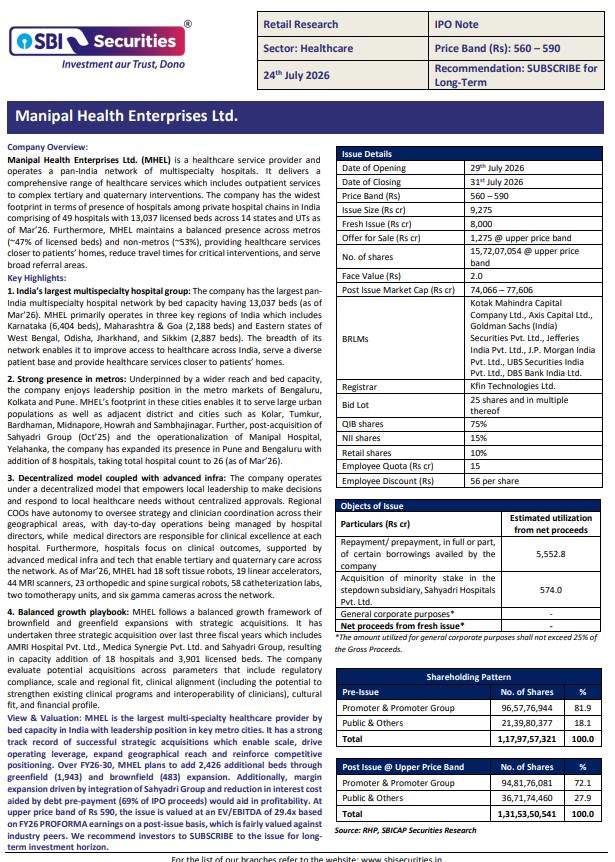

Manipal Health Enterprises (MHEL) is the largest multi-specialty healthcare provider by bed capacity in...

SBI Securities research reports

IMFA is India’s leading fully integrated producer of value-added Ferro Chrome (FeCr) - a...

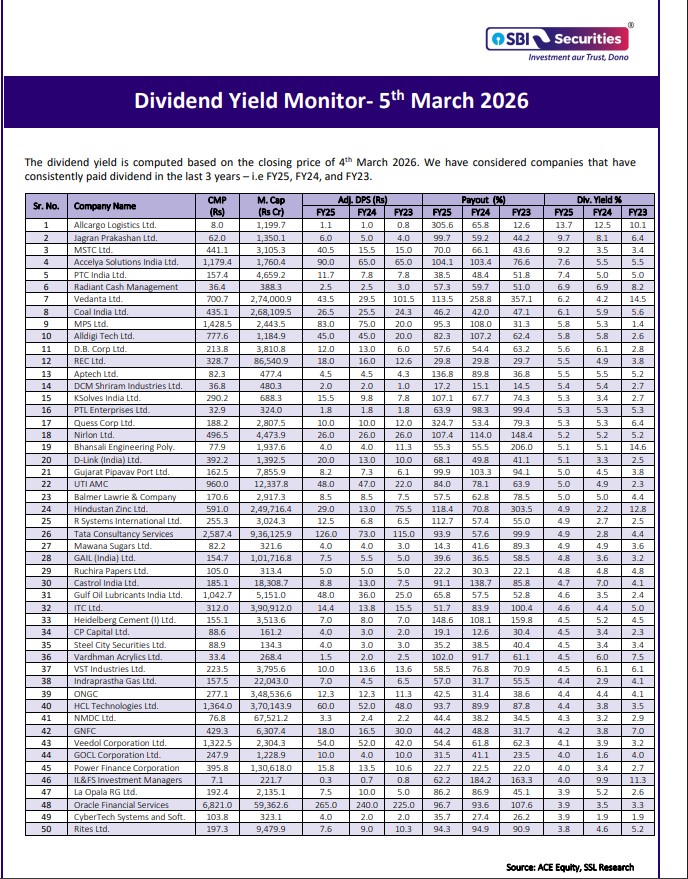

The dividend yield is computed based on the closing price of 4th March 2026

In the Union Budget 2026-27, announcements were made for 7 new bullet train corridors,...

The 2 acquired subsidiaries – IAC India and GreenFuel Energy continue to drive growth...

As of Dec’25, MAN’s aggregate executable order book stands at ~Rs 4,000 cr, providing...

