Porinju Veliyath has made yet another of his famous predictions. In the past, we...

Mid Cap

The trio of Porinju Veliyath, Shyam Sekhar & Ekansh Mittal has raked in enormous...

Mudar Patherya's previous stock recommen dations have yielded huge gains. He has now recommended...

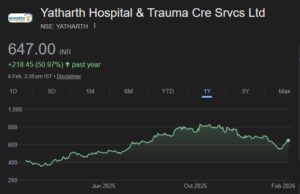

Porinju Veliyath & Shyam Sekhar are sitting pretty in a nano-nivesh stock of impeccable...

Narendra Nathan of ET has spoken to leading experts and identified eight top-quality stocks...

Dolly Khanna has broken her long-standing rule of not investing in banking and NBFC...

Porinju Veliyath & Shyam Sekhar turned contrarian at precisely the right time and bought...

Dharmesh Kant and G. Chokkalingam have recommended four stocks as being worthy of investment

Kshitij Anand of ET has spoken to leading experts and identified five cheap stocks...

Nirmal Bang has issued a detailed research report in which it has recommended several...