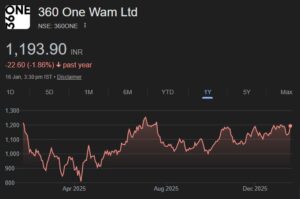

Strong inflows; operating leverage drives CI ratio down

360 One WAM (360ONE) reported 3QFY26 operating revenue of INR8b (in line), up 33% YoY. For 9MFY26, revenue grew 24% YoY to INR22.3b. Revenue growth was driven by 45% YoY growth in ARR income to INR6.2b (7% beat) and 4% YoY growth in TBR income to INR1.9b (17% miss).

Cost-to-income ratio at 49.6% declined 320bp YoY (est. 52.6%), resulting in 7% beat in 3Q operating profit at INR4.1b. For 9MFY26, operating profit grew 19% YoY to INR10.8b.

The 63% miss in other income at INR200m resulted in PAT of INR3.3b (in line), which grew 20% YoY. For 9MFY26, PAT grew 22% YoY to INR9.3b.

Management is targeting a 120-150bp CI improvement in core business (with a similar improvement in new businesses) and aspires to reach a 45- 46% CI ratio next year. It aims to achieve 22-24% AUM growth, which should lead to 16-18% revenue growth and 22-24% PAT growth.

We have largely maintained our estimates and we expect the company to report FY25-28 revenue/PAT CAGR of 21%/22%. We adopt the SoTP approach, valuing ARR at 38x FY28E PAT and TBR/other income at 20x FY28E PAT, to arrive at a fair value of INR1,400. Reiterate BUY.

Valuation and view

360ONE offers a compelling structural growth story anchored to India’s expanding wealth and asset management market. The company continues to garner strong gross flows across both wealth and asset management, which is likely to be supported by the onboarding of new teams. The recent acquisition of B&K and the UBS collaboration enhance the company’s international footprint, broaden client access, and strengthen its transactional platform. Operating leverage and cost synergies from integrations are expected to improve profitability as new businesses scale up.

We have largely maintained our estimates and we expect the company to report FY25-28 revenue/PAT CAGR of 21%/22%. We adopt the SoTP approach, valuing ARR at 38x FY28E PAT and TBR/other income at 20x FY28E PAT, to arrive at a fair value of INR1,400. Reiterate BUY.