Key Highlights of the 3QFY26 Result

Robust Infra demand provides support to earnings, Defence & Auto verticals to pick up pace!

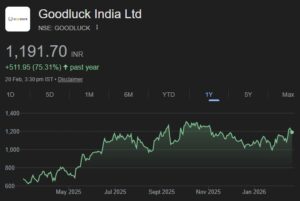

Goodluck India Ltd. during 3QFY26 reported a 10.1%/26.1%/6.0% YoY increase in Revenue/EBITDA/PAT to Rs 1,037 cr/101 cr/Rs 44 cr respectively. During the quarter, the company registered sales volume of 1,20,196 MT, up 8.2% YoY led by healthy demand from the Infra & Engineering sector, particularly from solar tracker tubes and other value-added products.

Defence & Aerospace production started, major capex ahead: The Defence & Aerospace vertical has successfully commenced production, and the first order is ready for dispatch, currently awaiting necessary permissions. The vertical possesses strong visibility over the next 4-5 years given the current demandsupply mismatch (demand is outstripping supply). Additionally, the vertical is fully booked for the next 12 months, supported by the government’s strong push on indigenous defence manufacturing.

In light of these advancements, the management has decided to augment the annual capacity from 1,50,000 shells currently to 4,00,000 shells, alongside the addition of a small capacity for manufacturing value-added aerospace components. This incremental capacity shall be operational by 1QFY28, with an estimated capex outlay of ~Rs 400 cr, which will be funded through a mix of debt and equity (40% debt:60% equity).

Softer tariffs likely to boost up auto export prospects: Volumes from the Precision pipes and Auto tubes segment are expected to be positively impacted given the recent easing of US tariffs on Indian exports. The Hydraulic tubes plant operated with a capacity utilization of ~45% during the quarter. However, we expect the plant to clock 60%-65% utilization over the next few quarters, given the steep reduction in tariffs. Going forward, upon reaching 80% utilization, the company plans to augment capacity by an additional 50,000 MT, raising the total to 2,20,000 MT.

Strong Infra-led support: The company’s Infra-led order book is booked for the next 12-18 months, led by increased domestic infrastructure investments and high-speed rail expansion. In the Union Budget 2026-27, announcements were made for 7 new bullet train corridors, and given the company’s prior success in completion of the first bullet train project, Goodluck India is well-placed to participate in the upcoming projects.

Maintain BUY- Target Rs 1,531/-

At the CMP of Rs 1,209, the stock is trading at a P/E of 22.8x/19.6x/11.1x of its FY26E/FY27E/FY28E EPS of Rs 53.1/Rs 61.6/Rs 109.3 respectively. We roll forward our FY28 estimates and value the stock at Rs 1,531, implying an upside of 26.6% from CMP of Rs 1,209, bas ed on FY28E P/E multiple of 14.0x.