Operation Epic Churn

We see the recent correction in the market and stock prices due to the ongoing conflict between Iran and Israel-US and resultant dislocations in stock prices as an opportunity to (1) add ‘better’ stocks, (2) remove ‘narrative’ stocks and (3) reduce positions in expensive cement and consumer stocks. A churn in portfolios may be the best option, given the circumstances.

Short-term conflict base case scenario for now

The duration and extent of the ongoing conflict between Iran and US-Israel remain highly uncertain, given (1) different objectives and ‘pain’ thresholds of different actors and (2) the unpredictable nature and outcome of conflicts. For now, we assume (1) a few weeks of high-intensity conflict, (2) several months of heightened tensions and (3) normalization of trade in oil and gas through the Strait of Hormuz (SoH) over the next few weeks as our base case scenario.

Assessing collateral damage to India—limited if conflict is over in a few weeks

The impact on BoP is relatively straightforward, with a US$10/bbl change in crude price and related change in natural gas price impacting India’s CAD by US$20 bn (0.5% of GDP) on an annualized basis; see Exhibit 1. The impact on the fiscal is more nuanced and will depend on the extent of the conflict and the sharing of higher costs between companies (PSUs), customers and government (see Exhibit 2 for a few hypothetical scenarios). The impact on growth will depend on the availability of crude, gas and refined products, which have been disrupted through the SoH (see Exhibits 3-6).

Too early to assess earnings impact, although downside risks have increased

We do not see material risks to our earnings estimates (see Exhibits 7-9), except for the oil, gas & consumable fuels sector, from the higher oil prices if elevated oil prices were to last beyond a few weeks. We expect (1) pure refiners and upstream oil & gas companies to see a short-term earnings boost on higher refining margins and oil prices, (2) downstream oil & gas companies to see earnings cuts; they may not be able to pass on the higher crude prices to customers based on past form; India has several forthcoming state elections (see Exhibit 10) and (3) downstream users of petroleum products will see varying short-term earnings impact but no long-lasting damage.

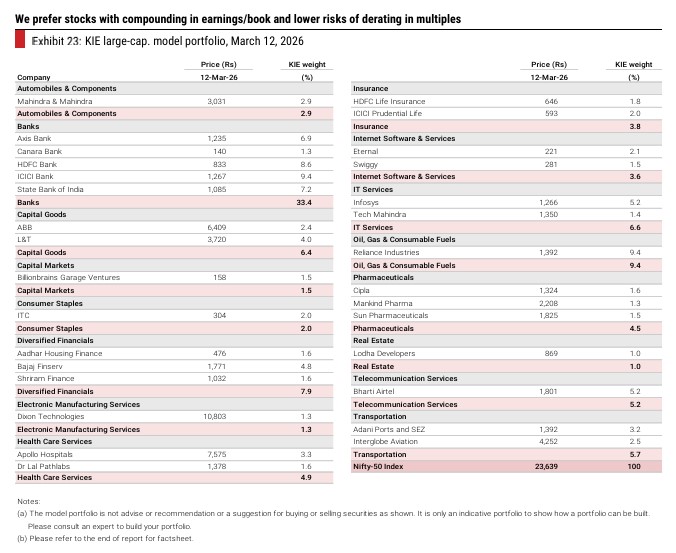

Churning portfolios while waiting for more clarity to emerge

We see the sharp correction in stock prices and dislocation in parts of the market as an opportunity for investors to review their portfolios and make appropriate changes. The haphazard correction in stock prices across caps (see Exhibits 11-13), sectors (see Exhibit 14) and companies would imply a permanent decline in companies’ earnings, which is clearly invalid. We recommend reducing positions in cement, consumer staples and ‘narrative’ stocks, which trade at high or inexplicable valuations and adding to financials and other sectors (see Exhibits 15-21 for valuations across sectors and stocks), which have fallen sharply on unjustified concerns.