Performance above our estimates; ECD outperforms

Enters residential wires segment; launch in six weeks in select markets

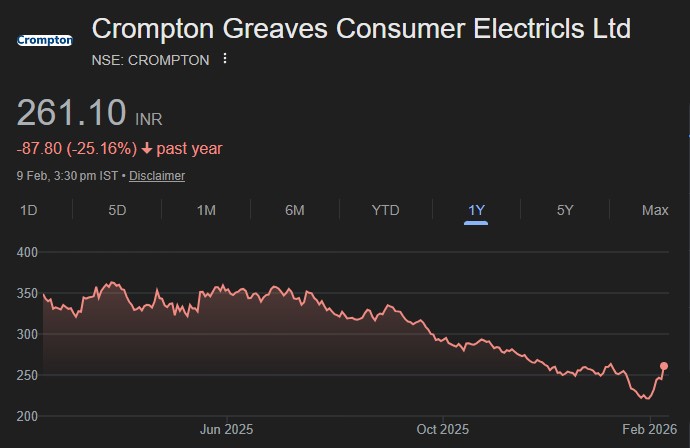

Crompton Greaves Consumer Electricals (CROMPTON)’s 3QFY26 earnings were above our estimate, driven by better-than-estimated performance in the ECD segment. EBITDA increased ~4% YoY to INR1.9b (~14% beat). OPM contracted 30bp YoY to 10.3% (vs. est. 9.3%). Adj. PAT after MI increased ~3% YoY to INR1.1b (~19% beat).

Management indicated CROMPTON’s disciplined strategy of entering adjacencies where it can build leadership through scale, distribution, and brand strength. The company has a proven track record across fans, pumps, lighting, appliances, kitchens, and solar. It has currently announced the launch of residential wires, a large market with strong adjacency, and is leveraging its pan-India distribution and dealer network. The products would be rolled out in select markets over the next 6-7 weeks. It has also executed a seamless BEE-2 transition in ceiling fans, effective Jan’26. Financial performance has seen a recovery QoQ in 3Q, driven by volume and margin improvement in ECD and sustained strength in lighting.

We recently initiated coverage on CROMPTON with a BUY rating (Initiating Coverage). We raise our EPS by ~5% for FY26E, while retaining it for FY27E/ FY28E. We value CROMPTON at 33x FY28E EPS to arrive at our TP of INR350. Reiterate BUY.

ECD revenue and margin better than our estimates

CROMPTON’s consol. revenue/EBITDA/ Adj. PAT stood at INR19.5b/INR2.0b/ INR1.1b (+7%/+4%/+3% YoY and +3%/+14%/+19% vs. our estimate). Gross margin dipped 1.1pp YoY to ~32%. OPM declined 35bp YoY to ~10.3%.

Segmental highlights: 1) ECD: Revenue surged ~8% YoY to INR13.8b, while EBIT declined ~8% YoY to INR1.8b (~13% beat). EBIT margin declined 2.2pp YoY to ~13% (est. ~12%); 2) Lighting: revenue grew by ~7% YoY to INR2.8b. EBIT increased ~20% YoY to INR333m. EBIT margin increased 1.3pp YoY to ~12%; and c) Butterfly: revenue increased by ~7% YoY to INR2.4b. EBIT increased ~14% YoY to INR140m. EBIT margin expanded 40bp YoY to ~6%.

In 9MFY26, CROMPTON’s revenue/EBITDA/PAT stood at INR58.1b/INR5.5b/ INR3.2b (flat/-12%/-17% YoY). OPM dipped 1.2pp YoY to ~9%. The ECD revenue declined ~1% YoY to INR43.4b, and EBIT declined ~19% to INR5.4b. The ECD margin contracted 2.6pp to ~12%.

Key highlights from the management commentary

It continues to gain market share across categories, with particularly strong momentum in BLDC fans. CROMPTON also emerged as the second-largest water heater brand.

ECD performance was led by strong solar pump execution, volume growth in LDA, and continued improvement in SDA. Lighting growth was supported by ceiling lights and accessories, together with new product launches.

Commodity cost inflation persisted during the quarter, prompting pricing actions, with further calibrated increases expected to offset cost pressures.