AIL’s performance exceeded expectations across all parameters

Robust performance, Strong growth potential ahead, Maintain BUY! Overall performance was above our expectations....

The listed Indian CRDMO players have entered a sustained growth phase (17% revenue CAGR...

Suzlon is well-placed to benefit from India’s accelerating wind-energy buildout

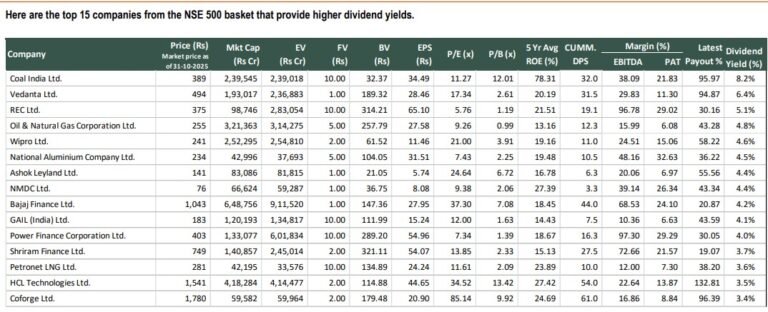

top 15 companies with high dividend yield

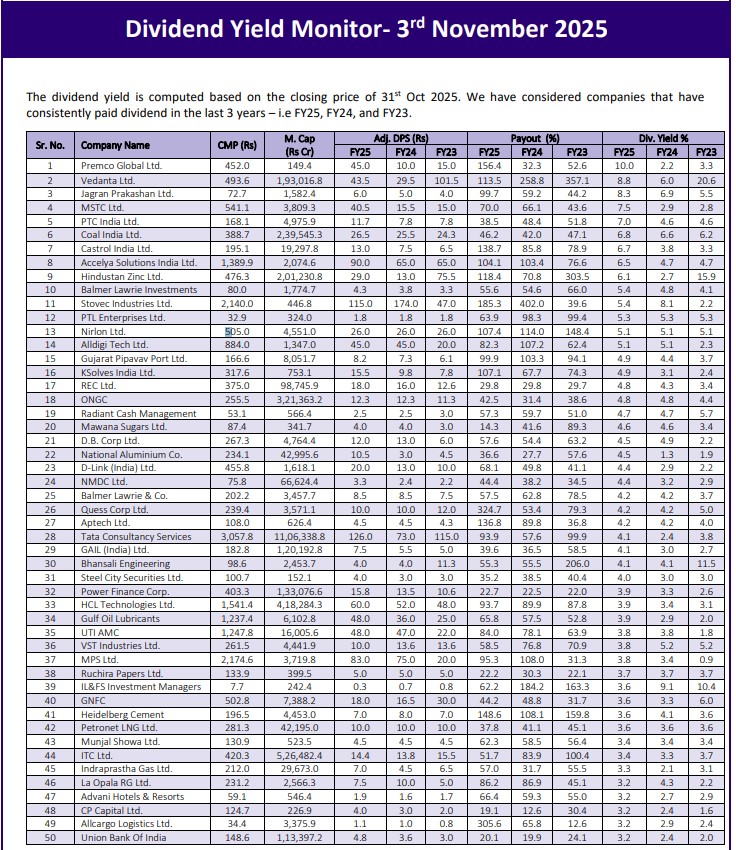

Dividend Yield Monitor- 3rd November 2025

The recycling industry is witnessing structural tailwinds, with increased regulatory focus shifting scrap flows...

Post the recent correction, APTUS is set for a re-rating

SAMHI IN trades at attractive valuation of 11.1x/8.8x our FY27E/FY28E EBITDA estimates