Kshitij Anand of ET has written an article in which he has spoken to leading stock market experts and also identified the best stocks being recommended for purchase now by investors.

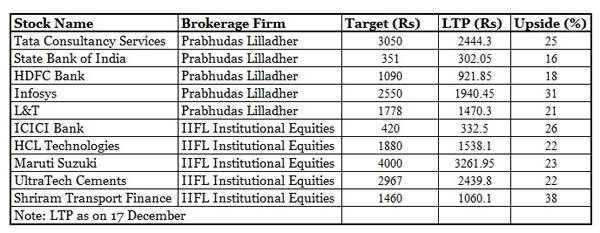

TCS: Target price Rs 3,050

According to the management, the quarter will see usual seasonality in-line with the previous year Q3. In terms of verticals, BFSI and retail verticals may witness usual seasonality, whereas telecom and smaller verticals would grow faster than company average, while insurance and energy is likely to witness weakness.

SBI: Target price Rs 351

SBI has reported a pick-up in growth in core operating profits (31% YoY), though NII growth has been slightly soft due to flattish trend in advances growth. Asset quality has showed some positive signs with stressed assets accretion moderating on sequential basis.

HDFC Bank: Target price Rs 1090

HDFC Bank’s earnings are expected to improve as significant investments made in branch expansion over past two years begin to show results, while a pick-up in loan growth and benign delinquency trend help keep credit cost under control.

Infosys Ltd: Target price Rs 2550

The management was confident of achieving industry leading growth with steady operating margin by Q1FY17. The stated objective of 15-18% YoY revenue growth with 25-28% operating margin is still in reach. Despite the investments on newer initiatives, the management was confident of retaining operating margin of 25% in narrow range of over 1%.

L&T: Target price Rs 1778

The company’s consolidated order inflow for the quarter was up 17 per cent, YoY, to Rs398 billion. The management highlighted that the domestic market has started to see some revival in sectors like power, oil & gas and transportation.

ICICI Bank: Target price Rs 420

ICICI Bank is well positioned to benefit from the recovery in the economy and flexible structuring of long-term project loans. This would reduce the risk of infrastructure loans.

HCL Technologies Ltd: Target price Rs 1800

HCL Technologies’ revenue growth will be among the best in Indian IT. Margins are likely to be stable over FY15-17, following a sharp increase over the past three years. They estimate a robust 15 per cent EPS CAGR over FY15-17. Despite such strong fundamentals, valuations are the cheapest in the peer group.

Maruti Suzuki India Ltd: Target price Rs 4000

Maruti is the best OEM play on macro-economic recovery in India. Following flat volumes for the past four years, the brokerage firm expects car sales to bounce back, led by high pent-up demand, economic recovery and deceleration in car ownership costs.

UltraTech Cements Ltd: Target price Rs 2967

UltraTech Cements is expected to report a 26 per cent earnings CAGR for FY14-FY17 driven by 1) increased pricing power for cement producers with an improvement in industry demand; 2) increased volumes driven by new capacity additions and 3) improved efficiency led by a cost reduction programme.

Shriram Transport Finance: Target price Rs 1460

Operating environment for Shriram Transport is at the cusp of change. Improvement in the finances of SHTF’s borrowers, uptick in demand for loans and reduction in NPL’s and funding costs are likely to drive a sharp improvement in the company’s earnings and profitability over the medium term.