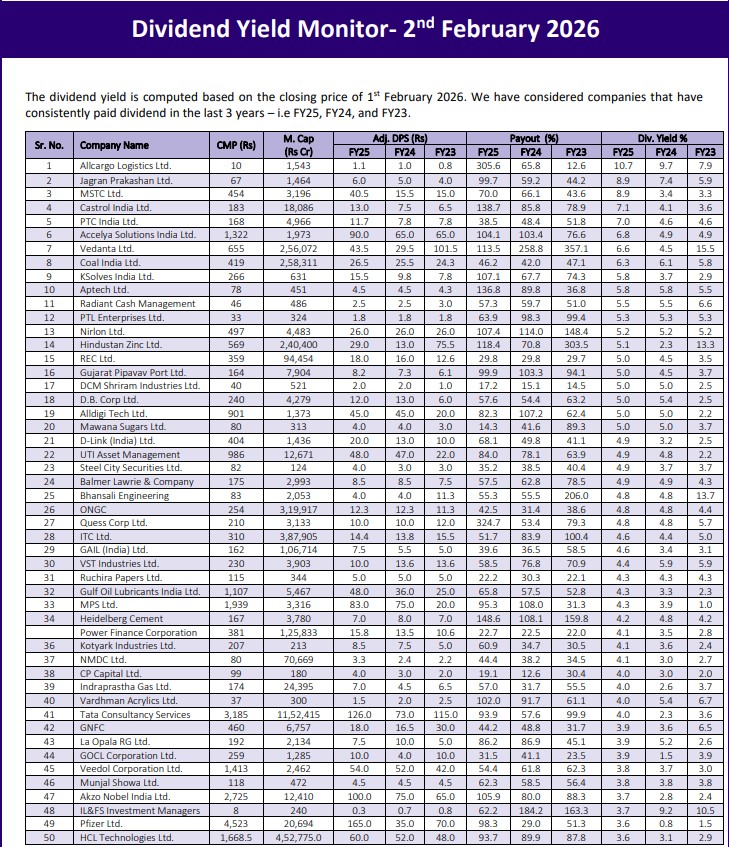

dividend yield is computed based on the closing price of 1st February 2026

The company is on track to expand its production capacity from 5 Mn ton...

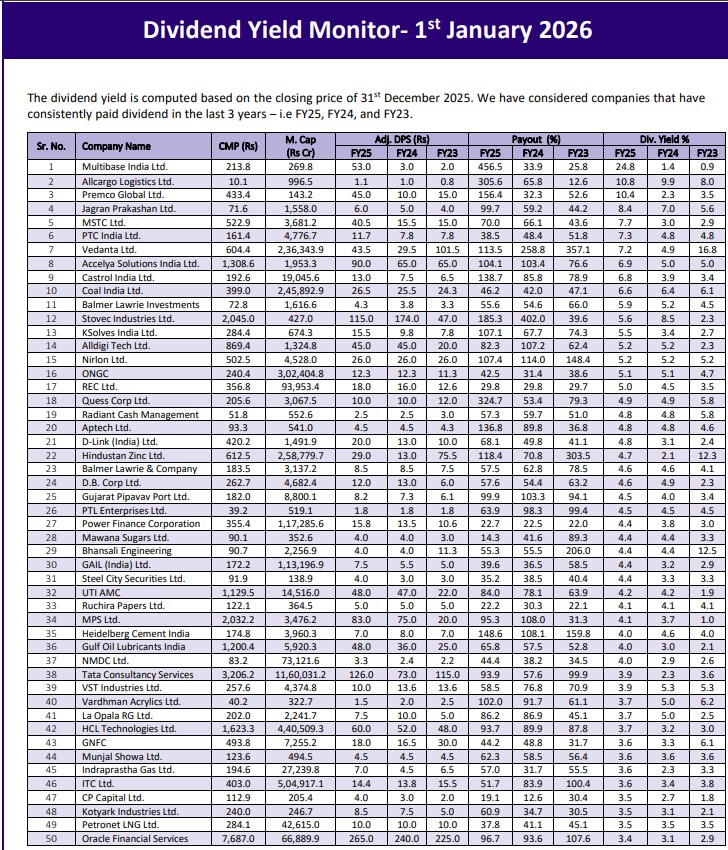

Multibase India Ltd has paid Rs 53 per share as interim dividend in Nov’24

MAN’s aggregate executable order book stands at Rs 4,750 cr,