Near-term Consolidation; Focus Remains on Style & Sector Rotation

The Axis Top Picks Basket delivered an excellent return of 14.2% in the last three months against the 12% returns posted by Nifty 50 over the same period. Moreover, the basket climbed up by 2.7% in the last one month. It gives us immense joy to share that our Top Picks Basket has delivered an impressive return of 338% since its inception (May’20), which stands well above the 172% return delivered by the NIFTY 50 index over the same period. In light of this, we continue to believe in our thematic approach to Top Picks selection.

FY25 – Good Start but Volatile Path Ahead; Macro to Remain at the Centre: Nifty reached an all-time high of 25,236 on 30th Aug’24. This impressive growth was driven by several factors including 1) Post-budget rally 2) Continued focus on Capex and other Infrastructure building, 3) Improved sentiments towards policy continuity, 4) Domestic inflows, 5) Valuation comfort after the correction, and 6) Q1FY25 earnings season in line with expectations, and 7) Strengthening of rate cut narrative in the global market. Aug’24 was a volatile month for the global market. In recent developments, the market experienced increased volatility during the first week of the month due to the unwinding of the Yen carry trade. However, later in the month, some recovery was seen across the world, supported by the strengthening narrative of the expectation of a rate cut in Sep’24. With this development, the IT sector saw some optimism towards the recovery in discretionary spending. In the last one month, our benchmark index Nifty 50 grew by 1.1% while the Midcap/Small Cap went up by 0.5%/1.2% respectively. Moreover, in FY25 so far, FIIs were neutral on the Indian market and invested $3 Bn while DIIs have invested $24 Bn over the same period. Mutual fund SIP contribution has crossed 23,000 Cr for the first time in Jul’24.

We Maintain our Mar’25 Nifty Target at 24600

Base case: In our Dec’23 Top Picks report, we upgraded the Dec’24 Nifty target to 23,000 with an upside potential of 14% from the Nov’23 closing. We are happy to say that we have successfully achieved the target well before the time. This indicates our confidence in the current macroeconomic cycle and the earnings growth. We continue to believe that, the Indian economy stands at the sweet spot of growth and remains the land of stability against the backdrop of a volatile global economy. We continue to believe in its long-term growth story, driven by the country’s favourable structure, thanks to the increasing Capex which is enabling banks to improve credit growth. This will ensure that Indian equities will easily manage to deliver double-digit returns in the next 2-3 years, supported by double-digit earnings growth. Against this backdrop, we foresee Nifty earnings to post excellent growth of 16% CAGR over FY23-26. Financials will remain the biggest contributors for FY25/26 earnings

In our base case, we maintained our Mar’25 Nifty target at 24,600 by valuing it at 20x on Mar’26 earnings. While the medium to long-term outlook for the overall market remains positive, we may see volatility in the short run with the market responding in either direction. Keeping this in view, the current setup is a ‘Buy on Dips’ market. Hence, any market correction on account of global challenges will be an opportunity to add to the equity investment.

Bull Case: In the bull case, we value NIFTY at 22x, which translates into a Mar’25 target of 27,000. Our bull case assumption is based on the Goldilocks scenario which presumes an overall reduction in volatility and the success of a soft landing in the US market. At present, we find ourselves near the peak of the current rate hike cycle and the outlook for a soft landing has notably strengthened over the last one to two months. The market is currently building an expectation of at least one rate cut by US FED in the remaining part of 2024 and developments regarding the same will be keenly watched by the Street. Furthermore, the private Capex, which has been sluggish for the last several years, is expected to receive a muchneeded push in the upcoming years with an expectation of policy continuity. In light of expectations of political stability, policy continuity, fiscal prudence path, private Capex cycle, rural revival, and soft landing in the US market, Nifty earnings are likely to grow at 17-18% over FY23-26. This would augur well for capital inflows into emerging markets (EMs) and would increase the market multiples in the domestic market. We believe the likelihood of this scenario is very high at the current juncture.

Bear Case: In the bear case, we value NIFTY at 16x, which translates into a Mar’25 target of 19,700. We assume the market to trade at an average valuation, led by political instability and deviation in policy continuity. Adding to that, we assume inflation to continue posing challenges in the developed world. Currently, we are near the peak of the rate hike cycle and the market has not seen such levels of interest rate hike in the recent past. Hence the chances to go wrong have increased significantly. If this scenario materializes, it would translate into a slowdown or heightened chance of recession in the developed market, which in turn, will impact export-oriented growth in the domestic market. Consequently, this will pose challenges to the earnings and market multiple of the domestic market. However, the likelihood of this scenario appears slim at the current juncture

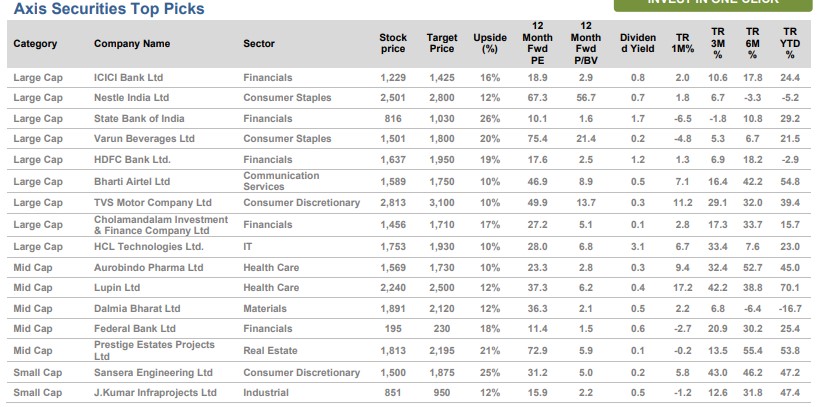

Based on the above themes, we recommend the following stocks: HDFC Bank, ICICI Bank, Dalmia Bharat, Nestle India, State Bank of India, HCL Tech, Lupin ltd, Aurobindo Pharma, Federal Bank, Varun Beverages, TVS Motors, Bharti Airtel, J Kumar Infra, Prestige Estates, Sansera Engineering, and Cholamandalam Invest and Finance