Market share gains in roofs; value enhancement to lift margins

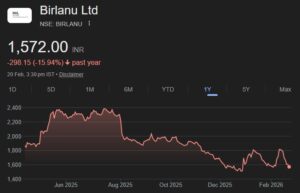

BirlaNu Ltd. (BirlaNu) reported a weak performance in Q3FY26, with consolidated revenue increasing ~6.5% YoY to ~Rs 8.57 bn due to a subdued demand environment and a soft pricing regime across key product categories. Margin performance improved YoY in roofs & pipes & construction chemicals segments, supported by focused initiatives on sales acceleration, cost discipline and profitability enhancement, even as industry headwinds persisted. The India business remained the key growth driver, delivering ~7% revenue growth along with a ~240 bps YoY margin expansion. Within segments, walls posted strong momentum with revenue growth of ~18% YoY, led by higher traction in panels and boards, while construction chemicals continued to scale rapidly with a robust ~49% YoY growth. The roofs business also delivered industry-beating growth of about ~7% YoY and gained roughly 200 bps in market share, reinforcing the strength of its brands and distribution network. The pipes segment, however, remained under pressure with revenue declining ~6% YoY due to continued softness in resin prices, although sustained cost control measures aided profitability and early signs of demand recovery emerged as resin prices began to rebound toward the end of the quarter. The Parador flooring business registered modest ~5% YoY revenue growth but saw margin compression due to pricing pressures and higher input costs, prompting management to implement portfolio calibration and tighter operational discipline to support gradual recovery.

During the quarter, the company also completed the acquisition of Clean Coats and reported smooth integration progress, while strategic initiatives such as the AP Boards plant execution, OPVC commercialization and multiple new product launches across construction chemicals and designer boards strengthened the medium-term growth pipeline. At the consolidated level, EBITDA and PAT losses widened YoY, reflecting ongoing pricing pressures and investment phase dynamics.

Management remains cautiously optimistic on demand recovery, with a continued focus on execution excellence, capital efficiency and structural profitability improvement, supported by a comprehensive value enhancement program expected to deliver more meaningful benefits from Q1FY27 onward.

The company has taken significant steps to enhance operational efficiencies including improvements in sourcing, cost management and value enhancement initiatives. HIL has rebranded to BirlaNu which represents management’s aspiration to make the company a leading global provider of innovative, sustainable home & building solutions. Management aims to double the consolidated revenue of the company over the next three years and long term vision is to achieve USD 1 bn revenue.

Outlook and Valuation: Considering BirlaNu dominant market position in the domestic fiber cement sheet industry and its vision to achieve USD 1 bn revenue, we continue to value the stock at 15x FY28e EPS of Rs. 135.8 to arrive at a target price of Rs. 2037. We continue to maintain our “Buy” rating on the stock.

BirlaNu Ltd – Q3FY26 Result Update – SMIFS Institutional Research