks

These segments are witnessing strong consumer demand, particularly among urban and health-conscious buyers. The company expects these new launches to complement its existing product portfolio while improving overall profitability.

Q4FY26 Performance Slightly Below Expectations

According to Anand Rathi’s latest research report, Mrs. Bector Food reported 9% year-on-year revenue growth in Q4FY26, marginally below market expectations of around 10%.

EBITDA margin stood at 12.7%, compared with the Street expectation of 12.9%, as elevated prices of key raw materials continued to weigh on profitability.

Demand also remained subdued during the quarter.

The biscuits business faced multiple challenges during FY26, including:

- GST-related transition issues in the domestic market

- Intense competitive activity

- Tariff-related uncertainty affecting exports to the US

- Geopolitical disruptions in West Asia impacting international operations

Management Expects FY27 to Be Better

Despite the near-term challenges, the management remains optimistic about FY27.

Domestic biscuit demand is expected to recover as competition normalises following the GST transition. International operations are also likely to improve as the company diversifies both export markets and vendor relationships, reducing dependence on any single geography.

Meanwhile, the English Oven bakery business continues to be a bright spot. Management expects the brand to deliver mid- to high-teen revenue growth, supported by expansion into new markets, premium product offerings and continued innovation.

The company is also targeting an EBITDA margin of 14% in FY27, aided by selective price increases and various cost-saving initiatives.

Anand Rathi Retains BUY Rating

While Anand Rathi has reduced its FY27 and FY28 earnings estimates by around 15% to account for recent margin pressures, the brokerage believes the worst may now be behind the company.

The brokerage has retained its BUY rating, although it has revised its target price to ₹250 from the earlier ₹320, reflecting a more conservative earnings outlook.

The revised target still implies an upside of nearly 48% from the acquisition price of ₹168.97, suggesting that the brokerage expects earnings growth to improve as operating conditions normalise.

Investment Takeaway

Mrs. Bector Food has faced a difficult year due to rising input costs, GST-related disruptions and weakness in international markets, leading to a significant correction in its share price.

However, the combination of improving industry dynamics, a strong bakery franchise, expanding premium product portfolio and the long-term shift towards organised food companies provides reasons for optimism.

Sunil Singhania’s latest investment adds another layer of confidence, while Anand Rathi’s continued BUY recommendation suggests that the current weakness could offer an attractive opportunity for long-term investors willing to look beyond short-term earnings volatility.