‘REDEVELOPING’ INTO REAL ESTATE SPACE

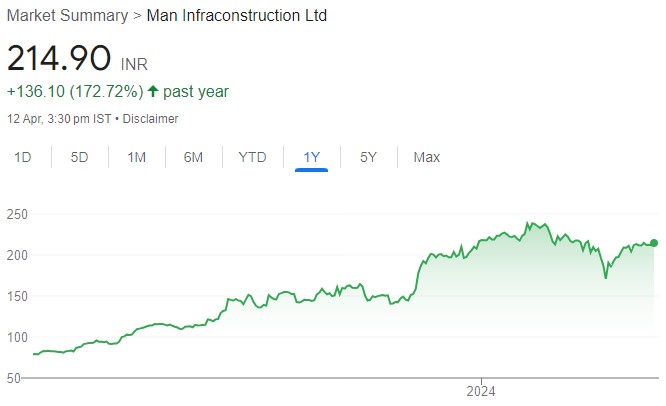

We are initiating coverage on Man Infraconstruction Ltd. (MICL) with a BUY recommendation and a target price of Rs 270/share, which implies an upside of 28% from the CMP. With roots tracing back to 1964, the company started as an engineering contractor and has since completed numerous landmark projects across various sectors such as ports, infrastructure, residential developments, townships, and commercial projects.

Investment Thesis

Asset-light Business Model – Efficient and Scalable

Diversified Business: MICL has strategically adopted a business model that can be divided into two segments, each with multiple streams of income. The first segment is Real Estate Projects, and the second is EPC Projects. These segments have different streams of income, which helps diversify the company’s risk profile. For the real estate business, MICL has adopted a Joint Venture (JV)/Development Management (DM)/Joint Development (JD) model, which spreads its leverage with other partners. This model is both value-accretive and scalable, allowing the company to maximize cash flows while maintaining low leverage.

MICL’s Income Streams and Business Model Innovation: The income streams for MICL include DM fee (~12-14%), EPC margin on ports (~20%), interest margin (~10-14%), and PMC margin (~10%). Currently, the ratio of JV/DM projects to owned projects is 1:3, but the company plans to adjust this to 2:3 in the coming years, ensuring efficient use of capital and high scalability. Under DM all cost and revenue is booked in landlord, while in JV all costs and revenue is booked in SPV while MICL receives share of profit based on its stake in JV entity. This approach maximizes the company’s bottom line without exerting stress on the balance sheet.

MICL’s Real Estate Investments and Sales Performance: Being asset-light model, As of June 30, 2023, MICL has invested only Rs ~700 Cr in real estate projects, covering a portfolio of 4.6 million square feet. This relatively low investment for a real estate developer makes MICL an attractive company in this segment. Furthermore, MICL has near-zero inventory left in completed projects. The company boasts an impressive sales record at the launch, with over 70% of its ongoing projects already sold, this does not include new launches done in last six months – Avaan and Aaradhya One Park.

Robust Order Book & Pipeline of Upcoming Projects

Currently, MICL has ~2.0 Mn square feet of ongoing projects, including development projects in Dahisar, Ghatkopar, Mulund, Juhu, and Tardeo-Avaan. Its upcoming projects comprises around 3.7 Mn square feet of real estate projects. This includes – 1) two residential towers of Aaradhya Parkwood in Dahisar, 2) one of the largest redevelopment project in western suburbs in Goregaon on a 10 acre land parcel with a topline potential of over Rs 4000 Cr, 3) an ultra-luxury project in Pali Hill, Bandra, and 4) a gated community project comprising cluster of 10 societies spanning over 10,000 square meters in Ghatkopar East. Additionally, it has the potential for further development in the Dahisar project totaling about 10 Lc square feet and ~3 Lc square feet in the Vile Parle project. Moreover, MICL has expressed interest in launching atleast 3-4 upcoming projects in FY25 which mainly could comprise another balance two residentials towers of Aaradhya Parkwood in Dahisar, recently acquired Marine Lines project. and Vile Parle project. Furthermore, its EPC business order book stands healthy at Rs 1,047 Cr, which includes ongoing ports and infrastructure projects covering ~110 hectares. MICL is also determined to bid for future government and commercial projects.

Healthy Balance Sheet and Financial Discipline

The company has maintained a very healthy balance sheet with only Rs 205 Cr in borrowings, which include short-term borrowings of Rs 135 Cr (secured debt). It has considerably reduced its debt by around Rs 300 Cr in FY23, Year-to-Date. The company exhibits a very low debt book for a real estate developer, combined with healthy and consistent cash flow. Despite paying back a majority of debt in FY23-24, it has cash and cash equivalents of Rs ~545 Cr as on Dec-23. Additionally, In Dec-23, company issued Rs 543 Cr of preferential shares for future growth expansion. A low leverage and high cash flow blend present a very efficient and attractive scenario in the real estate development business. Due to its asset-light business model, it can scale up without significant capital pressure, thereby improving the bottom line in coming years. Valuation & Recommendation

We initiate coverage on Man Infraconstruction (MICL) with a BUY recommendation. Our recommendation is supported by a) Healthy project pipeline; b) Asset–light business model, and c) Strong execution capabilities. Based on our DCF valuation method, we arrive at a Target Price of Rs 270/share, implying an upside of 28% from the current levels.

Click here to download Man Infraconstruction Ltd – Initiating Coverage by AXIS Securities 12-04-2024